3 Dividend Stocks That Pay You More Than Exxon Does

ExxonMobil's (NYSE: XOM) 4% yield makes the stock a popular income investment, but the price often fluctuates with cyclical crude oil prices. For example, the stock's 25% decline over the past five years wiped out any dividend gains for long-term investors.

So today, a trio of our Motley Fool contributors will discuss three stocks that pay higher dividends than Exxon but have more stable growth prospects -- AT&T (NYSE: T), Magellan Midstream Partners (NYSE: MMP), and Tanger Factory Outlet Centers (NYSE: SKT).

Image source: Getty Images.

A dependable dividend aristocrat

Leo Sun (AT&T): AT&T raised its dividend annually for 34 straight years, making it an elite member of the S&P 500's Dividend Aristocrats that raise their payouts for 25 years or more. It currently pays a forward dividend yield of 6.6% and trades at just eight times forward earnings.

AT&T's valuation fell and its yield rose because of the stock's poor growth over the past few years. The growth of its wireless business decelerated, its pay TV business stalled out, and its massive acquisitions of DIRECTV and Time Warner caused its debt levels to soar.

AT&T hasn't resolved all those problems yet, but it's made progress. Its wireless business posted healthy growth last quarter, the inclusion of Time Warner's business boosted its sales, and it reported a gradual reduction of its long-term debt -- which fell from $180 billion last June to $169 billion last quarter.

It expects to generate at least $26 billion in free cash flow, this year, compared with $22.4 billion last year, and it plans to spend about $14 billion of that total on dividends and the rest on extinguishing its debt. That news indicates that AT&T won't lose its Dividend Aristocrat title anytime soon.

Wall Street expects AT&T's revenue to stay flat next year -- after it laps the Time Warner acquisition -- as its earnings rise just 2%. That growth rate seems anemic, but it indicates that AT&T's core business will remain stable as its low P/E and high yield set a floor under the stock.

Another energy play, but without the oil risk

Reuben Gregg Brewer (Magellan Midstream Partners): I own shares of Exxon and think it's a great dividend stock, but commodity prices have a big impact on its performance. The sharp drop in first-quarter results put that issue on clear display. It's reasonable that conservative income investors would want a fat yield but not the commodity risk. That's why Magellan Midstream Partners, and its 6.5% yield, should be on your radar.

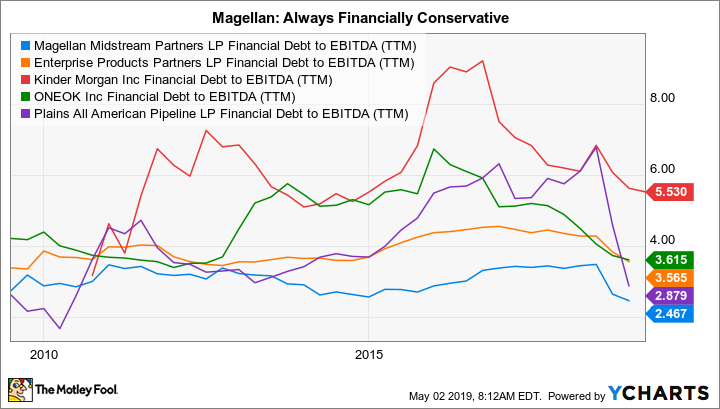

Magellan is a limited partnership that owns the assets that help move oil and gas from where it gets drilled to where end users consume it. It's not a glamorous business, but it is a fairly stable one. As long as oil and natural gas are in demand, Magellan's assets will get used. And, perhaps most important for income investors, over 85% of its top line is fee based. In other words, it gets paid the same amount no matter what commodity prices are doing.

MMP Financial Debt to EBITDA (TTM) data by YCharts

Now add to that a conservative financial profile -- debt to EBITDA is at the low end of the industry, and distribution coverage is targeted at a strong 1.2 -- along with distribution increases every quarter since its 2001 IPO, and a plan to keep growing the distribution by around 5% annually. Magellan's high yield should start to look even more enticing, given that its distribution growth plans are backed by over $1.2 billion in capital spending across 2019 and 2020, with more on the back burner.

If you want a high-yield energy stock in your portfolio but don't like the commodity uncertainty of Exxon's business, take a look at even higher-yielding Magellan today.

A stronghold for brick-and-mortar retail

Steve Symington (Tanger Factory Outlet Centers): Given the astronomical rise of e-commerce, it might seem counterintuitive to put your money to work in a company whose future depends on the brick-and-mortar retail business. But as an outlet center-oriented real estate investment trust, Tanger Factory Outlets still offer consumers compelling value, while -- to borrow the words of CEO Steven Tanger during the most recent quarterly call -- providing retail tenants with "an important, proven, and profitable distribution channel."

That's not to say Tanger hasn't had its challenges. The company has also proved adept at renegotiating leases as needed to keep portfolio occupancy rates high -- occupancy stood at 95.4% at the end of last quarter. Tanger also started this year by divesting four declining non-core properties, giving it more flexibility and boosting resources to focus on more profitable, higher-growth opportunities.

That isn't to say Tanger was desperately raising cash, however. The business generates impressive cash flows, and the stock offers investors a mouthwatering 7.74% annual dividend yield, supported by a healthy 61% payout ratio. With shares trading near a 52-week low, and for investors willing to collect that now-enormous dividend as Tanger continues to steadily position its property portfolio for future growth, I think the stock is a compelling bargain today.

More From The Motley Fool

Leo Sun owns shares of AT&T and Tanger Factory Outlet Centers. Reuben Gregg Brewer owns shares of ExxonMobil and Tanger Factory Outlet Centers. Steve Symington has no position in any of the stocks mentioned. The Motley Fool recommends Magellan Midstream Partners and Tanger Factory Outlet Centers. The Motley Fool has a disclosure policy.