While shareholders of ZoomInfo Technologies (NASDAQ:ZI) are in the red over the last year, underlying earnings have actually grown

It is a pleasure to report that the ZoomInfo Technologies Inc. (NASDAQ:ZI) is up 43% in the last quarter. But that doesn't change the reality of under-performance over the last twelve months. After all, the share price is down 33% in the last year, significantly under-performing the market.

The recent uptick of 5.3% could be a positive sign of things to come, so let's take a lot at historical fundamentals.

View our latest analysis for ZoomInfo Technologies

We don't think that ZoomInfo Technologies' modest trailing twelve month profit has the market's full attention at the moment. We think revenue is probably a better guide. Generally speaking, we'd consider a stock like this alongside loss-making companies, simply because the quantum of the profit is so low. It would be hard to believe in a more profitable future without growing revenues.

In the last year ZoomInfo Technologies saw its revenue grow by 57%. That's a strong result which is better than most other loss making companies. Given the revenue growth, the share price drop of 33% seems quite harsh. Our sympathies to shareholders who are now underwater. Prima facie, revenue growth like that should be a good thing, so it's worth checking whether losses have stabilized. Our brains have evolved to think in linear fashion, so there's value in learning to recognize exponential growth. We are, in some ways, simply the wisest of the monkeys.

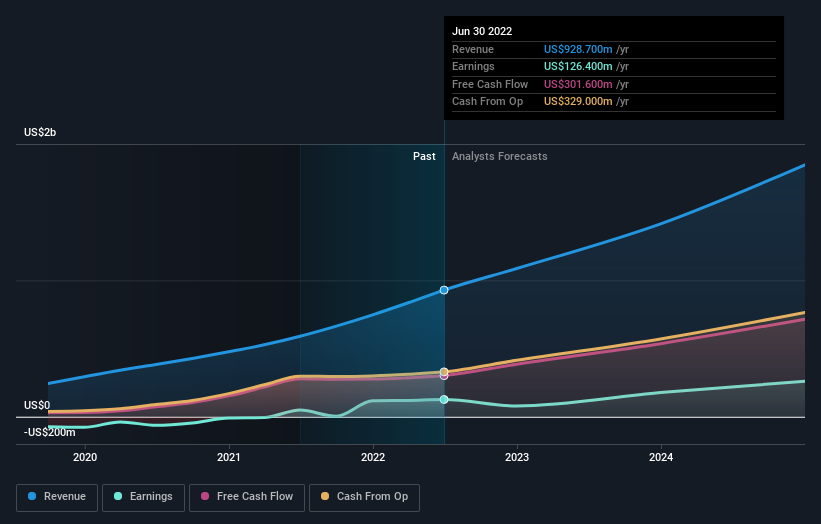

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

We're pleased to report that the CEO is remunerated more modestly than most CEOs at similarly capitalized companies. But while CEO remuneration is always worth checking, the really important question is whether the company can grow earnings going forward. You can see what analysts are predicting for ZoomInfo Technologies in this interactive graph of future profit estimates.

A Different Perspective

ZoomInfo Technologies shareholders are down 33% for the year, even worse than the market loss of 16%. That's disappointing, but it's worth keeping in mind that the market-wide selling wouldn't have helped. It's great to see a nice little 43% rebound in the last three months. Let's just hope this isn't the widely-feared 'dead cat bounce' (which would indicate further declines to come). While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Take risks, for example - ZoomInfo Technologies has 3 warning signs (and 1 which can't be ignored) we think you should know about.

But note: ZoomInfo Technologies may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here