Should You Be Tempted To Sell Winmark Corporation (NASDAQ:WINA) Because Of Its PE Ratio?

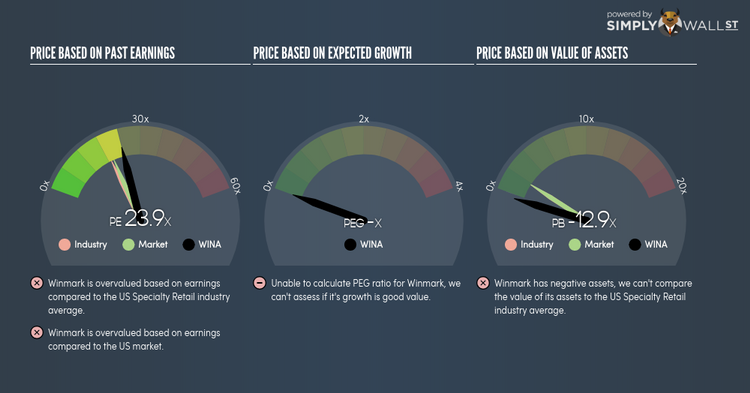

Winmark Corporation (NASDAQ:WINA) is trading with a trailing P/E of 23.9x, which is higher than the industry average of 18.9x. While WINA might seem like a stock to avoid or sell if you own it, it is important to understand the assumptions behind the P/E ratio before you make any investment decisions. In this article, I will deconstruct the P/E ratio and highlight what you need to be careful of when using the P/E ratio. See our latest analysis for Winmark

What you need to know about the P/E ratio

The P/E ratio is a popular ratio used in relative valuation since earnings power is a key driver of investment value. It compares a stock’s price per share to the stock’s earnings per share. A more intuitive way of understanding the P/E ratio is to think of it as how much investors are paying for each dollar of the company’s earnings.

P/E Calculation for WINA

Price-Earnings Ratio = Price per share ÷ Earnings per share

WINA Price-Earnings Ratio = $133.15 ÷ $5.579 = 23.9x

The P/E ratio itself doesn’t tell you a lot; however, it becomes very insightful when you compare it with other similar companies. Our goal is to compare the stock’s P/E ratio to the average of companies that have similar attributes to WINA, such as company lifetime and products sold. A common peer group is companies that exist in the same industry, which is what I use. Since WINA’s P/E of 23.9x is higher than its industry peers (18.9x), it means that investors are paying more than they should for each dollar of WINA’s earnings. As such, our analysis shows that WINA represents an over-priced stock.

Assumptions to be aware of

Before you jump to the conclusion that WINA should be banished from your portfolio, it is important to realise that our conclusion rests on two assertions. The first is that our “similar companies” are actually similar to WINA, or else the difference in P/E might be a result of other factors. For example, if you compared higher growth firms with WINA, then its P/E would naturally be lower since investors would reward its peers’ higher growth with a higher price. The second assumption that must hold true is that the stocks we are comparing WINA to are fairly valued by the market. If this does not hold true, WINA’s lower P/E ratio may be because firms in our peer group are overvalued by the market.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.