2 ‘Strong Buy’ Penny Stocks With Massive 300% Upside Potential — Or More

When searching for risk/reward plays, look no further than penny stocks. These names trading for under $5 per share are considered to be some of the most controversial on the Street, and divide market watchers into two factions: critics and fans.

The former brings a valid argument to the table. Stocks don’t just end up trading at such low levels; typically, there’s a very real reason for their bargain price tags. This can be weak fundamentals or headwinds that are too strong to overcome.

As for the latter, the potential for an investment worth only pocket change to appreciate even a seemingly insignificant amount, the result of which could be massive percentage gains, is too enticing to ignore. Not to mention the low share price means you can carve out a bigger stake for less money upfront.

The implication for investors? Due diligence is essential, as some penny stocks might not have what it takes to climb their way back up.

Taking all of this into consideration, we used TipRanks’ database to pinpoint two penny stocks that have amassed enough analyst support to earn a ‘Strong Buy’ consensus rating. Adding to the good news, each pick boasts over 300% upside potential.

Codexis, Inc. (CDXS)

We’ll start with Codexis, a biotech firm and a leader in enzyme engineering technology. Enzymes are proteins that facilitate chemical and biological reactions in living cells, making it possible for these reactions to take place in the confined spaces within cells. They are essential for metabolic functioning, aiding in the synthesis of necessary substances and the breakdown of others. In short, enzymes play a vital role in life processes, making them a natural focus for biotherapeutic and pharmaceutical companies.

Codexis has a proprietary platform called CodeEvolver, which is used to discover, develop, and enhance novel enzymes to address the challenges associated with the biopharmaceutical industry. Small-molecule pharmaceutical manufacturing, nucleic acid synthesis, and gene sequencing all offer potential therapeutic applications that can benefit from enzymatic actions. Codexis focuses on creating enzymes that improve therapeutic production yields, reduce energy consumption and waste in manufacturing processes, and enhance the sensitivity and effectiveness of end-result therapeutics.

The company is currently pursuing two major research tracks. The first of these, the build-out of the RNAi synthesis platform, has high potential to boost efficiency and lower costs for pharmaceutical companies. There are more than 300 RNAi therapies under development in the biotech ecosystem, making this a rich field for Codexis to enter.

The second major research track involved the clinical trial program for CDX-7108. This is a potential treatment for exocrine pancreatic insufficiency, under development in partnership with Nestle Health Sciences. The company has already released positive interim results from the Phase 1 trial, and is currently preparing a Phase 2 trial, scheduled for the first half of next year.

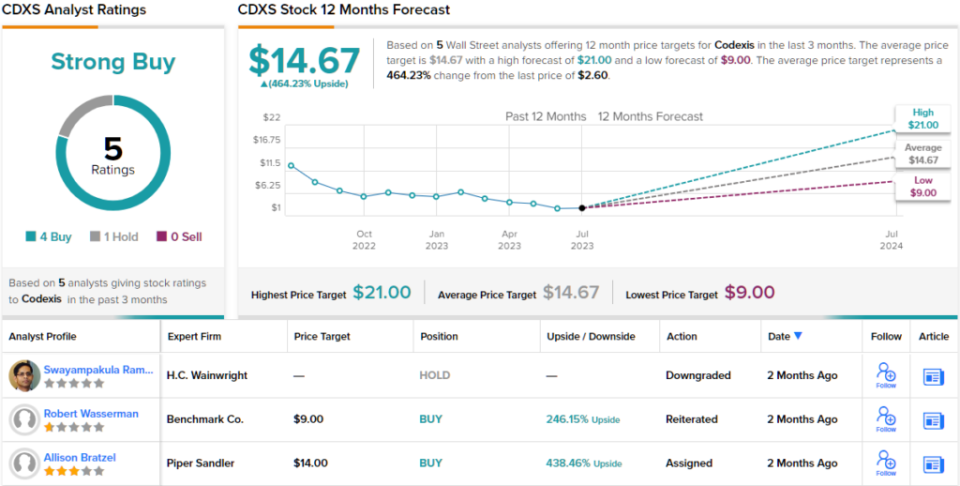

With key catalysts ahead, Piper Sandler analyst Allison Bratzel believes that at $2.60 apiece, now is the time to pull the trigger on CDXS.

“We see the opportunities in the company’s RNAi synthesis capabilities and biotherapeutics efforts, rather than the legacy business, as the primary drivers of value and reasons to own CDXS… More specifically, we think the November update, where management expects to demonstrate gram-scale synthesis capabilities, and/or a potential R&D day ~YE23/early-’24 will provide a more comprehensive view of the market opportunity/strategy for the [RNAi synthesis] platform. As for biotherapeutics, IND filing for CDX-7108 is on track for YE23, which will enable P2 trial initiation 1H24. We view presentation/publication of full clinical data from the P1 proof-of-concept trial in 2H23, as well as finalization of the Nestlé commercialization agreement as key catalysts ahead of the anticipated ~2025 P2 readout,” Bratzel noted.

“We continue to think the stock can work as these key drivers come into better focus in coming quarters. Remain buyers,” the analyst summed up.

Bratzel backs up her bullish stance with an Overweight (i.e. Buy) rating on the stock, while her $14 price target suggests a robust one-year upside potential of 438%. (To watch Bratzel’s track record, click here)

Similarly, other analysts are in CDXS’ corner. 4 Buys and 1 Hold assigned in the last three months add up to a ‘Strong Buy’ consensus rating. With an average price target of $14.67, the upside potential comes in at 464%. (See CDXS stock forecast)

CorMedix (CRMD)

The second penny stock we’ll look at is CorMedix, another biopharma company. CorMedix is working on new treatments for infectious and/or inflammatory diseases, with particular attention to the prevention, reduction, and treatment of infection due to intravenous catheterization. IV catheters are used in a number of medical procedures, and bring with them a substantial risk of infection at the needle site – CorMedix’ leading product, DefenCath, is a proprietary combination of two medications, taurolidine and heparin, intended for use as a catheter-lock solution for the prevention of catheter-related bloodstream infections (CRBSIs).

CorMedix is studying DefenCath for use in patients undergoing hemodialysis with the use of central venous catheters. This is a life-saving procedure for patients with kidney failure, but the central venous catheter (CVC) comes with serious risk of systemic infection.

DefenCath uses a broad antimicrobial activity to prevent catheter infection, and has proven to be effective in clinical trials. However, CorMedix made several NDA submissions to the FDA, and received two complete response letters (CRLs) due to ‘deficiencies’ at a contracted manufacturing plant for the necessary heparin. The last rejection was in August of 2022, and CorMedix worked to address the issues cited. In May of this year, the company submitted its third NDA – and in late June received the FDA’s acceptance of the NDA, with a PDUFA target date set for this coming November 15.

The ubiquity of IV catheters in the medical field presents a rich opportunity for DefenCath, and the FDA’s recent acceptance of the NDA is an important step forward. This is the thesis laid out by Jason Butler, in his note for JMP.

“We are encouraged by the continued progress towards DefenCath approval and remain confident that all outstanding items from the CRL have been fully resolved… Management noted that it is continuing to ramp launch preparations, and we believe the compelling clinical results and market readiness activities the company has already advanced, most notably in-patient reimbursement and healthcare economic data, well position the launch for success,” Butler opined.

Looking ahead, Butler gives CorMedix an Outperform (i.e. Buy) rating, and he sets a $19 price target to indicate potential for ~393% upside in the next 12 months. (To watch Butler’s track record, click here)

Butler is not the only analyst to see a solid upside here; all three of this stock’s recent reviews are positive, for a Strong Buy consensus rating. The shares are priced at $3.90 and the $16.67 average target suggests an upside of ~327% from that level. (See CRMD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.