Ultragenyx Pharmaceutical Stock Is Estimated To Be Significantly Undervalued

- By GF Value

The stock of Ultragenyx Pharmaceutical (NAS:RARE, 30-year Financials) is believed to be significantly undervalued, according to GuruFocus Value calculation. GuruFocus Value is GuruFocus' estimate of the fair value at which the stock should be traded. It is calculated based on the historical multiples that the stock has traded at, the past business growth and analyst estimates of future business performance. If the price of a stock is significantly above the GF Value Line, it is overvalued and its future return is likely to be poor. On the other hand, if it is significantly below the GF Value Line, its future return will likely be higher. At its current price of $113.2 per share and the market cap of $7.6 billion, Ultragenyx Pharmaceutical stock gives every indication of being significantly undervalued. GF Value for Ultragenyx Pharmaceutical is shown in the chart below.

Because Ultragenyx Pharmaceutical is significantly undervalued, the long-term return of its stock is likely to be much higher than its business growth, which averaged 315.7% over the past three years and is estimated to grow 21.69% annually over the next three to five years.

Link: These companies may deliever higher future returns at reduced risk.

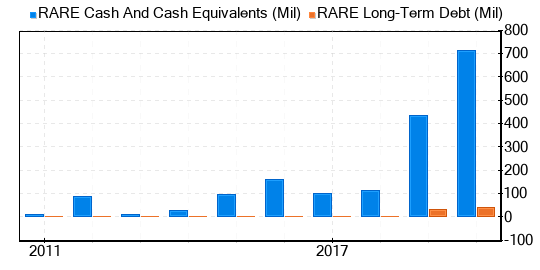

Since investing in companies with low financial strength could result in permanent capital loss, investors must carefully review a company's financial strength before deciding whether to buy shares. Looking at the cash-to-debt ratio and interest coverage can give a good initial perspective on the company's financial strength. Ultragenyx Pharmaceutical has a cash-to-debt ratio of 24.91, which ranks in the middle range of the companies in Biotechnology industry. Based on this, GuruFocus ranks Ultragenyx Pharmaceutical's financial strength as 7 out of 10, suggesting fair balance sheet. This is the debt and cash of Ultragenyx Pharmaceutical over the past years:

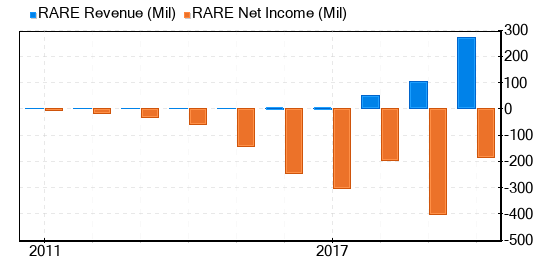

It poses less risk to invest in profitable companies, especially those that have demonstrated consistent profitability over the long term. A company with high profit margins is also typically a safer investment than one with low profit margins. Ultragenyx Pharmaceutical has been profitable 0 over the past 10 years. Over the past twelve months, the company had a revenue of $271 million and loss of $3.14 a share. Its operating margin is -121.80%, which ranks in the middle range of the companies in Biotechnology industry. Overall, GuruFocus ranks the profitability of Ultragenyx Pharmaceutical at 1 out of 10, which indicates poor profitability. This is the revenue and net income of Ultragenyx Pharmaceutical over the past years:

Growth is probably the most important factor in the valuation of a company. GuruFocus research has found that growth is closely correlated with the long term stock performance of a company. A faster growing company creates more value for shareholders, especially if the growth is profitable. The 3-year average annual revenue growth of Ultragenyx Pharmaceutical is 315.7%, which ranks better than 98% of the companies in Biotechnology industry. The 3-year average EBITDA growth rate is 32.2%, which ranks better than 78% of the companies in Biotechnology industry.

Another method of determining the profitability of a company is to compare its return on invested capital to the weighted average cost of capital. Return on invested capital (ROIC) measures how well a company generates cash flow relative to the capital it has invested in its business. The weighted average cost of capital (WACC) is the rate that a company is expected to pay on average to all its security holders to finance its assets. When the ROIC is higher than the WACC, it implies the company is creating value for shareholders. For the past 12 months, Ultragenyx Pharmaceutical's return on invested capital is -70.22, and its cost of capital is 12.91. The historical ROIC vs WACC comparison of Ultragenyx Pharmaceutical is shown below:

In summary, the stock of Ultragenyx Pharmaceutical (NAS:RARE, 30-year Financials) appears to be significantly undervalued. The company's financial condition is fair and its profitability is poor. Its growth ranks better than 78% of the companies in Biotechnology industry. To learn more about Ultragenyx Pharmaceutical stock, you can check out its 30-year Financials here.

To find out the high quality companies that may deliever above average returns, please check out GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.