How Should Investors React To Layne Christensen Company’s (NASDAQ:LAYN) CEO Pay?

Mike Caliel took the reins as CEO of Layne Christensen Company’s (NASDAQ:LAYN) and grew market cap to USD$244.35M recently. Understanding how CEOs are incentivised to run and grow their company is an important aspect of investing in a stock. Incentives can be in the form of compensation, which should always be structured in a way that promotes value-creation to shareholders. Today we will assess Caliel’s pay and compare this to the company’s performance over the same period, as well as measure it against other US CEOs leading companies of similar size and profitability. Check out our latest analysis for Layne Christensen

Did Caliel create value?

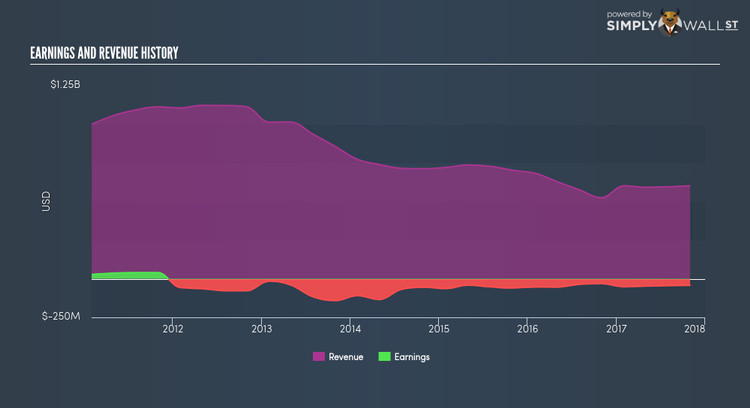

Profitability of a company is a strong indication of LAYN’s ability to generate returns on shareholders’ funds through corporate activities. In this exercise, I will use profits as a proxy for Caliel’s performance. Over the last year LAYN produced negative earnings of -$41.9M , which is a further decline from prior year’s loss of -$31.7M. Moreover, on average, LAYN has been loss-making in the past, with a 5-year average EPS of -$2.53. In the situation of unprofitability the company may be facing a period of reinvestment and growth, or it can be a signal of some headwind. Regardless, CEO compensation should represent the current condition of the business. In the most recent financial report, Caliel’s total compensation declined by -6.91%, to $2,166,670. Moreover, Caliel’s pay is also made up of 46.15% non-cash elements, which means that variabilities in LAYN’s share price can move the actual level of what the CEO actually takes home at the end of the day.

Is LAYN’s CEO overpaid relative to the market?

Though no standard benchmark exists, as remuneration should be tailored to the specific company and market, we can gauge a high-level benchmark to see if LAYN is an outlier. This outcome helps investors ask the right question about Caliel’s incentive alignment. Normally, a US small-cap has a value of $1B, generates earnings of $96M, and remunerates its CEO at roughly $2.7M annually. Typically I would use earnings and market cap to account for variations in performance, however, LAYN’s negative earnings lower the usefulness of my formula. Analyzing the range of remuneration for small-cap executives, it seems like Caliel is remunerated sensibly relative to peers. Putting everything together, even though LAYN is loss-making, it seems like the CEO’s pay is reflective of the appropriate level.

What this means for you:

Are you a shareholder? My conclusion is that Caliel is not being overpaid. But your role as a shareholder should not end here. As above, this is a relatively simplistic calculation using high-level benchmarket. Proactive shareholders should question their representatives (i.e. the board of directors) how they think about the CEO’s incentive alignment with shareholders and how they balance this with retention and reward. To find out more about LAYN’s governance, look through our infographic report of the company’s board and management.

Are you a potential investor? Although remuneration can be a useful gauge of whether Caliel’s incentives are well-aligned with LAYN’s shareholders, it is certainly not sufficient to base your investment decision solely on this factor. Whether the company is fundamentally strong depends on LAYN’s financial health and its future outlook. To research more about these fundamentals, I recommend you check out our simple infographic report on LAYN’s financial metrics.

PS. If you are not interested in Layne Christensen anymore, you can use our free platform to see my list of over 50 sustainable companies producing great returns.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.