Pilgrim's Pride (PPC) Q4 Earnings Beat Estimates, Sales Up Y/Y

Pilgrim's Pride Corporation PPC reported fourth-quarter 2021 results, with the top and the bottom line increasing year over year. Earnings in the quarter surpassed the Zacks Consensus Estimate.

However, the company has been battling input cost inflation, pandemic-induced volatility, supply chain disruptions and labor shortages. That said, focus on the Customer strategy along with robust diversified portfolio are aiding.

Pilgrim's Pride Corporation Price and EPS Surprise

Pilgrim's Pride Corporation price-eps-surprise | Pilgrim's Pride Corporation Quote

Q4 in Detail

The company reported adjusted earnings of 56 cents a share, up from 25 cents reported in the year-ago quarter. Quarterly earnings surpassed the Zacks Consensus Estimate of 40 cents.

This producer, marketer and distributor of fresh, frozen and value-added chicken and pork products, generated net sales of $4,038.8 that increased 29.5% from the year-ago quarter’s levels. Sales reflect 20.6% organic growth and a 9.4% contribution from the acquisition of Pilgrim's Food Masters (concluded in September 2021). Net sales increased in Mexico, Europe as well as in the U.S. operations.

Net sales in the U.S. operations amounted to $2,399 million, up from $1,876.2 million reported in the year-ago quarter. Adjusted EBITDA across the U.S. region was $265 million, up from $74.9 million reported in the year-ago quarter.

Management stated that in the U.S. market, retail sales were flat year over year. In the U.S. Prepared Foods business, sales rose more than 50% and volumes jumped 7%.

Mexico operations generated net sales of $426.7 million in the reported quarter, up from $392.5 million in the prior-year quarter. Volumes across Mexico increased 3.4%. In Mexico, adjusted EBITDA was $27 million, down from $77.7 million reported in the year-ago quarter.

Net sales from Europe operations rose to $1,213 million from $849.2 million in the quarter under review. The company highlighted that its Moy Park business and poultry initiatives continue to face major cost increases and labor challenges. Apart from the pandemic-led absences, post-Brexit rules have been causing worker-related problems. In Europe, adjusted EBITDA came in at $24.7 million, down from $52.8 million reported in the year-ago quarter.

Pilgrim's Pride’s cost of sales increased to $3,686.3 million from $2,890.4 million reported in the year-ago quarter. Gross profit climbed to $352.5 million from $227.4 million. Adjusted EBITDA came in at $316.7 million, up from $205.4 million reported in the year-ago quarter. Adjusted EBITDA margin increased to 7.8% from 6.6% recorded in the prior-year quarter.

Image Source: Zacks Investment Research

Other Financial Details

Pilgrim's Pride ended the quarter with cash and cash equivalents of $427.7 million, long-term debt (less current maturities) of $3,191.2 million and total shareholders’ equity of $2,588.9 million. The company generated $326.5 million of cash from operating activities for the year ended Dec 26, 2021.

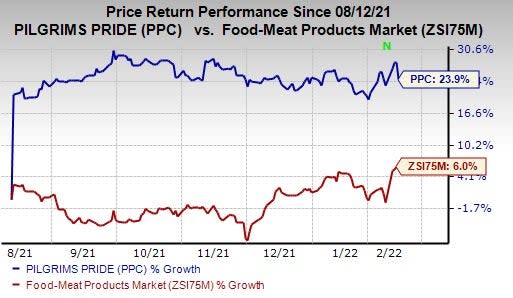

Shares of this Zacks Rank #2 (Buy) company have increased 23.9% in the past six months compared with the industry’s growth of 6%.

Looking for Solid Food Stocks? Check These

Some more better-ranked stocks are Tyson Foods, Inc. TSN, Flowers Foods FLO and Medifast, Inc. MED

Tyson Foods, a meat provider, currently sports a Zacks Rank #1 (Strong Buy). Shares of Tyson Foods have dropped 22.3% in the past six months. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Tyson Foods’ current financial year sales suggests growth of 9.5% from the year-ago reported number. TSN has a trailing four-quarter earnings surprise of 32.2%, on average.

Flowers Foods, which produces and markets packaged bakery products, carries a Zacks Rank #2 (Buy). Shares of Flowers Foods have moved up 22.8% in the past six months.

The Zacks Consensus Estimate for Flowers Foods' 2022 financial year sales suggests growth of 2.1% from the year-ago reported number. FLO has a trailing four-quarter earnings surprise of 15.4%, on average.

Medifast, the manufacturer and distributor of weight loss, weight management, healthy living products and other consumable health and nutritional products, currently carries a Zacks Rank #2. Shares of Medifast have declined 19.2% in the past six months.

The Zacks Consensus Estimate for Medifast’s current financial year sales and EPS suggests growth of about 63% and 49.3%, respectively, from the year-ago reported figure. MED has a trailing four-quarter earnings surprise of 17.3%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tyson Foods, Inc. (TSN) : Free Stock Analysis Report

Flowers Foods, Inc. (FLO) : Free Stock Analysis Report

Pilgrim's Pride Corporation (PPC) : Free Stock Analysis Report

MEDIFAST INC (MED) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research