3 International Upstream Stocks Too Alluring to Resist

Post pandemic, operators in the Zacks Oil and Gas - Exploration and Production - International industry are focused heavily on cost-cutting initiatives. Together with their focus on high-quality, high-return assets, the companies are able to capture an attractive return on capital. The sector has uniformly stuck to shareholder return and long-term spending plans, driving equities higher. This positive sentiment supports the potential upside for international exploration and production firms such as Harbour Energy HBRIY, VAALCO Energy EGY and Capricorn Energy CRNCY.

Industry Overview

The Zacks Oil and Gas - International E&P industry consists of companies primarily operating outside the United States and focused on the exploration and production (E&P) of oil and natural gas. These firms find hydrocarbon reservoirs, drill oil and gas wells, and produce and sell these materials to be refined later into products such as gasoline, fuel oil, distillate, etc. The economics of oil and gas supply and demand is the fundamental driver of this industry. In particular, a producer’s cash flow is determined by realized commodity prices. In fact, all E&P companies are vulnerable to historically volatile prices in the energy markets. A change in realizations affects their returns on drilling inventory and causes them to alter production growth rates. These operators are also exposed to exploration risks where drilling results are uncertain.

3 Key Investing Trends to Watch in the Oil and Gas - International E&P Industry

Sustainable Cost-Cutting Efforts: The energy companies have changed their approach to spending capital. Over the past few years, producers have worked tirelessly to cut costs to a bare minimum and look for innovative ways to churn out more oil and gas. And they managed to do just that by improving drilling techniques and extracting favorable terms from the beleaguered service providers. Moreover, driven by operational efficiencies, most E&P operators have been able to reduce unit costs, while the coronavirus-induced collapse in crude forced them to adopt a more disciplined approach to spending capital. These actions are expected to preserve cash flow and support balance sheet strength.

Concerns About Cost Escalation: Most energy companies (including the upstream operators) have been experiencing rising costs in the form of increased expenses related to maintenance and inventory. Despite moderating from record levels, inflation in Europe and the United States remains above threshold levels. This, together with supply-chain tightness, is not only pushing costs higher but also affecting capital programs. Apart from being hard to ignore, escalation in expenses is also drowning out the benefits of any commodity price increase. In our view, the inflation-associated headwinds will continue to challenge growth and margin numbers with little chance of a quick resolution. This may lead to a rough road for oil/gas equities engaged in energy exploration and production.

Prioritizing Shareholder Returns: Despite gyrations in the energy market, upstream operators continue to give back cash to stakeholders. In particular, cash from operations is on a sustainable path, with revenues stabilizing and companies slashing capital expenditures from the pre-pandemic levels amid commodity realizations at a healthy enough level for market participants. To put it simply, efficiency improvements over the past few years helped the E&P firms generate significant “excess cash,” which they intend to use to boost investor returns. In fact, more and more energy companies are allocating their increasing cash pile by way of dividends and buybacks to pacify the long-suffering shareholders.

Zacks Industry Rank Reflects Positive Outlook

The Zacks Oil and Gas – International E&P industry is a 10-stock group within the broader Zacks Oil - Energy sector. It currently carries a Zacks Industry Rank #50, which places it in the top 20% of 250 Zacks industries.

The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates strong near-term prospects. Our research shows that the top 50% of the Zacks-ranked industries outperforms the bottom 50% by a factor of more than 2 to 1.

The industry’s position in the top 50% of the Zacks-ranked industries is a result of an encouraging earnings outlook for the constituent companies in aggregate. Looking at the aggregate earnings estimate revisions, it appears that analysts are becoming optimistic about this group’s earnings growth potential. As a matter of fact, the industry’s earnings estimates for 2024 have gone up 71.4% in the past year.

Considering the encouraging dynamics of the industry, we will present a few stocks that you may want to consider for your portfolio. But it’s worth taking a look at the industry’s shareholder returns and current valuation first.

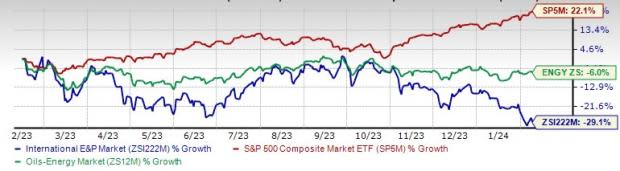

Industry Underperforms Sector & S&P 500

The Zacks Oil and Gas - International E&P industry has fared worse than the broader Zacks Oil - Energy Sector as well as the Zacks S&P 500 composite over the past year.

The industry has fallen 29.1% over this period compared with the broader sector’s decrease of 6%. Meanwhile, the S&P 500 has gained 22.1%.

One-Year Price Performance

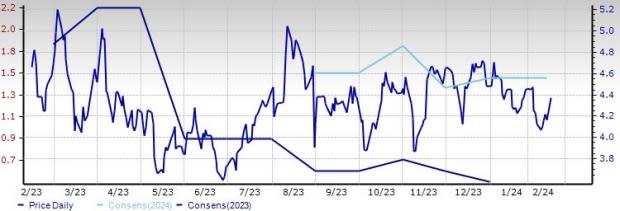

Industry's Current Valuation

Since oil and gas companies are debt-laden, it makes sense to value them based on the EV/EBITDA (Enterprise Value/ Earnings before Interest Tax Depreciation and Amortization) ratio. This is because the valuation metric takes into account not just equity but also the level of debt. For capital-intensive companies, EV/EBITDA is a better valuation metric because it is not influenced by changing capital structures and ignores the effect of non-cash expenses.

On the basis of the trailing 12-month enterprise value-to EBITDA (EV/EBITDA) ratio, the industry is currently trading at 4.65X, significantly lower than the S&P 500’s 13.73X. However, it is higher than the sector’s trailing-12-month EV/EBITDA of 3.65X.

Over the past five years, the industry has traded as high as 16.32X, as low as 2.19X, with a median of 5.03X.

Trailing 12-Month Enterprise Value-to EBITDA (EV/EBITDA) Ratio (Past Five Years)

3 Oil and Gas - International E&P Stocks to Buy

VAALCO Energy: Founded in 1985, VAALCO Energy’s productive capacity is based offshore West Africa, where it focuses on growth through a combination of acquisitions and active drilling. The operator of the Gabon offshore Etame license, EGY is known for its operational excellence and cost discipline, which are expected to generate significant free cash flows at the current strip pricing.

The 2024 Zacks Consensus Estimate for VAALCO Energy’s earnings per share indicates 325.7% year-over-year growth. Valued at around $439.6 million, EGY currently carries a Zacks Rank #1 (Strong Buy). VAALCO Energy’s shares have declined around 6.4% in a year.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Price and Consensus: EGY

Harbour Energy: A pure-play upstream global oil and gas producer, Harbour Energy targets high-return, short-cycle drilling opportunities. The company's robust financial position and strict capital discipline support competitive shareholder returns and the optionality to grow inorganically. Harbour Energy's recent $11.2-billion deal to acquire substantially all of Wintershall Dea AG's upstream assets should expand its asset base significantly.

The 2024 Zacks Consensus Estimate for Harbour Energy’s earnings per share indicates 5,500% year-over-year growth. Valued at around $2.6 billion, HBRIY currently carries a Zacks Rank of 2. Harbour Energy’s shares have dropped around 12.6% in a year.

Price and Consensus: HBRIY

Capricorn Energy: Founded in 1981, Capricorn Energy’s productive capacity is based onshore Egypt, where it focuses on the lower cost rapid payback Western Desert. CRNCY’s attractive asset base and operational efficiency in the country provide it with a competitive advantage in an energy-hungry domestic and regional market.

The 2024 Zacks Consensus Estimate for Capricorn Energy’s earnings per share indicates 95.8% year-over-year growth. Valued at around $142.3 million, CRNCY currently carries a Zacks Rank #2 (Buy). Capricorn Energy’s shares have gone down around 84.2% in a year.

Price and Consensus: CRNCY

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Harbour Energy PLC Sponsored ADR (HBRIY) : Free Stock Analysis Report

Vaalco Energy Inc (EGY) : Free Stock Analysis Report

Capricorn Energy PLC Unsponsored ADR (CRNCY) : Free Stock Analysis Report