Cypress' (CY) Q2 Earnings and Revenues Surpass Estimates

Cypress Semiconductor Corporation CY delivered second-quarter 2018 non-GAAP earnings of 33 cents beating the Zacks Consensus Estimate by 4 cents. The figure surged 57.1% on a year-over-year basis and 22.3% sequentially.

Revenues came in $624.1 million, surpassing the Zacks Consensus Estimate of $620 million. The figure also exhibited year-over-year growth of 5.1% and quarter-over-quarter improvement of 7.2%.

The company’s robust product portfolio aided management in executing the strategy for delivering the package of connect, compute and store solutions which in in turn drove year-over-year growth. Further, Cypress witnessed improving demand for its products and stability in the order patterns of its customers during the quarter.

Moreover, proper execution of Cypress’ 3.0 strategy which is focused on delivering embedded solutions for consumer, automotive and industrial customers of all sizes as well as strong performance contributed significantly to the second quarter results.

Since the second-quarter earnings, share price of the company have grown 6.04%. This can be primarily attributed to solid operating results and improved outlook for the next quarter.

Notably, shares of Cypress have returned 18.6% on a year-to-date basis, outperforming the industry’s rally of 6.4%.

Quarter in Detail

In order to strengthen presence in the industrial and automotive markets, Cypress deepened its focus toward enhancement of wireless connectivity solutions during the quarter. The company also partnered with Semtech to co-develop a two-chip LoRaWAN-based module for smart city applications. Further, Cypress acquired a customer named Pioneer for its automotive-grade Wi-Fi and Bluetooth combo solutions.

Further, considering the growth opportunities of USB-C, the company unveiled 7-port USB-C hub controller for notebook and tablet docking stations and monitor docks.

Cypress also continued with the further expansion of NOR Flash product portfolio by introducing Semper NOR Flash memory family which helps the developers in building fail-safe embed automotive systems by meeting the automotive industry’s functional safety standard.

Top-line in Detail

By Business Unit: Cypress reports in two organised segments — Microcontroller and Connectivity Division (“MCD”) and Memory Products Division (“MPD”).

MCD: This segment generated $368.5 million revenues (59% of total revenues), improved 2.2% year over year and 9.4% from the previous quarter. The figure came slightly below the Zacks Consensus Estimate of $370 million. The company witnessed strong performance of its wireless IoT business within this segment. This was primarily driven by robust Bluetooth Wi-Fi combo solution that contributed 55% to revenues generated by wireless IoT business. Further, the microcontroller business performed well and exhibited growth of 7% from the year-ago quarter. Additionally, strong demand pattern for PSoC products remained positive.

MPD: Cypress generated $255.6 million revenues (41% of revenues) from this segment, up 4.1% sequentially and 9.6% on a year-over-year basis. The figure also surpassed the Zacks Consensus Estimate of $248 million. Improving demand by industrial and internet infrastructure, especially 4.5G and 5G customer for the company’s flash memory product drove top-line growth.

By End-Market: The company operates in four high growth markets — Industrial, Automotive, Consumer and Enterprise end markets.

Industrial: The company generated 19% of its revenues from this market, which expanded 100 basis points (bps) sequentially but contracted 20 bps year over year. Cypress experienced strong performance of PSoC and flash memory products which aided revenue generation in this end-market.

Automotive: This market generated 30.8% of total revenues, remaining flat with the year-ago quarter but contracted 320 bps from the last quarter. Strong performance of product and solutions portfolio which includes NOR memory, MCU and touch interface solutions supported the company in generating revenues from this segment. NOR Flash continued to gain momentum in ADAS systems and MCU solutions gained traction with Traveo II controller in the instrument cluster market. Additionally, 802.11ac combo solution coupled with RSDB (real-time simultaneous dual band) technology aided the company in attracting customers from high-growth infotainment areas.

Consumer: Cypress generated 31.3% of revenues from this market, expanding 30 bps sequentially but contracted 280 bps year over year. The company sustained momentum in this market with the help of its 28-nanometer 11ac connectivity solutions and 40-nanometer PSoC 6. Additionally, Cypress continued to experience winning platform designs in the smart home and wearable applications space which drove the results within this segment.

Enterprise: Cypress generated 18.9% of revenues from this market, which expanded 190 bps sequentially and 300 bps on a year-over-year basis. The building of 5G stations globally is aiding top-line growth in this segment.

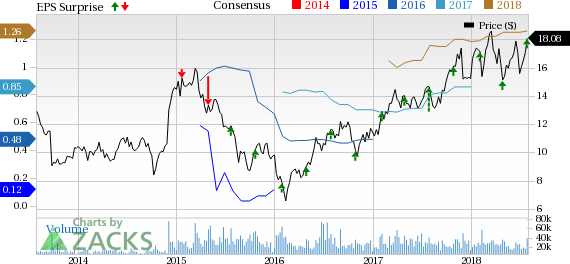

Cypress Semiconductor Corporation Price, Consensus and EPS Surprise

Cypress Semiconductor Corporation Price, Consensus and EPS Surprise | Cypress Semiconductor Corporation Quote

Operating Details

For the second quarter, Cypress’ gross margin was 46.3%, increasing 40 bps sequentially and 540 bps from the prior-year quarter. The impressive year-over-year improvement in gross margin can be attributed to favorable product mix.

Further, the company’s cost stringent strategies and growing Fab 25 loadings that led to 83% improvement in utilization from the last quarter also contributed well.

Operating margin came in 22.3%, expanded 690 bps from the year-ago quarter and 280 bps on a sequential basis.

Per the company, operating expenses were $183.3 million, down 0.2% year over year but up 3.8% from the previous quarter. The year-over-year fall was a result of decrease in selling, general & administrative expenses which outweighed the increase in research and development expenses.

Balance Sheet and Cash Flows

As of Jul 1, 2018, cash, cash equivalents and short-term investments totaled $112.7 million compared with $106.7 million as of Apr 1, 2018. Accounts receivables were nearly $404.5 million, increased from $393.3 million in the previous quarter.

Inventory grew to $286.8 million, increasing from $275.4 million in the last reported quarter.

Cypress generated $110.7 million cash from operations improved massively from $31.7 million in the last quarter and $32.4 million in the year-ago quarter.

CapEx was $25.6 million in the quarter under review.

The company also paid quarterly dividend of $39.4 million or 11 cents per share which was up 1.8% sequentially and 8.8% year over year.

Guidance

For third-quarter 2018, Cypress expects revenues in the range of $655-$685 million. The Zacks Consensus Estimate for revenues is pegged at $652.9 million.

Further, non-GAAP earnings for the next quarter are anticipated in a range of 36-40 cents. The Zacks Consensus Estimate is projected at 34 cents.

The company anticipates non-GAAP gross margin between 46.5% and 47.5%.

Zacks Rank and Stocks to Consider

Cypress carries a Zacks Rank #3 (Hold).

Some better-ranked stocks in the broader technology sector are Micron Technology MU, Analog Devices A and Stoneridge SRI. While Micron Technology sports a Zacks Rank #1 (Strong Buy), Analog Devices and Stoneridge carry a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Long-term earnings growth rate for Micron Technology, Analog Devices and Stoneridge is pegged at 8.18%, 12.4% and 8.5%, respectively.

Wall Street’s Next Amazon

Zacks EVP Kevin Matras believes this familiar stock has only just begun its climb to become one of the greatest investments of all time. It’s a once-in-a-generation opportunity to invest in pure genius.

Click for details >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cypress Semiconductor Corporation (CY) : Free Stock Analysis Report

Stoneridge, Inc. (SRI) : Free Stock Analysis Report

Micron Technology, Inc. (MU) : Free Stock Analysis Report

Agilent Technologies, Inc. (A) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research