Wall Street’s Best Analyst Suggests 2 Semiconductor Stocks to Buy — Here’s What Makes Them Stand Out

Today, investors have access to huge amounts of information that can help in pointing towards the best stocks to pick up. So much information, in fact, that it can often result in overload and confusion, rather than providing a clear signal.

Therefore, it might be best to stick to an uncomplicated regime and let the stock picking experts lead the way. And on Wall Street, right now Jeffries analyst Mark Lipacis is the best of the lot. According to TipRanks, a platform that tracks and measures the performance of anyone giving financial advice online, over the past year, 72% of Lipacis’ recommendations have been successful. At the same time, his choices have generated an average return of 29.7%. These metrics have positioned the 5-star expert as the Street’s Top Analyst.

Recently, Lipacis has been writing up positive reviews for a pair of semiconductor stocks, believing they are primed to push ahead from here. So, let’s see what it is about these names that makes them stand out from the pack.

GlobalFoundries (GFS)

The first semiconductor stock we’ll look at is GlobalFoundries, an important player in the US chip industry with a large multinational presence. The company is based in Malta, New York, and has operations in the US, in the EU, and in East Asia, with a large footprint in Singapore. The company’s products are found in smart mobile devices, in IoT applications, in personal computing, and in the automotive, aerospace, and defense industries.

Unlike many US-based chip makers, GlobalFoundries has maintained a strong presence in its home country – with design and R&D centers on the West Coast and manufacturing and foundry facilities in the Northeast. This gives the company a built-in advantage at a time of increasing geopolitical tensions with China – a major tech competitor – over Taiwan – the world’s largest chip exporter. In addition, GlobalFoundries is proactive at protecting its intellectual property, and recently filed a lawsuit against the tech and business giant IBM, alleging trade secret misappropriation.

A homefield advantage and safe secrets are good to have, but investors want to see results. GlobalFoundries’ 1Q23 numbers had some good ones, but not all the news pleased investors.

The quarterly top line, at $1.84 billion, slipped 5% year-over-year, but came in just over the forecast, beating it by $10 million. At the bottom line, GlobalFoundries’ non-GAAP earnings of 52 cents per share were up 10 cents y/y and beat the estimates by 3 cents. Also of note, the company reported liquid reserves totaling $3.23 billion.

However, the stock fell after the earnings release. Investors were worried by an adjusted EBITDA miss ($655 million vs. the analysts’ expectation of $694.7 million) and the concurrent announcement of changes to the management team, with new people stepping in as CFO and CBO.

For his part, top analyst Mark Lipacis isn’t worried. Assessing the print, Lipacis noted the company’s ‘onshore’ US footprint as an important advantage, writing: “We view GFS as the leading trailing-node, analog/ mixed-signal foundry benefiting from IoT demand and customers moving to a fab-lite model. We continue to see GFS as a beneficiary of the nationalization of the supply chain trend. As a result, we expect GFS to maintain a premium valuation multiple.”

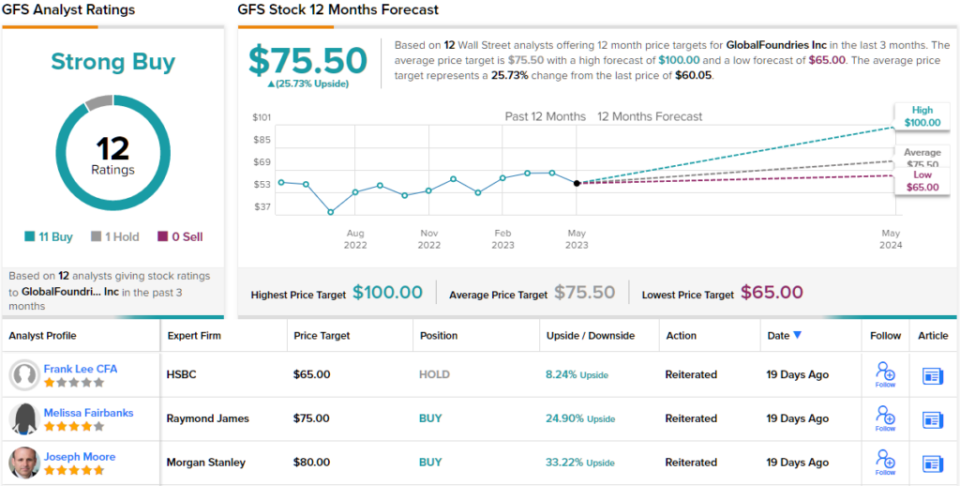

Based on this stance, Lipacis rates GFS shares as a Buy, and he sets a $73 price target to imply a 22% one-year upside potential.

Wall Street’s top analyst is hardly an outlier here. GFS shares have 12 recent analyst reviews, and these include 11 Buys against 1 Hold, for a Strong Buy consensus rating. (See GFS stock forecast)

Texas Instruments (TXN)

Next up is Texas Instruments, a Dallas-based firm with a long history in the tech field. The company traces its roots to 1930, and by the 1960s it had become a strong name in consumer electronics, known for its popular lines of calculators and the ‘Speak & Spell’ educational toy franchise. Today, the company is known as a major supplier of analog technology, electronics, and processor chips to the industrial economy, and is a major supplier for both automotive and aerospace high-tech needs. TI still keeps a foot in the educational sector, and has several graphic calculators on the market.

All of this is background to one of the world’s largest tech companies. TI boasts a market cap of $155 billion and brought in just over $20 billion in revenue last year. The firm also has a sound record of returning value to shareholders. Since 2004, the company has posted 19 consecutive years of dividend increases, while also cutting back on outstanding shares by 47%. Over the same period, TI has also shown 11% annual growth in free cash flow.

However, in the most recent reported quarter, 1Q23, TI showed mixed results. At the top line, the $4.38 billion in revenue was down almost 11% from 1Q22 – but was $10 million better than had been expected. The bottom-line EPS, at $1.85, was down from $2.18 in the prior-year period, but beat the forecast by 7 cents, or 3.6%.

That said, the company came unstuck with its guide. The outlook for Q2 revenue was set in the range of $4.17 billion to $4.53 billion, against the consensus figure of $4.46 billion. On earnings, the Q2 outlook calls for EPS in the range of $1.62 to $1.88; the consensus figure was $1.87.

Looking under the hood at TI after the earnings release, Mark Lipacis remains optimistic. He notes the weaker performance year-over-year, but still feels confident long-term.

“We highlighted TXN as our top large-cap analog pick heading into earnings because it was one of the few analog companies that saw material cut to CY23 EPS estimates (~20%), and it has been a bottom-quartile stock performer YTD… We continue to favor TXN because it is shipping below trendline, and we believe its internal manufacturing strategy will lead to share gains… We remain buyers after the print,” Lipacis noted.

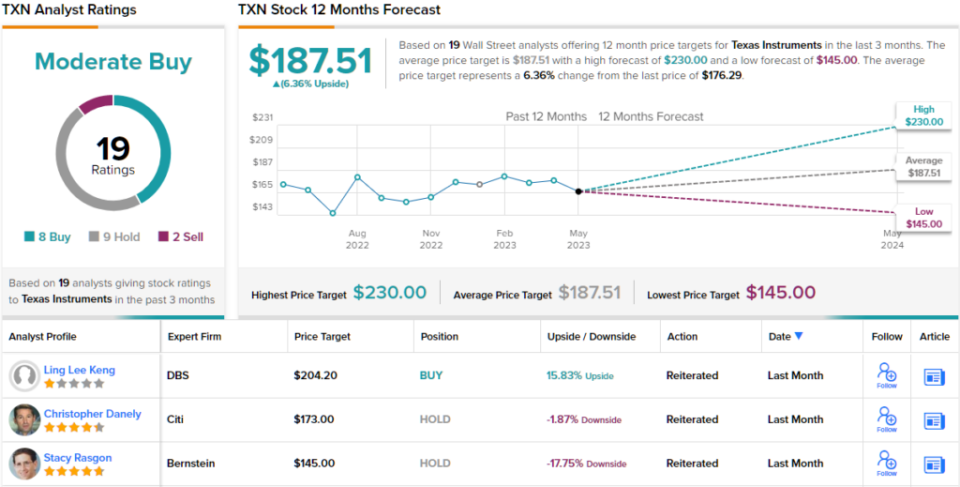

As such, Lipacis reiterated a Buy rating and $215 price target that indicates room for 22% share appreciation over the next 12 months.

Big-name tech has never failed to pick up attention from Wall Street, and Texas Instruments has 19 analyst reviews on file, including 8 Buys, 9 Holds and 2 Sells – for a Moderate Buy consensus rating. (See TXN stock forecast)

To stay updated on Mark Lipacis’ latest ratings and price target, check out his profile page on TipRanks.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.