Ubisoft Entertainment SA (EPA:UBI) Just Released Its Full-Year Results And Analysts Are Updating Their Estimates

Ubisoft Entertainment SA (EPA:UBI) shareholders are probably feeling a little disappointed, since its shares fell 6.5% to €69.08 in the week after its latest yearly results. The results don't look great, especially considering that statutory losses grew 468% to€1.12 per share. Revenues of €1.6b did beat expectations by 8.3%, but it looks like a bit of a cold comfort. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

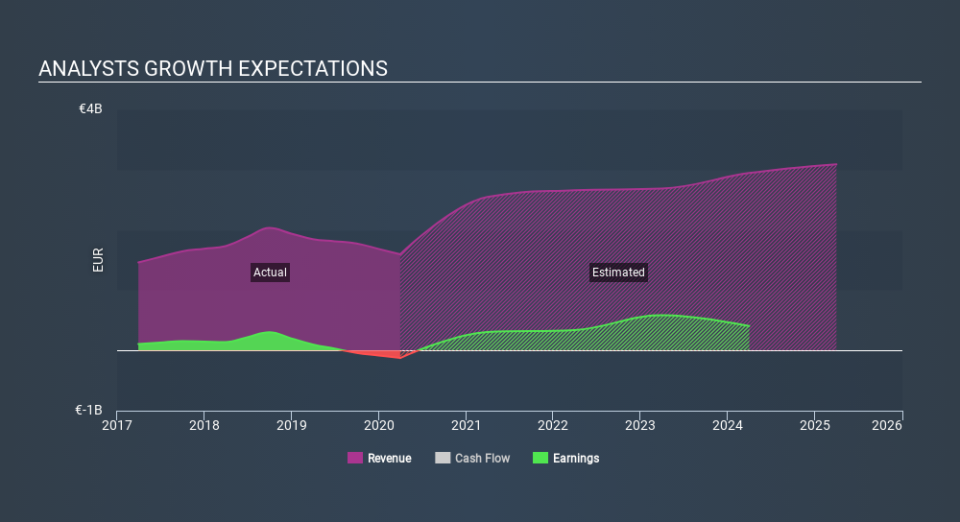

View our latest analysis for Ubisoft Entertainment

Taking into account the latest results, the consensus forecast from Ubisoft Entertainment's 20 analysts is for revenues of €2.55b in 2021, which would reflect a substantial 60% improvement in sales compared to the last 12 months. Earnings are expected to improve, with Ubisoft Entertainment forecast to report a statutory profit of €2.49 per share. Before this earnings report, the analysts had been forecasting revenues of €2.56b and earnings per share (EPS) of €2.51 in 2021. So it's pretty clear that, although the analysts have updated their estimates, there's been no major change in expectations for the business following the latest results.

There were no changes to revenue or earnings estimates or the price target of €77.91, suggesting that the company has met expectations in its recent result. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values Ubisoft Entertainment at €89.00 per share, while the most bearish prices it at €57.00. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Ubisoft Entertainment's past performance and to peers in the same industry. It's clear from the latest estimates that Ubisoft Entertainment's rate of growth is expected to accelerate meaningfully, with the forecast 60% revenue growth noticeably faster than its historical growth of 7.2%p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 5.3% next year. Factoring in the forecast acceleration in revenue, it's pretty clear that Ubisoft Entertainment is expected to grow much faster than its industry.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. The consensus price target held steady at €77.91, with the latest estimates not enough to have an impact on their price targets.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for Ubisoft Entertainment going out to 2025, and you can see them free on our platform here.

Plus, you should also learn about the 2 warning signs we've spotted with Ubisoft Entertainment (including 1 which makes us a bit uncomfortable) .

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.