Quanta (PWR) Gains From Carbon-Neutral Drive Amid Challenges

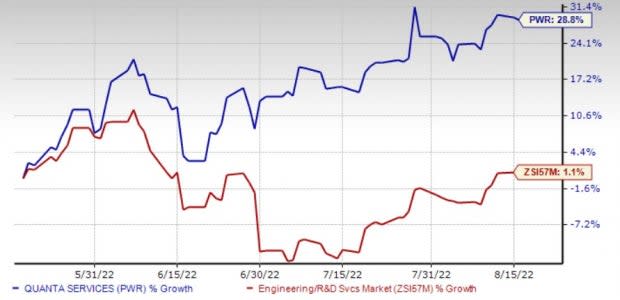

Quanta Services Inc.’s PWR shares have been riding high since the release of its second-quarter 2022 results. Ever since this Zacks Rank #3 (Hold) company reported quarterly numbers on Aug 4, its shares have risen 6.7%, outperforming the industry’s growth of 4.8%. The company has been capitalizing on megatrends to lead the energy transition and enable technological development. Initiatives toward a reduced-carbon economy continue to drive demand for PWR’s services and depict incremental growth opportunities. These factors have helped the company to gain 28.8% over the past three months, outperforming the industry’s 1.1% rise.

Notably, Quanta reported robust financial numbers in second-quarter 2022. Adjusted earnings and revenues increased 45.2% and 41.1% year over year, respectively. This marked the ninth consecutive quarter of earnings beat. Moreover, revenues surpassed the Zacks Consensus Estimate in six out of nine consecutive quarters. Notably, Quanta generated record revenues in the second quarter, exceeding $4 billion for the first time in history and achieved strong double-digit growth of adjusted EBITDA and adjusted earnings per share, which is reflective of the benefits of operations portfolio strategy and strategic capital deployment.

However, Quanta remains vulnerable to supply-chain disruptions, regulatory challenges and risks like project delays and stiff competition.

Image Source: Zacks Investment Research

Factors Favoring the Stock

Infrastructural Push for Energy Transition: Development and deployment of technology solutions across the full spectrum of decarbonization efforts, including carbon management mitigation and compliance consulting, as well as all facets of infrastructure for providing carbon-free energy solutions, will benefit the company going forward. Notably, PWR continues to experience growing demand for renewable generation and infrastructure solutions in 2023 and beyond, giving continued confidence in its multi-year financial targets.

Quanta remains uniquely positioned to capitalize on the megatrends and opportunities to lead the energy transition and enable technological development with initiatives such as electric vehicle charging infrastructure and undergrounding of electrical infrastructure gaining momentum.

As a result, Quanta envisions to deliver a 10% organic adjusted EPS compound annual growth rate (“CAGR”) and more than 15% adjusted EPS CAGR through 2026.

Upbeat View for 2022: Given solid performance in the first half of 2022, coupled with record 12-month backlog, ongoing active customer discussions and robust end-market dynamics, the company now envisions earnings per share in the band of $6.10-$6.44 for 2022 (versus $6.00-$6.50 expected earlier) compared with $4.90 per share reported in the year-ago period. It expects adjusted (non-GAAP) earnings between $6.10 and $6.44 versus $6.00-$6.50 expected earlier. Adjusted EBITDA is now projected within $1.64-$1.71 billion versus $1.60-$1.71 billion expected earlier. Quanta’s full-year non-GAAP free cash flow projection is pegged at $550-$750 million.

The Zacks Consensus Estimate for 2022 earnings of $6.26 per share calls for 27.2% year-over-year growth.

Solid Backlog: The company ended second-quarter 2022 with a record total backlog of $19.85 billion and 12-month backlog of $11.58 billion. This compares favorably with $16.98 billion of total backlog and $8.98 billion of 12-month backlog a year ago. This demonstrates the strength of its core operations. Quanta’s optimism stems from healthy backlog levels, which are expected to grow further.

Strong Electric Power Operations: Electric Power operations continued to perform well from a top-line perspective. Segment revenues, which comprise revenues from base business activities, including communications operations, which grew 24.2% in first-half 2022, 17.9% in 2021 and 9.1% in 2020 from the comparable year-ago period. Solid performance was backed by base business activities, courtesy of robust spending by electric utilities on grid modernization and infrastructure hardening, particularly in the western United States, as well as by gas utilities on distribution system modernization and safety programs.

As of Jun 30, 2022, the segment’s 12-month backlog was $6.38 billion (up from $5.56 billion a year ago), and the total backlog was $11.72 billion (up from $11.29 billion reported in the prior-year quarter). Prospects of the Electric Power segment remain robust, given customers’ investment in grid modernization programs intended to address the aging infrastructure, strengthen systems for resiliency against extreme weather conditions and support long-term economic growth.

Hurdles

The global pandemic-related impediments like project delays are undeniable and unavoidable. During second-quarter 2022, margins of the Electric Power segment were impacted by normal project variability and somewhat by inefficiencies attributable to supply-chain disruptions impacting certain operations and elevated consumables costs.

Factors like supply chain disruptions, inflation, COVID-19 and regulatory uncertainties are causes of concern.

3 Top-Ranked Construction Stocks Hogging the Limelight

Better-ranked stocks, which warrant a look in the Construction sector, include Arcosa ACA, United Rentals URI and Primoris Services Corporation PRIM. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Arcosa — sporting a Zacks Rank #1 — is a manufacturer of infrastructure-related products and services which serves construction, energy and transportation markets.

ACA’s expected earnings growth rate for fiscal 2022 is 7.8%. The Zacks Consensus Estimate for current-year earnings has improved 13.7% over the past 30 days.

United Rentals — currently carrying a Zacks Rank #2 (Buy) — is the largest equipment rental company in the world.

URI’s expected earnings growth rate for 2022 is 40.7%. The Zacks Consensus Estimate for current-year earnings has improved 5.4% over the past 30 days.

Primoris — a Zacks Rank #2 company — is a specialty contractor company operating in the United States and Canada. A robust backlog level of more than $4 billion and solid contract awards in the Energy/Renewables and Utilities segments depict incredible momentum in the future despite the supply chain and permitting challenges. Utility-scale solar projects continued to drive the progress of the Energy/Renewables segment.

Primoris’ earnings for 2022 are expected to grow by 18.4%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Quanta Services, Inc. (PWR) : Free Stock Analysis Report

United Rentals, Inc. (URI) : Free Stock Analysis Report

Primoris Services Corporation (PRIM) : Free Stock Analysis Report

Arcosa, Inc. (ACA) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research