It will take months or years to tell if the tax cuts President Trump signed at the end of 2017 will boost economic growth or help create jobs, as intended. But little by little, we’re getting more evidence of what is likely to change under the new tax regime.

Some of the changes will be big. Congress’s Joint Committee on Taxation has published new estimates of the ways people will file their taxes for 2018, the first year most of the new tax provisions will be in effect. Here are 3 big changes:

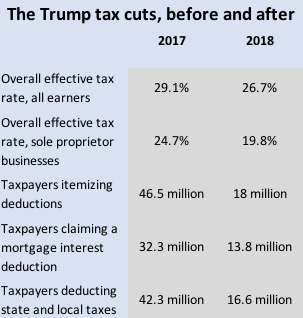

Far fewer people deducting state and local taxes. One of the most disruptive changes to the tax code is a new limit of $10,000 on the deductibility of state and local taxes, which used to be subject to no limit. The JCT estimates the number of people claiming the so-called SALT deduction will drop from 42.3 million for 2017 to 16.6 million for 2018—a 61% decline. For many filers, the new threshold for the SALT deduction means there will be no point itemizing, because their tax bill will end up lower using the standard deduction, which nearly doubled under the new law to $12,000 for individuals. About 7% of filers will end up with a higher tax bill under the new law, in large part because they have a large state and local tax bill and will lose more through the new SALT limit than other provisions of the bill will make up for.

Far fewer people deducting mortgage interest. The JCT predicts the number of taxpayers claiming a mortgage interest deduction will fall from 32.3 million for 2017 to 13.8 million for 2018—a 57% decline. The Trump tax cuts made only one significant change regarding mortgage interest, by lowering the maximum amount of deductible mortgage debt on a new loan from $1 million to $750,000. That affects very few home owners. But the new limit on the SALT deduction, along with the bigger standard deduction, will simply limit the benefits of itemizing for millions of taxpayers.

Overall, the JCT expects the number of taxpayers choosing to itemize, for any reason, to fall from 46.5 million for 2017 to 18 million for 2018 – a 61% drop. For many, that will make filing taxes simpler and cheaper.

There could be unintended consequences, however – changes in the deductibility of mortgage interest could affect home values, over time. The tax break for mortgage interest essentially makes owning a home cheaper, since borrowers earn something akin to a refund on a portion of the interest they pay. So if fewer people claim that deduction, the net cost of home ownership goes up. A lower tax bill, overall, might make it a wash for many home owners. But in some regions or parts of the market, the tax changes might also change the incentives for buying (or selling) a home.

A windfall for businesses. Big businesses known as C corporations will enjoy a 40% reduction in the corporate tax rate, from 35% to 21%. Yahoo Finance and many other news outlets have reported extensively on what big companies are likely to do with the tax savings, with many buying back shares or raising dividends. Some companies, such as Apple, have committed to new investments. And dozens of companies have given employees one-time bonuses.

The JCT research provides new insight on how the tax cuts will benefit smaller businesses. The effective tax rate for sole proprietorships—which account for about 73% of all businesses—will drop from 24.7% to 19.8%, according to the JCT. That’s a hefty 4.9 percentage points, a bigger decline than most individuals will see, since the effective tax rate for individuals is expected to fall from 29.1% in 2017 to 26.7% for 2018, or 2.4 percentage points.

Most privately owned businesses will benefit from the tax cuts, but those owned by the wealthy will benefit the most. The JCT found that 44% of the net benefit of a new tax break for privately owned businesses will accrue to individuals with incomes of $1 million or more, while just 7.5% of the net gain will accrue to individuals with incomes of $100,000 or less.

That skew is both deliberate and problematic. Slashing business taxes is supposed to leave companies with more money to invest in workers and facilities, and wealthier business owners obviously have more income to tax. But there’s no guarantee businesses will invest the windfall in ways that help ordinary people, and many Americans feel the tax cuts favor the wealthy over the working and middle class. If businesses really do amp up spending and hiring, maybe skeptical voters will start to feel they’re getting a bigger share of the tax cuts. But we’re still waiting for convincing signs of that.

Confidential tip line: rickjnewman@yahoo.com. Click here to get Rick’s stories by email.

Read more:

Why a “Democratic wave” could harm stocks

Rick Newman is the author of four books, including Rebounders: How Winners Pivot from Setback to Success. Follow him on Twitter: @rickjnewman

Follow Yahoo Finance on Facebook, Twitter, Instagram, and LinkedIn