2U (NASDAQ:TWOU) Posts Better-Than-Expected Sales In Q3, Gross Margin Improves

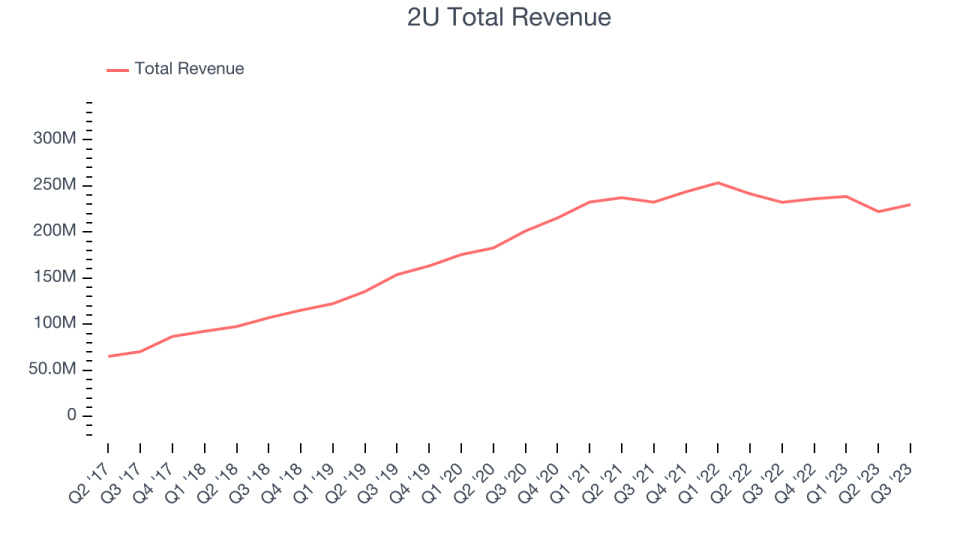

Online education platform, 2U (NASDAQ:TWOU) reported results ahead of analysts' expectations in Q3 FY2023, with revenue down 1.1% year on year to $229.7 million. On the other hand, its full-year revenue guidance of $977.5 million at the midpoint came in slightly below analysts' estimates. Turning to EPS, 2U made a non-GAAP loss of $0.15 per share, improving from its loss of $1.57 per share in the same quarter last year.

Is now the time to buy 2U? Find out by accessing our full research report, it's free.

2U (TWOU) Q3 FY2023 Highlights:

Revenue: $229.7 million vs analyst estimates of $224 million (2.5% beat)

EPS (non-GAAP): -$0.15 vs analyst estimates of -$0.13

The company dropped its revenue guidance for the full year from $990 million to $977.5 million at the midpoint, a 1.3% decrease

Free Cash Flow was -$20.93 million compared to -$27.18 million in the previous quarter

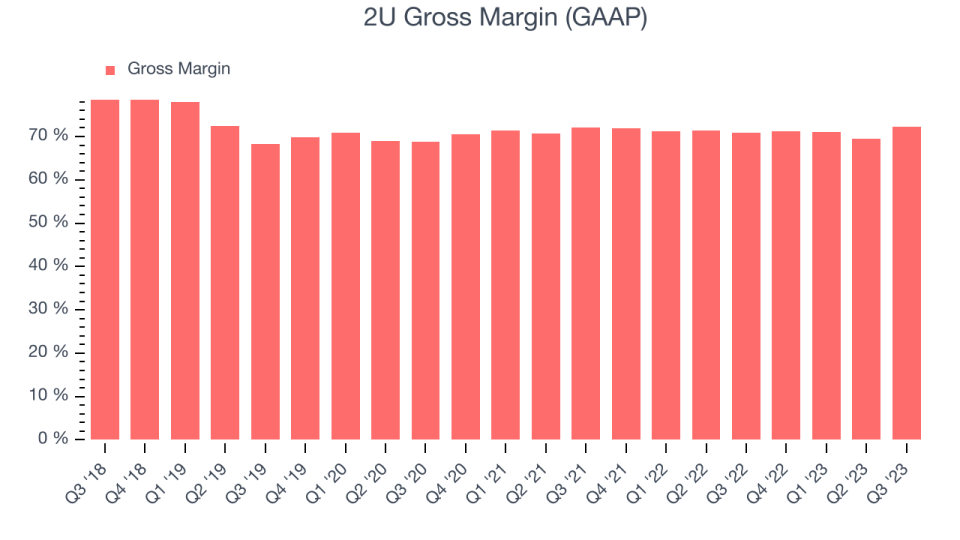

Gross Margin (GAAP): 72.3%, up from 70.9% in the same quarter last year

"Our edX platform uniquely positions us to capitalize on the demand shift to more skill-based courses and the advancements in technology, including AI, with our diverse portfolio of offerings," said Christopher "Chip" Paucek, Co-Founder and Chief Executive Officer of 2U.

Originally named 2tor after the founder's dog Tor, 2U (NASDAQ:TWOU) provides software for universities and colleges to deliver online degree programs and courses.

Education Software

The overwhelming trend of moving work, life and consumption of content online is starting to catch up with the education sector that has until recently stuck to providing courses and degrees in the same way as they did decades ago - in person. The COVID pandemic massively accelerated adoption of online education and has forced institutions to invest in creating digital courses, which drives demand for the software that enables it.

Sales Growth

This quarter, 2U's revenue was down 1.1% year on year, which might disappointment some shareholders.

Looking ahead, analysts covering the company were expecting sales to grow 12.5% over the next 12 months before the earnings results announcement.

The pandemic fundamentally changed several consumer habits. There is a founder-led company that is massively benefiting from this shift. The business has grown astonishingly fast, with 40%+ free cash flow margins. Its fundamentals are undoubtedly best-in-class. Still, the total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Profitability

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. 2U's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 72.3% in Q3.

That means that for every $1 in revenue the company had $0.72 left to spend on developing new products, sales and marketing, and general administrative overhead. Despite improving significantly since the last quarter, 2U's gross margin is still lower than that of a typical SaaS businesses. Gross margin has a major impact on a company’s ability to develop new products and invest in marketing, which may ultimately determine the winner in a competitive market. This makes it a critical metric to track for the long-term investor.

Key Takeaways from 2U's Q3 Results

With a market capitalization of $207.6 million, 2U is among smaller companies, but its more than $41.14 million in cash on hand and near break-even free cash flow margins puts it in a stable financial position.

We enjoyed seeing 2U materially improve its gross margin this quarter. We were also glad its revenue and adjusted EBITDA outperformed Wall Street's estimates, driven by better-than-expected results in its degree program division. Its full-year adjusted EBITDA guidance also cleared estimates. On the other hand, its full-year revenue guidance missed analysts' expectations. In terms of new product launches, 2U announced it will create 80 new degree programs in 2024, which are expected to add $120 million in incremental annual revenue once ramped. Zooming out, we think this was still a decent quarter, showing that the company is staying on track. The stock is flat after reporting and currently trades at $2.35 per share.

So should you invest in 2U right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

The author has no position in any of the stocks mentioned in this report.