Why You're Probably Never Getting a Real Raise From Social Security

In 2018, Social Security recipients got a 2% raise thanks to the Cost-of-Living Adjustment (COLA). While a 2% raise should theoretically result in about $27 more per month for seniors who received the average retirement benefit of $1,377 in 2017, many seniors will see no bump in income at all.

For those whose Social Security benefits didn't rise in 2018, it'll be business as usual. Social Security raises have been small in recent years, if they've happened at all. And, even when seniors get a COLA that bumps up their monthly checks, the raise doesn't usually increase purchasing power -- which means it's not a real raise. Here's why this happens.

Image source: Getty Images.

Cost-of-living adjustments aren't keeping pace with rising expenses

Social Security raises come in the form of cost-of-living adjustments calculated based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) -- despite the fact that most seniors are neither urban wage earners nor clerical workers. CPI-W is a price index published by the Bureau of Labor Statistics that tracks how much prices rise on things like food, housing, and transportation.

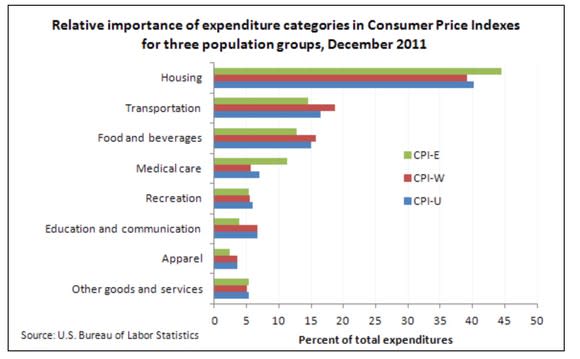

Unfortunately, CPI-W doesn't give as much weight as it should to rising prices on things seniors spend most of their money on -- like healthcare -- because it emphasizes the things urban wage earners do with their dollars, like paying for education, apparel, and entertainment. This chart shows the breakdown of expenditure categories given the most weight in CPI-W, along with two other consumer price indexes.

Source: Bureau of Labor Statistics.

Because CPI-W underweights categories of spending seniors actually spend a disproportionate share of their money on, seniors are getting cost of living adjustments that are too small given the realities of their spending patterns.

Seniors have gotten an average cost of living adjustment of just 1.35% per year from 2010 to 2018, with no raises at all in two of eight years. In 2016 alone, out-of-pocket health spending grew by 3.9%, according to Centers for Medicare and Medicaid Services.

A different index, CPI-E, which is tailored to measure spending habits of the elderly, has shown the actual cost of living for seniors is likely increasing faster than CPI-W suggests. In fact, from 1982 to 2011, CPI-E rose an annual average of 3.1% compared with CPI-W increases of 2.9%. Much of this discrepancy is explained by both shelter costs outpacing overall inflation and, more significantly, by a 5.1% annual increase in medical care costs compared with a 2.8% cost increase for all non-medical items.

If you get an average raise that's lower than the actual increase in your cost of living, you haven't gotten a real raise even if the check looks bigger. And as long as CPI-W continues to be the metric by which Social Security raises are measured, COLA adjustments are likely to continue to be too low for seniors to actually increase their purchasing power.

Medicare premiums typically increase faster than Social Security

Speaking of medical expenses going up, it's not just rising copays and increasing prescription drug prices that make Social Security raises nothing more than a mirage. Rising Medicare premiums can literally cause your Social Security raise to disappear so you don't even get a bigger Social Security benefit deposited.

When you're receiving Social Security and Medicare, as most seniors are, your Medicare Part B premiums are typically deducted right from your Social Security benefit. These Medicare premiums don't stay steady -- they regularly increase.

Seniors don't always have to pay this increase right away. Medicare sets a standard premium, which was $134 in 2017 per month. However, if Medicare premiums go up more than COLAs, most seniors don't pay the full standard premium thanks to "hold harmless" provisions that prevent Social Security checks from getting smaller due to Medicare increases. Since seniors saw bigger Medicare increases than COLAs, most seniors in 2017 had only $109 deducted from their Social Security benefits for Medicare premiums -- $25 less than premiums actually cost.

But, when seniors do get a COLA, those seniors protected by hold harmless provisions need to catch back up to paying the standard premium. This means all those seniors paying only $109 now need to pay the 2018 standard premiums, which remained at $134 per month. This $25 increase means the average $27 raise seniors were getting all but disappears, which explains why around 70% of retirees won't see any extra money in 2018 despite the 2% COLA.

This problem is likely to reoccur in the future and again prevent seniors from getting a bigger benefits check.

How can you maximize your Social Security benefits?

Since Social Security raises probably aren't going to improve your standard of living, the only thing you can do if you plan to rely on Social Security for a large portion of your income is to try to get the maximum benefit possible. This often means working longer, as Social Security benefits decline if you retire before full retirement age but increase if you wait, up until age 70.

Of course, even if you get the maximum Social Security benefits, living on Social Security alone is almost impossible. Saving and investing during your career so you have a big nest egg means you won't have to depend on Social Security and it won't matter so much if you receive a paltry raise or no raise at all.

More From The Motley Fool

The Motley Fool has a disclosure policy.