DCP Midstream (DCP) Q4 Earnings Beat, Revenues Decline Y/Y

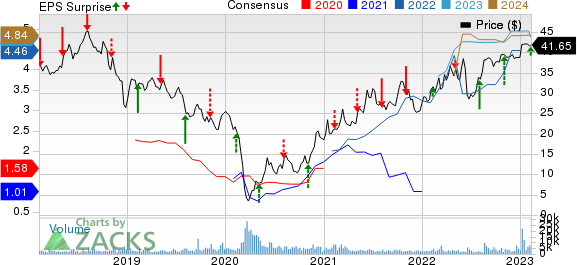

DCP Midstream, LP DCP reported fourth-quarter adjusted earnings of $1.13 per unit, which beat the Zacks Consensus Estimate of $1.05. The bottom line declined from the year-ago quarter’s earnings of $1.44 per unit.

Total quarterly revenues of $3,030 million beat the Zacks Consensus Estimate of $2,027 million. However, the top line declined from $3,477 million in the year-ago quarter.

The better-than-expected quarterly results were driven by favorable NGL and gas marketing results, and tariffs on NGL pipelines. The positives were partially offset by higher operating and maintenances expenses.

DCP Midstream Partners, LP Price, Consensus and EPS Surprise

DCP Midstream Partners, LP price-consensus-eps-surprise-chart | DCP Midstream Partners, LP Quote

Operations

Logistics and Marketing

This segment of DCP Midstream recorded adjusted EBITDA of $209 million in the fourth quarter, up from the year-ago period’s $161 million. Favorable NGL and gas marketing results, and tariffs on NGL pipelines aided the segment.

The average NGL pipeline throughput in the quarter was 687 thousand barrels per day (Mbpd), lower than the year-ago quarter’s 692 Mbpd. Fractionator throughputs were recorded at 56 Mbpd, declining from 57 Mbpd in the year-ago quarter.

Gathering and Processing

The segment reported adjusted EBITDA of $235 million for the fourth quarter, down from $237 million in the year-ago quarter. Higher operating and maintenance expenses hurt the segment.

Average natural gas wellhead volumes in the quarter rose to 4,430 million cubic feet per day (MMcf/d) from the year-ago period’s 4,151 MMcf/d. NGL gross production totaled 418 Mbpd, up from 417 Mbpd.

Total Expenses

Purchases and related costs declined year over year in the quarter under review. Operating and maintenance expenses rose to $195 million from $177 million in the fourth quarter of 2021.

Total operating costs and expenses were $2,860 million, down from the year-ago quarter’s figure of $3,225 million.

Financials

In fourth-quarter 2022, total growth capital expenditures, acquisition and equity investments were $59 million. Sustaining capital in the quarter was $59 million. DCP generated an excess free cash flow of $62 million in the reported quarter.

At the end of the fourth quarter, DCP Midstream reported long-term debt of $4,357 million. Cash and cash equivalents were $1 million. It had current debt of $506 million.

Zacks Rank & Stocks to Consider

DCP Midstream currently carries a Zacks Rank #3 (Hold).

Investors interested in the energy sector might look at stocks like Marathon Petroleum Corporation MPC and RPC Inc. RES, each sporting a Zacks Rank #1 (Strong Buy), and Murphy USA Inc. MUSA, carrying a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Marathon Petroleum’s adjusted earnings per share of $6.65 comfortably beat the Zacks Consensus Estimate of $5.54. The bottom line was favorably impacted by the stronger-than-expected performance of its key Refining & Marketing segment.

In the fourth quarter, MPC repurchased $1.8 billion of shares and a further $700 million worth of shares this year till Jan 27. Marathon Petroleum, which gave an additional $5 billion share repurchase approval, currently has a remaining authorization of $7.6 billion.

RPC’s adjusted earnings of 41 cents per share in the fourth quarter beat the Zacks Consensus Estimate of 30 cents. The strong quarterly results were backed by higher activity levels in all the service lines and rising equipment utilization.

As of Dec 31, RPC had cash and cash equivalents of $126.4 million, up sequentially from $73.2 million. Nonetheless, the company managed to maintain a debt-free balance sheet.

Murphy USA’s fourth-quarter 2022 earnings per share of $5.21 missed the Zacks Consensus Estimate of $6.16. The underperformance could be attributed to lower-than-expected petroleum product sales.

Murphy USA projects 2023 fuel volume in a range of 240 to 245 thousand gallons on an APSM basis. Further, Murphy USA’s 2023 guidance includes up to 45 new stores and up to 30 raze-and-rebuilds and $795-$815 million in merchandise margin contribution.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Murphy USA Inc. (MUSA) : Free Stock Analysis Report

Marathon Petroleum Corporation (MPC) : Free Stock Analysis Report

RPC, Inc. (RES) : Free Stock Analysis Report

DCP Midstream Partners, LP (DCP) : Free Stock Analysis Report