3 Reasons to Hold Catalent (CTLT) Stock in Your Portfolio

Catalent, Inc. CTLT is well-poised for growth in the coming quarters, courtesy of its product and service launches over the past few months. The optimism led by a solid fourth-quarter fiscal 2023 performance, along with a slew of strategic deals over the past few months, is expected to contribute further. Catalent’s operation in a competitive landscape and forex fluctuations pose threats.

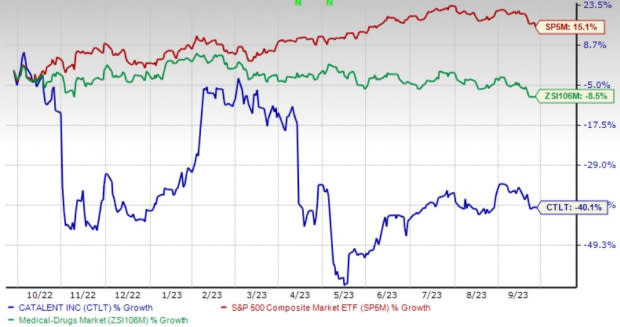

Over the past year, this Zacks Rank #3 (Hold) stock has lost 40.2% compared with the 8.5% decline of the industry. The S&P 500 has witnessed 15.1% growth in the said time frame.

The renowned global developer and supplier of better treatments has a market capitalization of $8.23 billion. Catalent projects 18% growth for the next five years and expects to maintain its strong performance. Catalent’s earnings yield of 1.8% is favorable to the industry’s negative yield.

Image Source: Zacks Investment Research

Let’s delve deeper.

Product and Service Launches: We are upbeat about Catalent’s product and service launches over the past few months. In March, Catalent announced the launch of the ProteoSuite Oral suite, which allows the rational selection of orally developable targeted protein degrader candidates and their advancement into clinical trials. The same month, Catalent announced the expansion of its UpTempo platform process for the development and cGMP (current good manufacturing practices) manufacturing of adeno-associated viral vectors.

Strategic Deals: We are optimistic about Catalent’s robust growth opportunities via its recent tie-ups and buyouts. In August, the company entered into a Cooperation Agreement with Elliott Investment Management L.P., one of Catalent’s investors. This agreement is likely to improve operational efficiencies and drive long-term value.

In March, the company signed a commercial supply agreement with Harm Reduction Therapeutics.

Strong Q4 Results: Catalent’s solid fourth-quarter fiscal 2023 results buoy optimism. The company registered a year-over-year improvement in the Pharma and Consumer Health segment. Management’s confirmation regarding Catalent’s continued progress in improving its operational performance and winning new business with new and existing customers raises our optimism.

Downsides

Forex Fluctuations: Catalent has significant operations outside the United States. Hence, changes in the exchange rates or any other applicable currency to the U.S. dollar will affect its operations. Volatility in currency exchange rates and other changes in exchange rates could result in unrealized and realized exchange losses despite any effort the company may undertake to manage or mitigate its exposure to fluctuations in the values of various currencies.

Stiff Competition: Catalent operates in a highly competitive market, wherein it competes with multiple companies, including those offering advanced delivery technologies and outsourced dose form or biologics manufacturing. The company also competes in some cases with the internal operations of pharmaceutical, biotechnology and consumer health customers with manufacturing capabilities and chooses to source these services internally.

Estimate Trend

Catalent has been witnessing a negative estimate revision trend for fiscal 2024. In the past 90 days, the Zacks Consensus Estimate for its earnings has moved 43.1% south to 82 cents.

The Zacks Consensus Estimate for the company’s first-quarter fiscal 2024 revenues is pegged at $933.2 million, suggesting an 8.7% decline from the year-ago quarter’s reported number.

Key Picks

Some better-ranked stocks in the broader medical space are DaVita Inc. DVA, McKesson Corporation MCK and Integer Holdings Corporation ITGR.

DaVita, sporting a Zacks Rank #1 (Strong Buy) at present, has an estimated long-term growth rate of 12.7%. DVA’s earnings surpassed estimates in three of the trailing four quarters and missed once, with an average surprise of 21.4%. You can see the complete list of today’s Zacks #1 Rank stocks here.

DaVita has gained 12.4% against the industry’s 4.7% decline over the past year.

McKesson, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth rate of 10.7%. MCK’s earnings surpassed estimates in three of the trailing four quarters and missed once, with an average of 8.1%.

McKesson has gained 26.9% compared with the industry’s 19.3% rise over the past year.

Integer Holdings, carrying a Zacks Rank #2 at present, has an estimated long-term growth rate of 12.1%. ITGR’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 8.4%.

Integer Holdings has gained 24.3% compared with the industry’s 1.3% rise over the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

DaVita Inc. (DVA) : Free Stock Analysis Report

McKesson Corporation (MCK) : Free Stock Analysis Report

Catalent, Inc. (CTLT) : Free Stock Analysis Report

Integer Holdings Corporation (ITGR) : Free Stock Analysis Report