Should You Be Adding LGL Group (NYSEMKT:LGL) To Your Watchlist Today?

Like a puppy chasing its tail, some new investors often chase 'the next big thing', even if that means buying 'story stocks' without revenue, let alone profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses.

In contrast to all that, I prefer to spend time on companies like LGL Group (NYSEMKT:LGL), which has not only revenues, but also profits. While profit is not necessarily a social good, it's easy to admire a business than can consistently produce it. In comparison, loss making companies act like a sponge for capital - but unlike such a sponge they do not always produce something when squeezed.

View our latest analysis for LGL Group

How Fast Is LGL Group Growing Its Earnings Per Share?

In business, though not in life, profits are a key measure of success; and share prices tend to reflect earnings per share (EPS). So like the hint of a smile on a face that I love, growing EPS generally makes me look twice. You can imagine, then, that it almost knocked my socks off when I realized that LGL Group grew its EPS from US$0.058 to US$0.37, in one short year. Even though that growth rate is unlikely to be repeated, that looks like a breakout improvement.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. The good news is that LGL Group is growing revenues, and EBIT margins improved by 5.2 percentage points to 6.7%, over the last year. Ticking those two boxes is a good sign of growth, in my book.

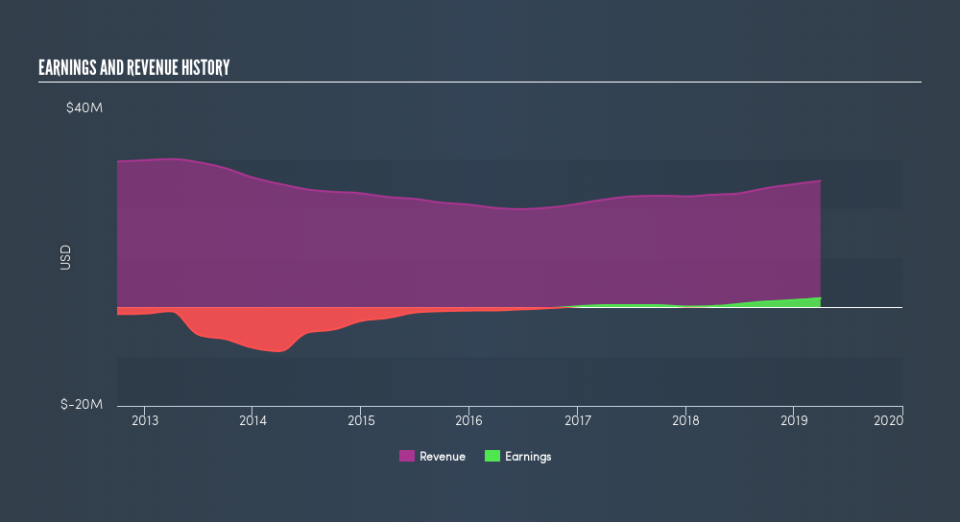

You can take a look at the company's revenue and earnings growth trend, in the chart below. Click on the chart to see the exact numbers.

LGL Group isn't a huge company, given its market capitalization of US$40m. That makes it extra important to check on its balance sheet strength.

Are LGL Group Insiders Aligned With All Shareholders?

Like the kids in the streets standing up for their beliefs, insider share purchases give me reason to believe in a brighter future. Because oftentimes, the purchase of stock is a sign that the buyer views it as undervalued. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

Although we did see some insider selling (worth -US$372.9k) this was overshadowed by a mountain of buying, totalling US$2.3m in just one year. I find this encouraging because it suggests they are optimistic about the LGL Group's future. Zooming in, we can see that the biggest insider purchase was by Non-Executive Chairman of the Board Marc Gabelli for US$1.5m worth of shares, at about US$7.50 per share.

Along with the insider buying, another encouraging sign for LGL Group is that insiders, as a group, have a considerable shareholding. To be specific, they have US$12m worth of shares. That's a lot of money, and no small incentive to work hard. That amounts to 30% of the company, demonstrating a degree of high-level alignment with shareholders.

Should You Add LGL Group To Your Watchlist?

LGL Group's earnings have taken off like any random crypto-currency did, back in 2017. If you're like me, you'll find it hard to ignore that sort of explosive EPS growth. And in fact, it could well signal a fundamental shift in the business economics. If that's the case, you may regret neglecting to put LGL Group on your watchlist. Of course, just because LGL Group is growing does not mean it is undervalued. If you're wondering about the valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of LGL Group, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.