Should Wayside Technology Group, Inc. (NASDAQ:WSTG) Be Part Of Your Dividend Portfolio?

Dividend paying stocks like Wayside Technology Group, Inc. (NASDAQ:WSTG) tend to be popular with investors, and for good reason - some research suggests a significant amount of all stock market returns come from reinvested dividends. If you are hoping to live on your dividends, it's important to be more stringent with your investments than the average punter. Regular readers know we like to apply the same approach to each dividend stock, and we hope you'll find our analysis useful.

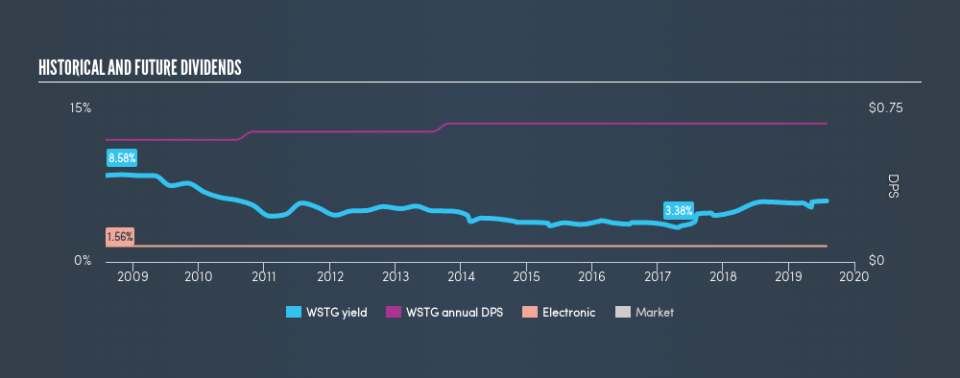

A high yield and a long history of paying dividends is an appealing combination for Wayside Technology Group. We'd guess that plenty of investors have purchased it for the income. The company also bought back stock during the year, equivalent to approximately 1.8% of the company's market capitalisation at the time. When buying stocks for their dividends, you should always run through the checks below, to see if the dividend looks sustainable.

Click the interactive chart for our full dividend analysis

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. As a result, we should always investigate whether a company can afford its dividend, measured as a percentage of a company's net income after tax. Wayside Technology Group paid out 90% of its profit as dividends, over the trailing twelve month period. It's paying out most of its earnings, which limits the amount that can be reinvested in the business. This may indicate limited need for further capital within the business, or highlight a commitment to paying a dividend.

Another important check we do is to see if the free cash flow generated is sufficient to pay the dividend. Wayside Technology Group paid out a conservative 27% of its free cash flow as dividends last year. It's positive to see that Wayside Technology Group's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Remember, you can always get a snapshot of Wayside Technology Group's latest financial position, by checking our visualisation of its financial health.

Dividend Volatility

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. Wayside Technology Group has been paying dividends for a long time, but for the purpose of this analysis, we only examine the past 10 years of payments. The dividend has been stable over the past 10 years, which is great. We think this could suggest some resilience to the business and its dividends. During the past ten-year period, the first annual payment was US$0.60 in 2009, compared to US$0.68 last year. This works out to be a compound annual growth rate (CAGR) of approximately 1.3% a year over that time.

While the consistency in the dividend payments is impressive, we think the relatively slow rate of growth is unappealing.

Dividend Growth Potential

While dividend payments have been relatively reliable, it would also be nice if earnings per share (EPS) were growing, as this is essential to maintaining the dividend's purchasing power over the long term. Wayside Technology Group's earnings per share have shrunk at 12% a year over the past five years. A sharp decline in earnings per share is not great from from a dividend perspective, as even conservative payout ratios can come under pressure if earnings fall far enough.

Conclusion

To summarise, shareholders should always check that Wayside Technology Group's dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. First, we think Wayside Technology Group has an acceptable payout ratio and its dividend is well covered by cashflow. Second, it has a limited history of earnings per share growth, but at least the dividends have been relatively stable. Ultimately, Wayside Technology Group comes up short on our dividend analysis. It's not that we think it is a bad company - just that there are likely more appealing dividend prospects out there on this analysis.

Now, if you want to look closer, it would be worth checking out our free research on Wayside Technology Group management tenure, salary, and performance.

We have also put together a list of global stocks with a market capitalisation above $1bn and yielding more 3%.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.