Is Yamana Gold Inc. a Buy?

A solid 21% jump in Yamana Gold (NYSE: AUY) shares in December lifted investors' hopes of a strong year ahead for the gold stock. Unfortunately, Yamana has been a dampener so far this year, down about 7.5% as of this writing. Comparatively, rival Goldcorp (NYSE: GG) has gained nearly as much year to date.

To be fair, there's nothing wrong with Yamana Gold. Its margins have been low, but the gold miner has a strong production profile, is focused on costs, and has visible cash flow catalysts in the near future, as the charts below reveal.

A key mine is finally on line

Yamana Gold is coming off a major expansionary phase. On June 26, its seventh mine, Cerro Moro, hit commercial production on time and within budget. It's a significant development, as Cerro Moro is expected to be among Yamana Gold's lowest-cost mines and a major contributor to its production and cash flows going forward.

It's time you pay attention to Yamana Gold. Image source: Getty Images.

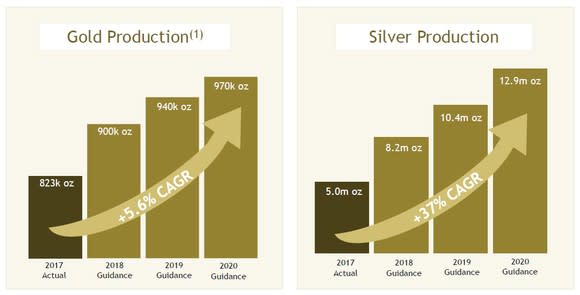

This year, Cerro Moro should produce 85,000 gold ounces and 3.75 million silver ounces. By 2020, Yamana expects the mine to add 130,000 gold ounces and 8.3 million silver ounces. The company has other projects under expansion, including Canadian Malartic, Jacobina, and Minera Florida, all of which should push its production higher.

Image source: Yamana Gold.

That translates into a production of 1.15 million gold equivalent ounces (GEOs) by 2020 compared to 892,000 GEOs produced in 2017. For the longer run, Yamana is developing projects like Chapada in Brazil to keep production flowing.

Yamana Gold's costs are expected to come down as production rises.

Costs are headed down

Given the inherent volatility in gold prices, cost effectiveness is the key to profitability for gold miners. More and more gold miners are now focused on improving productivity to cut costs. Goldcorp, for instance, has outlined an ambitious plan to lower its all-in sustaining cost (AISC) by 20% between 2017 and 2020. Yamana has a plan up its sleeve as well.

In fiscal 2017, Yamana Gold reported by-product AISC of $888 per ounce of gold, or a 1% improvement over 2016. Cerro Moro is expected to improve Yamana Gold's cost profile considerably, starting this year, thanks to its projected 2018 AISC of only $650 per ounce of gold -- also the lowest among all of Yamana's mines except Chapada copper mine. That number looks even more significant when you realize that the company's three largest gold-producing mines each is expected to have AISC above $900 per ounce in 2018.

Image source: Yamana Gold.

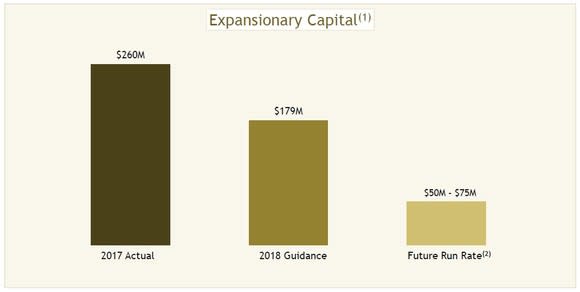

It's not surprising, then, that Yamana has prioritized the development of Cerro Moro in recent years and is banking heavily on the project to grow sales as well as cash flows in coming years.

Ample cash flows coming to cover debt

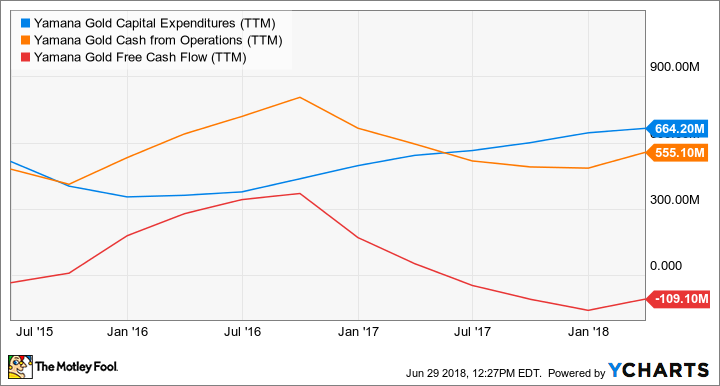

Investors have been wary of Yamana Gold's discouraging free cash flow (FCF) trend, but higher capital expenditures were largely to blame. Yamana is now ready to reap the fruits of some of those investments, or as CEO Peter Marrone put it in the company's 2017 annual report, Yamana is transitioning to a "cash harvesting phase of growth."

AUY Capital Expenditures (TTM) data by YCharts.

With Cerro Morro and Canadian Malartic projects near completion, Yamana's capital spending budget is expected to come down substantially next year onward. At the same time, higher production should drive its sales and operating cash flows higher.

The net effect should show up in its FCF, which should continue to rise at least through 2020. Yamana could also raise supplemental cash from other sources, such as the sale of its Gualcamayo mine in Argentina. The company is currently rightsizing operations at the mine while awaiting a purchase offer.

Image source: Yamana Gold.

Yamana hopes to use the incremental cash flows to pare down debt, which has been another cause for concern among investors: Its long-term debt was as high as $1.6 billion as of March 31. However, as scary as that number looks, it's worth noting that $1.2 billion of that debt isn't due before 2023. That leaves the the gold miner with ample time to build up its war chest.

So is it time to buy Yamana shares?

With Cerro Moro coming on line, investors now have greater visibility into Yamana's production and cash flow growth. For the potential, the stock looks like a great long-term bet at just five times price to operating cash flow, which is exactly half that of Goldcorp.

More From The Motley Fool

Neha Chamaria has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.