3 Reasons to Retain Veeva Systems (VEEV) Stock in Your Portfolio

Veeva Systems Inc. VEEV is well-poised for growth in the coming quarters, courtesy of a strong product portfolio. The optimism led by a solid fourth-quarter fiscal 2023 performance, along with strong product adoption, is expected to contribute further. Stiff competition and forex woes persist.

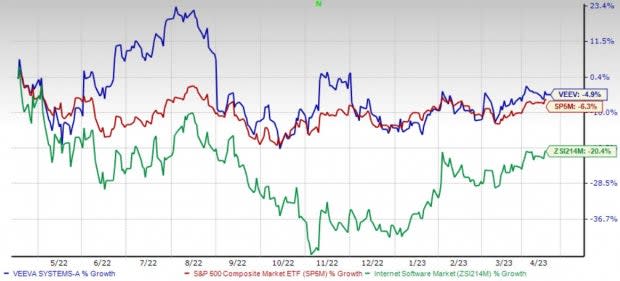

Over the past year, this Zacks Rank #3 (Hold) stock has lost 4.9% compared with the 20.3% decline of the industry and a 6.3% fall of the S&P 500 composite.

The renowned provider of cloud-based software applications and data solutions for the life sciences industry has a market capitalization of $28.59 billion. The company projects 23% growth for the next five years and expects to maintain its strong performance. It has delivered an earnings surprise of 6.5% for the past four quarters, on average.

Image Source: Zacks Investment Research

Let’s delve deeper.

Strong Product Portfolio: We are optimistic about Veeva Systems’ unique solutions, which include Veeva Vault, Veeva CRM (customer relationship management), Veeva Network and Veeva OpenData. In October 2022, the company announced Veeva Vault CRM for MedTech, a unified CRM and content management application built for MedTech sales teams, key account managers and medical affairs professionals. The same month, the company announced the availability of Veeva ePRO, a key advancement in patient-centric digital trials.

Product Adoption: We are upbeat about Veeva Systems registering a robust adoption for its products over the past few months. In March, the company announced that more than 100 life sciences companies are using Veeva CRM Events Management to plan and execute in-person, virtual and hybrid events worldwide.

Veeva Systems, in February, announced that biopharmas are leveraging Veeva Vault PromoMats for modular content to accelerate medical, legal and regulatory reviews and drive more impactful engagement across channels and regions.

Strong Q4 Results: Veeva Systems’ solid fourth-quarter fiscal 2023 results buoy optimism. The company saw an uptick in the overall top and bottom lines and robust performances by both segments during the quarter. The company continued to benefit from its flagship Vault platform, which is encouraging. Veeva Systems’ continued strength in its Commercial Solutions, with new small- to mid-sized customer additions, looked promising.

Downsides

Forex Woes: Veeva Systems derives a major share of its revenues from international operations. Some of its international agreements provide payment denominated in local currencies and the majority of its local costs are also denominated in local currencies. Fluctuations in the value of the U.S. dollar versus foreign currencies may impact its operating results when converted into U.S. dollars.

Stiff Competition: Veeva Systems operates in a highly competitive market. In new sales cycles within the company’s largest product categories, it competes with other cloud-based solutions from providers that make applications for the life sciences industry. The company’s Commercial Cloud and Veeva Vault application suites also compete to replace client-server-based legacy solutions offered by large companies and other smaller application providers.

Estimate Trend

Veeva Systems is witnessing a negative estimate revision trend for fiscal 2024. In the past 90 days, the Zacks Consensus Estimate for its earnings has moved 3.3% south to $4.33.

The Zacks Consensus Estimate for the company’s first-quarter fiscal 2024 revenues is pegged at $517.6 million, suggesting a 2.5% improvement from the year-ago quarter’s reported number.

This compares to our fiscal first-quarter revenue estimate of $515.1 million, suggesting a 2% improvement from the year-ago quarter’s reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Hologic, Inc. HOLX, Henry Schein, Inc. HSIC and Masimo Corporation MASI.

Hologic, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth rate of 15.2%. HOLX’s earnings surpassed the Zacks Consensus Estimate in all the trailing four quarters, the average beat being 30.6%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Hologic has gained 11.9% against the industry’s 10.8% decline in the past year.

Henry Schein, sporting a Zacks Rank #1 at present, has an estimated long-term growth rate of 8.1%. HSIC’s earnings surpassed estimates in three of the trailing four quarters and matched the same in the other, the average beat being 2.9%.

Henry Schein has lost 8.6% compared with the industry’s 2.1% decline over the past year.

Masimo, flaunting a Zacks Rank #1 at present, has an estimated growth rate of 3.5% for 2023. MASI’s earnings surpassed estimates in all the trailing four quarters, the average beat being 9%.

Masimo has gained 47.4% against the industry’s 10.8% decline over the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Hologic, Inc. (HOLX) : Free Stock Analysis Report

Henry Schein, Inc. (HSIC) : Free Stock Analysis Report

Masimo Corporation (MASI) : Free Stock Analysis Report

Veeva Systems Inc. (VEEV) : Free Stock Analysis Report