How Does Sinostar PEC Holdings Limited (SGX:C9Q) Fare As A Dividend Stock?

Is Sinostar PEC Holdings Limited (SGX:C9Q) a good dividend stock? How can we tell? Dividend paying companies with growing earnings can be highly rewarding in the long term. If you are hoping to live on the income from dividends, it's important to be a lot more stringent with your investments than the average punter.

With a 2.7% yield and a nine-year payment history, investors probably think Sinostar PEC Holdings looks like a reliable dividend stock. A low yield is generally a turn-off, but if the prospects for earnings growth were strong, investors might be pleasantly surprised by the long-term results. Some simple research can reduce the risk of buying Sinostar PEC Holdings for its dividend - read on to learn more.

Click the interactive chart for our full dividend analysis

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. Comparing dividend payments to a company's net profit after tax is a simple way of reality-checking whether a dividend is sustainable. Looking at the data, we can see that 24% of Sinostar PEC Holdings's profits were paid out as dividends in the last 12 months. We'd say its dividends are thoroughly covered by earnings.

Another important check we do is to see if the free cash flow generated is sufficient to pay the dividend. Last year, Sinostar PEC Holdings paid a dividend while reporting negative free cash flow. While there may be an explanation, we think this behaviour is generally not sustainable.

Is Sinostar PEC Holdings's Balance Sheet Risky?

As Sinostar PEC Holdings has a meaningful amount of debt, we need to check its balance sheet to see if the company might have debt risks. A rough way to check this is with these two simple ratios: a) net debt divided by EBITDA (earnings before interest, tax, depreciation and amortisation), and b) net interest cover. Net debt to EBITDA is a measure of a company's total debt. Net interest cover measures the ability to meet interest payments. Essentially we check that a) the company does not have too much debt, and b) that it can afford to pay the interest. Sinostar PEC Holdings is carrying net debt of 4.57 times its EBITDA, which is getting towards the upper limit of our comfort range on a dividend stock that the investor hopes will endure a wide range of economic circumstances.

Net interest cover can be calculated by dividing earnings before interest and tax (EBIT) by the company's net interest expense. Sinostar PEC Holdings has EBIT of 5.57 times its interest expense, which we think is adequate.

Consider getting our latest analysis on Sinostar PEC Holdings's financial position here.

Dividend Volatility

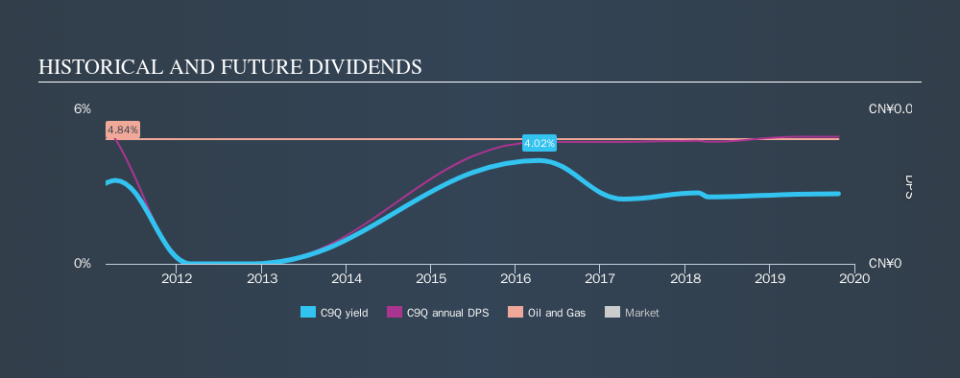

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. The first recorded dividend for Sinostar PEC Holdings, in the last decade, was nine years ago. Although it has been paying a dividend for several years now, the dividend has been cut at least once by more than 20%, and we're cautious about the consistency of its dividend across a full economic cycle. During the past nine-year period, the first annual payment was CN¥0.026 in 2010, compared to CN¥0.025 last year. Dividend payments have shrunk at a rate of less than 1% per annum over this time frame.

We struggle to make a case for buying Sinostar PEC Holdings for its dividend, given that payments have shrunk over the past nine years.

Dividend Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Strong earnings per share (EPS) growth might encourage our interest in the company despite fluctuating dividends, which is why it's great to see Sinostar PEC Holdings has grown its earnings per share at 17% per annum over the past five years. Earnings per share are growing at a solid clip, and the payout ratio is low. We think this is an ideal combination in a dividend stock.

Conclusion

When we look at a dividend stock, we need to form a judgement on whether the dividend will grow, if the company is able to maintain it in a wide range of economic circumstances, and if the dividend payout is sustainable. Firstly, the company has a conservative payout ratio, although we'd note that its cashflow in the past year was substantially lower than its reported profit. Next, earnings growth has been good, but unfortunately the dividend has been cut at least once in the past. Ultimately, Sinostar PEC Holdings comes up short on our dividend analysis. It's not that we think it is a bad company - just that there are likely more appealing dividend prospects out there on this analysis.

See if management have their own wealth at stake, by checking insider shareholdings in Sinostar PEC Holdings stock.

We have also put together a list of global stocks with a market capitalisation above $1bn and yielding more 3%.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.