Taylor Morrison Home Corporation (NYSE:TMHC): The Best Of Both Worlds

Building up an investment case requires looking at a stock holistically. Today I’ve chosen to put the spotlight on Taylor Morrison Home Corporation (NYSE:TMHC) due to its excellent fundamentals in more than one area. TMHC is a financially-healthy company with a a great track record of performance, trading at a discount. Below is a brief commentary on these key aspects. For those interested in digger a bit deeper into my commentary, read the full report on Taylor Morrison Home here.

Very undervalued with excellent balance sheet

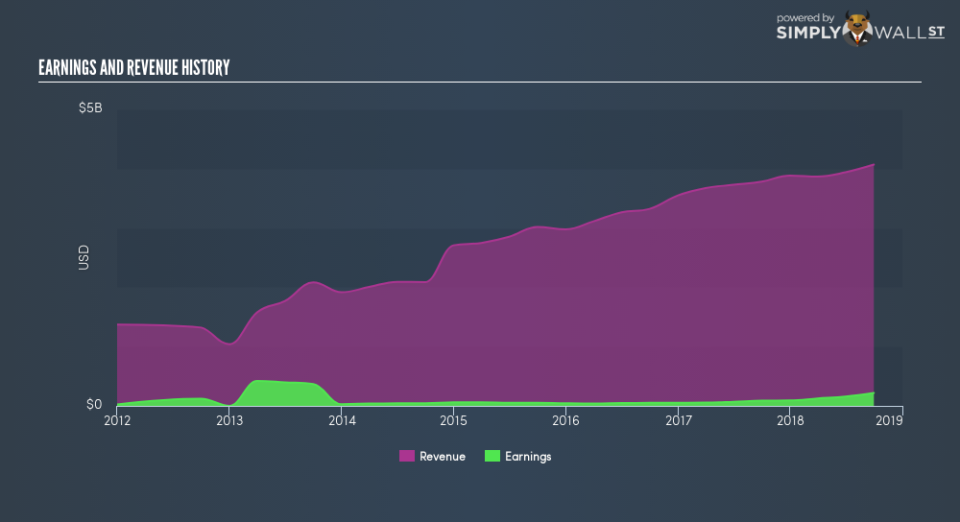

TMHC delivered a triple-digit bottom-line expansion over the past couple of years, with its most recent earnings level surpassing its average level over the last five years. Not only did TMHC outperformed its past performance, its growth also surpassed the Consumer Durables industry expansion, which generated a 17% earnings growth. This is what investors like to see! TMHC’s strong financial health means that all of its upcoming liability payments are able to be met by its current cash and short-term investment holdings. This indicates that TMHC has sufficient cash flows and proper cash management in place, which is a crucial insight into the health of the company. TMHC seems to have put its debt to good use, generating operating cash levels of 0.21x total debt in the most recent year. This is also a good indication as to whether debt is properly covered by the company’s cash flows.

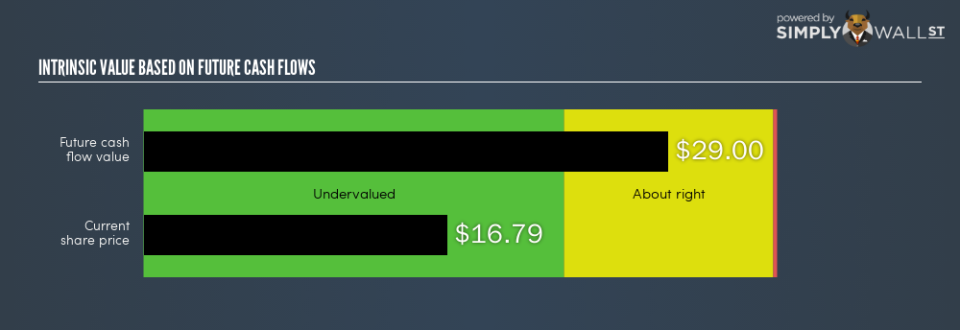

TMHC’s share price is trading at below its true value, meaning that the market sentiment for the stock is currently bearish. This mispricing gives investors the opportunity to buy into the stock at a cheap price compared to the value they will be receiving, should analysts’ consensus forecast growth be correct. Also, relative to the rest of its peers with similar levels of earnings, TMHC’s share price is trading below the group’s average. This supports the theory that TMHC is potentially underpriced.

Next Steps:

For Taylor Morrison Home, I’ve compiled three fundamental factors you should further examine:

Future Outlook: What are well-informed industry analysts predicting for TMHC’s future growth? Take a look at our free research report of analyst consensus for TMHC’s outlook.

Dividend Income vs Capital Gains: Does TMHC return gains to shareholders through reinvesting in itself and growing earnings, or redistribute a decent portion of earnings as dividends? Our historical dividend yield visualization quickly tells you what your can expect from TMHC as an investment.

Other Attractive Alternatives : Are there other well-rounded stocks you could be holding instead of TMHC? Explore our interactive list of stocks with large potential to get an idea of what else is out there you may be missing!

To help readers see past the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price-sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned. For errors that warrant correction please contact the editor at editorial-team@simplywallst.com.