These 2 ‘Strong Buy’ Penny Stocks Have Massive Upside Potential, Says Oppenheimer

Let’s talk about penny stocks. These are equities that trade for less than $5 per share, at the very bottom of the price range. While they are priced that low for a reason – and the reasons may vary – a low price in itself doesn’t mean that the stock’s fundamentals are sour. Smart investors can find some true bargains among penny stocks and set themselves up for outsized gains.

The opportunity is linked to a simple question: Why is the company’s stock priced so low? If the answer is mainly benign (a reaction to a new share offering or an unexpected capital expenditure), then investors have a chance to buy in at a bargain price. The key is learning to recognize when a low-cost stock is sound versus unsound.

The bottom line? Doing some research is necessary before pulling the trigger on any penny stock. Following the recommendations from Wall Street pros can help in the due diligence process.

Bearing this in mind, we used the TipRanks database to take a look at two penny stocks getting rave reviews from Oppenheimer analyst Francois Brisebois, with the firm’s analyst projecting massive upside potential for each. The platform also revealed that both boast a “Strong Buy” consensus rating from the rest of the Street. Let’s take a closer look.

Durect Corporation (DRRX)

We’ll start with Durect Corporation, a clinical- and commercial-stage biotech firm working on new therapeutic agents based on epigenetic regulation. This is a promising pathway in the treatment of disease, aimed at treating organ injuries due to chronic conditions that cause or are associated with dysregulations of the epigenome. Mitigation of such dysregulation has high potential to alter the disease course and to provide genuine improvement for patients’ conditions.

The company’s leading drug candidate, larsucosterol (DUR-928), has shown the ability to improve compromised cellular function and regulate the expression of multiple genes involved in cellular function. Durect is currently studying larsucosterol in the randomized Phase 2b AHFIRM trial for the treatment of alcohol-associated hepatitis (AH). Enrollment in the trial has been completed, and the company announced in September that the last patient visit had been conducted. Top-line results from AHFIRM are expected to be released during 4Q23.

Larsucosterol has already shown positive results in an uncontrolled Phase 2a clinical trial in the treatment of AH, as well as in an open-label Phase 1b trial in the treatment of nonalcoholic steatohepatitis (NASH). The company is continuing to investigate larsucosterol for additional indications and is pursuing new drug candidates to bring into the research pipeline.

All of this makes Durect a solid biotech for investors to consider, according to Oppenheimer’s Francois Brisebois.

“We believe DRRX is undervalued due to larsucosterol’s (DUR-928) opportunity in AH alone… Given AH’s prevalence (~158,000 AH hospitalizations in the US), high 90-day mortality rate (~30% in severe AH), and no viable treatments, we believe the market is primed for larsucosterol. Based on safety/efficacy seen in the successful P2a, we believe P2b is slightly derisked, given trial design similarities (albeit notable differences: severe-AH only, equivalent primaries: mortality or liver transplant),” Brisebois opined.

“While larsucosterol remains the primary focus, DRRX plans to enter the oncology space with its new chemical entities. We are closely monitoring progress as the company has internally developed multiple novel small-molecule DNMT inhibitors with broad spectrum activity against multiple hematologic and solid tumor types. We expect product candidate selection by year-end 2023,” the analyst added.

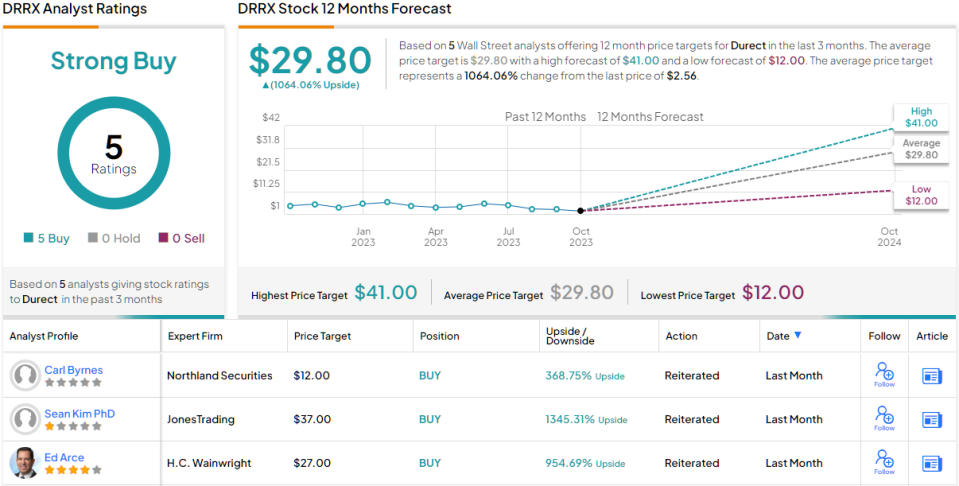

To this end, Brisebois rates DRRX an Outperform (i.e. Buy) along with a $32 price target, which suggests a powerfully robust 12-month upside of 1,130%. (To watch Brisebois’ track record, click here)

Overall, Durect gets a Strong Buy rating from the Street’s analyst consensus, based on 5 unanimously positive reviews. The stock’s $2.58 trading price and $29.80 average price target reflects the high potential of the leading drug candidate – and implies a gain of 1,064% in the coming year. (See DRRX stock forecast)

Ovid Therapeutics (OVID)

Next up is Ovid Therapeutics, a biopharmaceutical company working to develop new medications for the treatment of rare neurological disorders, particularly those causing severe, ongoing epileptic seizures. This is a rich field in biopharmaceutical study, with a potential patient base of approximately 50 million worldwide. Ovid is working on a pipeline of small molecule medications that offer the potential for meaningful improvement in patients’ lives.

Ovid’s approach aims to ameliorate hyperexcited states in neuronal activity and return active neurons to a balanced state, thus preventing manifest neurological symptoms such as one-off seizures or chronic and acute epilepsy. The company’s investigational medicines use mechanisms of action that impact novel or under-addressed biological targets and are possibly first-in-class or best-in-class therapeutic agents.

The company currently has several drug candidates in the pipeline, at both early and late stages of clinical trials. Of the early-stage candidates, OV329 is a GABA-AT inhibitor undergoing a Phase 1 trial with full findings anticipated during 1H 24. OV888 is a novel ROCK2 inhibitor which Ovid is studying in collaboration with Graviton pursuant to a license agreement made earlier this year.

The leading drug candidate, however, is Soticlestat, a first-in-class oral compound designed to inhibit cholesterol-24-hydroxylase (CH24H). Ovid co-developed and out-licensed its rights to Soticlestat to Takeda, and Takeda currently has Soticlestat under investigation in two Phase 3 trials for the treatment of both Lennox-Gastaut syndrome (LGS) and Dravet syndrome (DS).

While Ovid out-licensed its rights to Soticlestat, it retained a financial interest in the drug candidate. In an announcement made yesterday, Ovid announced an agreement with Ligand, in which Ovid received a $30 million up-front payment, and Ligand receives a 13% interest in future royalties and milestones in Soticlestat. Ovid retains an 87% interest in the drug, and the up-front payment extends the company’s cash runway into 2026.

Oppenheimer’s Brisebois sums up Ovid’s potential in his recent note, writing, “With key Soticlestat (out-licensed to TAK) pivotal readouts for Dravet syndrome (DS) and Lennox-Gastaut syndrome (LGS) around the corner (our estimate: 1H24), as well as an overlooked CNS pipeline, we believe OVID’s evolution warrants investor diligence. Given positive P2 (statistically significant reduction in seizures), OLE data (seizure frequency reduction up to two years), and slight adjustments to trial designs, we expect positive P3 pivotal readouts.”

“As up to ~90% of DS and LGS patients remain refractive to standard of care in a polypharmacy treatment paradigm, we believe Soticlestat’s unique MOA and clean safety profile make it an ideal commercial candidate. We believe our peak sales estimate of ~ $1B (US and EU), based on 25% market penetration of refractive patients, is fairly conservative… LGND partnership on Soticlestat royalties further bolsters our confidence in the potential commercial success,” Brisebois added.

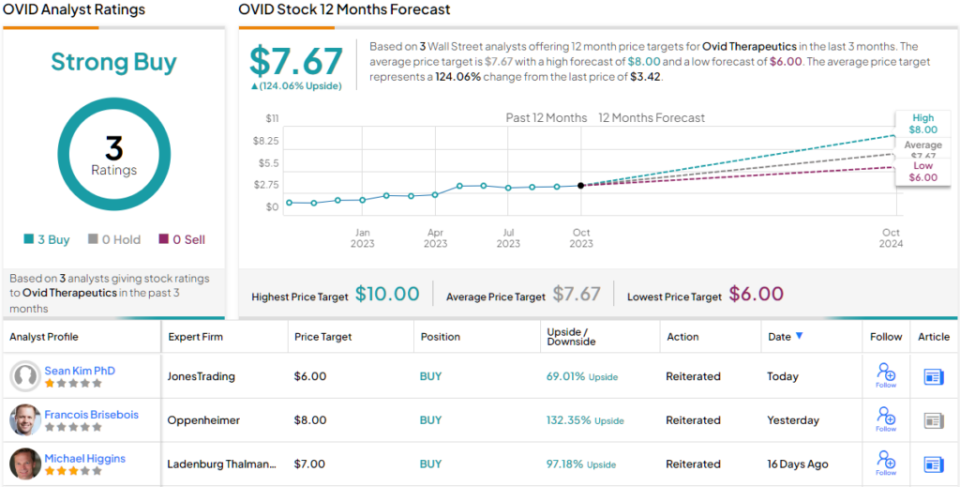

These comments support Brisebois’ stance on OVID shares, which he rates as Outperform (i.e. Buy). His price target here, set at $8 per share, points toward a 132% upside on the one-year time horizon.

The rest of the Street appears to echo Brisebois’ bullish sentiment. As it has racked up 3 Buys and no Holds or Sells, the consensus is unanimous: OVID is a Strong Buy. The current trading price, of $3.42 and the average target price of $7.67 together suggest a potential one-year upside of 124%. (See OVID stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.