Deutsche Bank: 3 ‘Strong Buy’ Giants to Consider Ahead of Earnings

Brexit in the UK, and a brewing border war in Syria. Missile strikes on Saudi Arabian refineries, and global warming ... everywhere.

Investors have had no lack of things to worry about in the global economy lately -- and that's probably a big part of the reason the S&P 500 is down 2% since this month began. Lately, investor worries have found a new center of focus in China, where trade negotiations between the U.S. and that country have taken a(nother) turn for the worse.

Not only are new 30% US tariffs on $250 billion in Chinese goods about to kick into effect on October 15. This week, the US Commerce Department announced a new blacklisting of 28 Chinese companies and organizations over allegations of Uighur persecution, putting new trade talks at risk.

Where is an investor to turn for safety in a world like this? Asking the TipRanks Stock Screener for some answers, we find many Wall Street analysts think you're best off sticking with "the usual suspects." No matter how bad things get for the world at large, Deutsche Bank analysts, in particular, still think that strong buy-rated tech giants Amazon, Alphabet, and Facebook each of which reports earnings this month -- will come out on top in the end. Let's take a closer look:

Amazon (AMZN)

The first of these tech giants to report will be Amazon, with Q3 earnings expected to arrive just two weeks from now, on October 24. That sounds like good news, but investors may need to be careful about this one.

On the one hand, analysts who track Amazon's fortunes are optimistic about revenues, predicting that Amazon's sales will surge more than 21% year over year to tip the scales at $68.8 billion. On the other hand, though, profits could come as a bit of a shock. The consensus estimate right now is that Amazon will earn only $4.57 per share for the quarter -- more than a 20% drop from last year's Q3.

Despite this prospect, 5-star Deutsche Bank analyst Lloyd Walmsley issued a bullish report on Amazon, reiterating the bank's "buy" rating on the shares and predicting the shares will top $2,450 a year from now -- 42% more than they sell for today. (To watch Walmsley's track record, click here)

What makes Walmsley so optimistic? "We ... think AWS related sales and marketing investment in 1H should pay dividends helping stabilize AWS growth in 2H," argues the analyst, referring to Amazon Web Services, the source of only 11% of Amazon's revenue ... but 59% of its profits. Although some investors are worried about the higher costs Amazon plans to incur in offering 1-day shipping service to its retail customers, Walmsley thinks a small sacrifice of "near term margins" in the service of winning faster sales growth through "1-day prime" is a trade-off worth making.

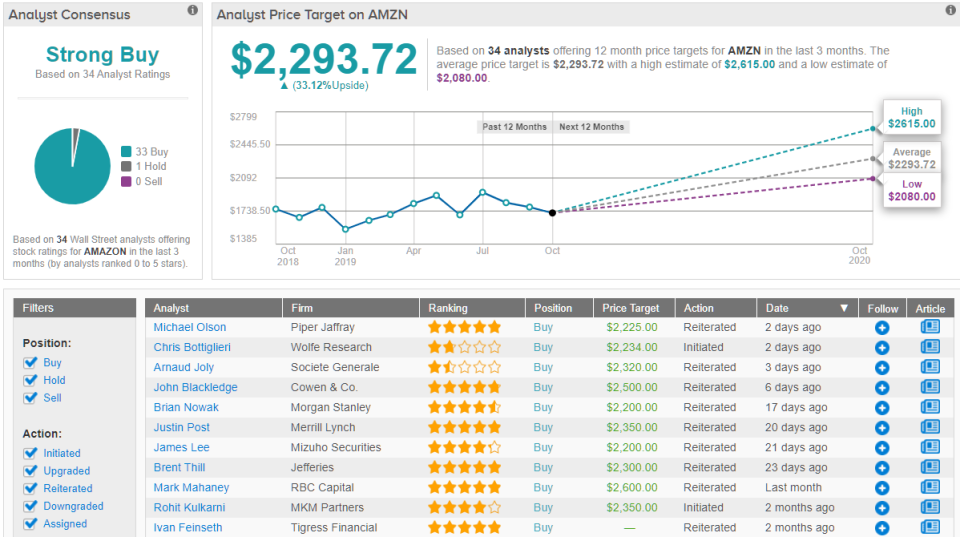

All in all, the retail giant looks like a very compelling investing opportunity, as TipRanks analytics showcasing AMZN as a "strong buy." With an average price target of $2,293.72, analysts are predicting an upside potential of 33% for the stock. In total, Amazon stock has received 33 "buy" ratings vs. just one "hold" rating in the past three months. (See Amazon stock analysis on TipRanks)

Alphabet (GOOGL)

Next to report will be Alphabet, coming in two days after Amazon with a Q3 report scheduled for October 28 (after close of trading) -- and once again, this could be a tale of sales or earnings growth -- not both.

Consensus projections right now see Google's parent company growing sales nearly 20% year over year. Earnings, however, are expected to suffer a 5% decline to $12.41 per share. So why should you want to own this one and why do most analysts on the Street insist Alphabet is still a "strong buy?"

Once again, Deutsche Bank's Lloyd Walmsley has the answer: "We are bullish on Google" not just in Q3, but "into the second half" and even "2020," because "a strong ad product pipeline [is] starting to kick in." (And as you know, Google's biggest business is selling ads). In particular, the analyst likes the fact that Google is "opening up Google Maps ads" as a new source of revenue.

Additionally, Walmsley believes Google is in line to book "some big deal wins" in its Cloud business, and could give additional insight into how this business is faring with "management seemingly being more open to company disclosures." On top of all this, Alphabet management is showing confidence in itself by "authorizing its biggest share buyback authorization in history."

With that in mind, Walmsley reiterates his own "buy" rating on the stock, and predicts Alphabet shares could go as high as $1,600 -- well ahead of consensus Street estimates, we might add, and potentially enough to give new buyers a 33% profit on their investment. (See Google stock analysis on TipRanks)

Facebook (FB)

Bringing up the rear in this month's cavalcade of gigantic tech stock reports, Facebook will release its Q3 earnings on October 30 -- also after close of trading -- and here, at long last, is where investors should get some unalloyed good news.

Not only are analysts enthused about Facebook's revenues, which are expected to grow 26.5% year over year, but they think earnings should go up as well -- from $1.76 a year ago, to $1.91 in this month's report. And by this point, you won't be surprised to hear that Deutsche's Lloyd Walmsley has an opinion on this one as well:

"We expect solid 3Q results at Facebook with upside potential to our top-line projections for 3Q ad revs +29% ex-FX," says the analyst. The bad news is that if sales might beat expectations, Walmsley worries that "EPS estimates" going forward could in fact "migrate lower" when Q3's news comes out.

But he's not too worried, even about that. The fact that Facebook's profits might not grow as fast as analysts' published projections indicate, says Walmsley, "is one of the worst kept secrets on the Internet," and not a reason to avoid the stock. Once expectations are officially recalibrated towards the $9.45 per share that Walmsley thinks Facebook will actually earn next year, "we think the story looks good for 2020," with "more associated advertising, ramping monetization" and "continued resurgence in core Facebook ad spend, growing revenue in marketplace and a call option with Facebook Watch."

Long story short, Deutsche's official position is that Facebook stock, too, is a "buy."

Other analysts share a similar enthusiasm with Deutsche when it comes to Facebook. TipRanks data shows out of 35 analysts, 30 are bullish and 5 are sidelined. With a consensus price target of $236.07, the potential upside is about 31%. (See Facebook stock analysis on TipRanks)