Is Editas Medicine (NASDAQ:EDIT) A Risky Investment?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Editas Medicine, Inc. (NASDAQ:EDIT) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Editas Medicine

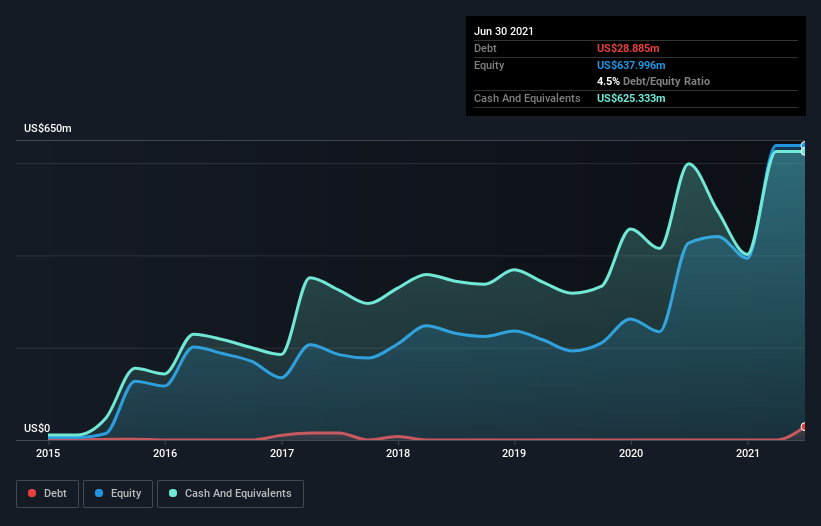

What Is Editas Medicine's Net Debt?

The image below, which you can click on for greater detail, shows that at March 2021 Editas Medicine had debt of US$28.9m, up from none in one year. But on the other hand it also has US$625.3m in cash, leading to a US$596.4m net cash position.

How Healthy Is Editas Medicine's Balance Sheet?

The latest balance sheet data shows that Editas Medicine had liabilities of US$64.0m due within a year, and liabilities of US$78.3m falling due after that. On the other hand, it had cash of US$625.3m and US$672.0k worth of receivables due within a year. So it can boast US$483.7m more liquid assets than total liabilities.

This surplus suggests that Editas Medicine has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, Editas Medicine boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Editas Medicine's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Editas Medicine wasn't profitable at an EBIT level, but managed to grow its revenue by 149%, to US$81m. So there's no doubt that shareholders are cheering for growth

So How Risky Is Editas Medicine?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that Editas Medicine had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through US$180m of cash and made a loss of US$167m. While this does make the company a bit risky, it's important to remember it has net cash of US$596.4m. That means it could keep spending at its current rate for more than two years. The good news for shareholders is that Editas Medicine has dazzling revenue growth, so there's a very good chance it can boost its free cash flow in the years to come. While unprofitable companies can be risky, they can also grow hard and fast in those pre-profit years. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 3 warning signs for Editas Medicine you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.