Better Buy: Baker Hughes vs. Schlumberger

Shares of energy services companies like Baker Hughes, a GE Company (NYSE: BHGE) and Schlumberger (NYSE: SLB) have been in a general downtrend ever since oil prices peaked in mid-2014. With oil prices hovering around the break-even point for many exploration and production companies, spending has been restrained throughout the energy space. But with the shares of these two industry giants now roughly 66% lower than they were five years ago, is a buying opportunity emerging?

A little background

With a $25 billion market cap, Baker Hughes is roughly half the size of Schlumberger. Still, they are both giants in the energy services space with long histories and broad, global product offerings. Baker Hughes, in fact, likes to describe itself as a "fullstream provider" since it spans the upstream (drilling), midstream (pipelines), and downstream (chemicals and refining) spaces.

Image source: Getty Images.

Schlumberger's services are varied, but it's best known for its drilling and reservoir characterization businesses. One thing that sets the company apart from peers is its market dominance. It holds leadership positions in an impressive number of market niches. That's one big reason the company has been able to grow so large. Although its size and history within the industry are impressive, there really isn't a winner on this point. Investors with a preference might find themselves leaning one way or the other.

Another important issue to watch here is the balance sheet, noting that oil prices are highly volatile. And while these two companies aren't directly reliant on oil prices, their customers are. On this score, Baker Hughes looks a little better, with a long-term debt-to-equity ratio of 0.15 compared with Schlumberger's 0.31. That said, despite being twice as high, Schlumberger's ratio is not unreasonable. And the companies' debt-to-EBITDA ratios are roughly the same. Baker Hughes has an edge, but not by much.

SLB Financial Debt to Equity (Quarterly) data by YCharts. TTM = trailing 12 months.

As hinted above, earnings and revenues will vary along with oil prices, since that is what helps dictate demand. There's no way around this. Still, it is hard to make an earnings comparison between the two names because Baker Hughes has existed in its current form for only a few years. Which brings us to some big issues for investors to consider.

Really notable differences

The single biggest factor for investors to monitor is the ownership stake that financially troubled General Electric (NYSE: GE) has in Baker Hughes. That stake is the remnant of the complicated merger and spinoff deal that created Baker Hughes, a GE Company, in 2017. As of the first quarter, GE owned roughly half of the energy services company. While that's down from around 62% -- and is slated to go to zero over time -- GE's weak financial state has made some market watchers question the timing of its Baker Hughes disposition efforts.

Basically, GE needs cash and appears to be making decisions from a position of weakness. Until it is on stronger financial ground, there will be lingering concerns on Wall Street about every move it makes. Since its Baker Hughes stake is a notable asset that it plans to sell, Baker Hughes stock will be facing big headwinds until GE is out of the picture, or until it lays out an actual plan for the disposition of its shares. This by itself is a good reason to avoid Baker Hughes today.

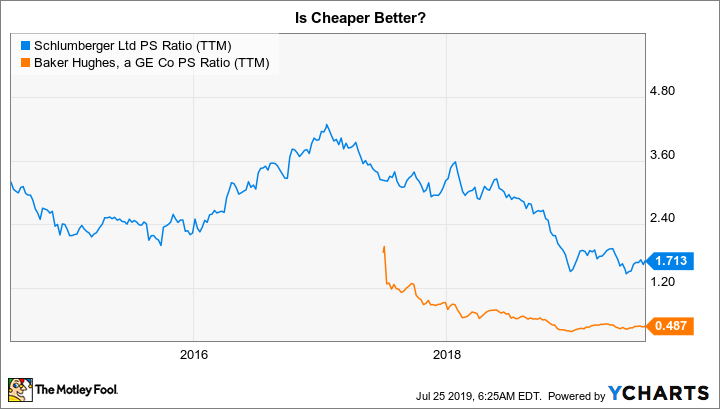

SLB PS Ratio (TTM) data by YCharts.

However, this overhang has actually created a bit of a disparity. Baker Hughes' price-to-sales ratio is roughly 0.5 times, versus 1.7 for Schlumberger, whose five-year average is roughly 2.8 times. So the giant energy services company looks relatively cheap historically. However, Baker Hughes looks even cheaper. The same general trend is true for price to book value and price to cash flow, as well. Baker Hughes has an edge here.

Should you pick either one?

Because of the volatility inherent in the energy services industry, most investors are probably better off avoiding both Baker Hughes and Schlumberger. But if this is a sector you want to invest in, then you need to make a call between Schlumberger, an industry giant that's working through a difficult market (like it has many times before), and Baker Hughes, which is facing the same industry headwinds as well as the overhang created by its relationship with General Electric. Although Baker Hughes looks relatively cheap, it's probably best for most investors to go with Schlumberger, at least until GE is out of the picture. There's no need to take on more risk than already exists within the industry.

More From The Motley Fool

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

This article was originally published on Fool.com