Pinduoduo Inc. Just Reported And Analysts Have Been Cutting Their Estimates

It's been a sad week for Pinduoduo Inc. (NASDAQ:PDD), who've watched their investment drop 11% to US$32.82 in the week since the company reported its annual result. The statutory results were mixed overall, with revenues of CN¥30b in line with analyst forecasts, but losses of CN¥6.04 per share, some 7.9% larger than analysts were predicting. Earnings are an important time for investors, as they can track a company's performance, look at what top analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We've gathered the most recent statutory forecasts to see whether analysts have changed their earnings models, following these results.

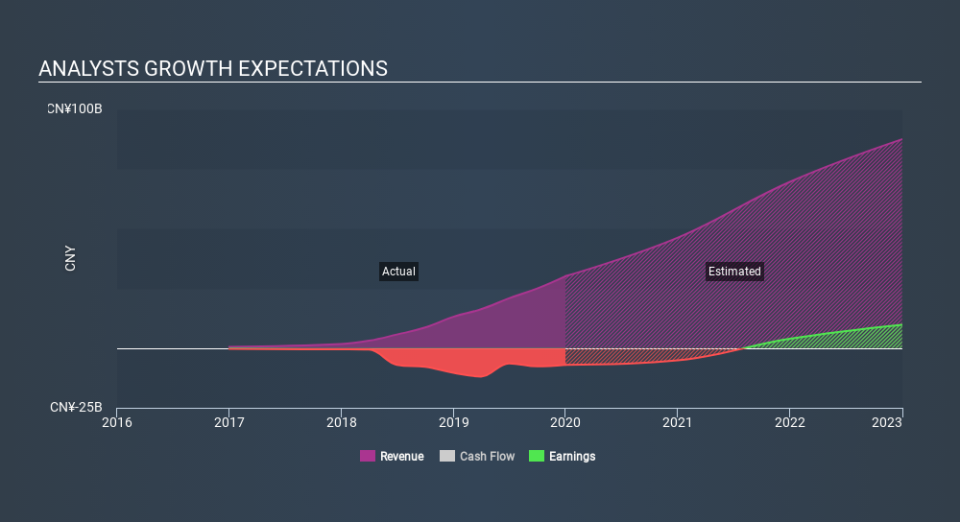

Check out our latest analysis for Pinduoduo

After the latest results, the 25 analysts covering Pinduoduo are now predicting revenues of CN¥46.3b in 2020. If met, this would reflect a huge 54% improvement in sales compared to the last 12 months. Statutory losses are forecast to balloon 31% to CN¥4.16 per share. Yet prior to the latest earnings, analysts had been forecasting revenues of CN¥49.9b and losses of CN¥2.59 per share in 2020. From this we can that analyst sentiment has definitely become more bearish after the latest results, leading to lower revenue forecasts and a large cut to earnings per share estimates.

The average analyst price target was broadly unchanged at CN¥283, perhaps implicitly signalling that the weaker earnings outlook is not expected to have a long-term impact on the valuation. The consensus price target just an average of individual analyst targets, so - considering that the price target changed, it would be handy to see how wide the range of underlying estimates is. There are some variant perceptions on Pinduoduo, with the most bullish analyst valuing it at CN¥508 and the most bearish at CN¥146 per share. We would probably assign less value to the analyst forecasts in this situation, because such a wide range of estimates could imply that the future of this business is difficult to value accurately. As a result it might not be possible to derive much meaning from the consensus price target, which is after all just an average of this wide range of estimates.

Further, we can compare these estimates to past performance, and see how Pinduoduo forecasts compare to the wider market's forecast performance. We would highlight that Pinduoduo's revenue growth is expected to slow, with forecast 54% increase next year well below the historical 85%p.a. growth over the last three years. By way of comparison, other companies in this market with analyst coverage, are forecast to grow their revenue at 16% next year. Even after the forecast slowdown in growth, it seems obvious that analysts still thinkPinduoduo will grow faster than the wider market.

The Bottom Line

The most important thing to take away is that analysts reduced their loss per share estimates for next year, perhaps highlighting increased optimism around Pinduoduo's prospects. Unfortunately analysts also downgraded their revenue estimates, although industry data suggests that Pinduoduo's revenues are expected to grow faster than the wider market. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. We have forecasts for Pinduoduo going out to 2022, and you can see them free on our platform here.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.