3 Reasons to Hold Inogen (INGN) Stock in Your Portfolio

Inogen, Inc. INGN is well-poised for growth in the coming quarters, courtesy of its high prospects in the portable oxygen concentrator (POC) space. The optimism led by solid third-quarter 2023 and a strong product portfolio also looks promising. However, issues like stiff competition and forex volatility are major downsides.

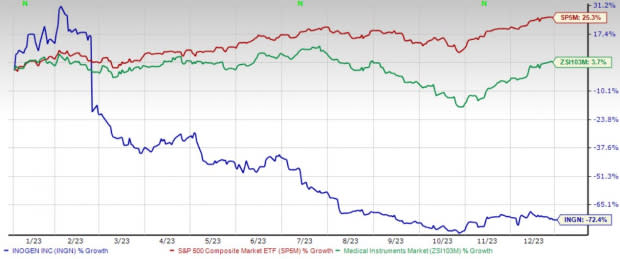

Over the past year, the Zacks Rank #3 (Hold) stock has lost 72.4% against the 3.7% rise of the industry and 25.3% growth of the S&P 500.

The renowned provider of POCs has a market capitalization of $127.9 million. The company projects 27.9% growth for 2024 and expects to witness continued improvements in its business. Inogen’s P/S ratio of 0.4 compares favorably with the industry’s 3.4.

Image Source: Zacks Investment Research

Let’s delve deeper.

High Prospects in the POC Space: We are optimistic about the POCs’ superiority over conventional oxygen therapy (known as the delivery model). Inogen primarily develops, manufactures and markets innovative POCs to deliver supplemental long-term oxygen therapy (LTOT) to patients suffering from chronic respiratory conditions. Inogen’s proprietary Inogen One and Inogen Rove systems concentrate the air around the patient to offer a source of supplemental oxygen anytime, anywhere, with a battery that can be plugged into an outlet.

Product Portfolio: We are optimistic about Inogen’s expanding product portfolio. The company completed the acquisition of Physio-Assist SAS in September 2023. Following the close of the transaction, it owns Physio-Assist and will now market the Simeox device outside of the United States.

On third-quarter 2023 earnings call in November 2023, Inogen’s management confirmed that it secured the reimbursement approval for Rove 6 in France in August. It is currently focused on introducing Rove 6 to key customers in that market.

Strong Q3 Results: Inogen’s robust year-over-year uptick in rental revenues and international business-to-business sales in third-quarter 2023 buoy optimism. The expansion of the adjusted gross margin also looked promising.

Downsides

Stiff Competition: The LTOT market is a highly competitive industry. Inogen competes with several manufacturers and distributors of POC and providers of other LTOT solutions, such as home delivery of oxygen tanks or cylinders. Given the relatively straightforward regulatory path in the oxygen therapy device manufacturing market, Inogen expects that the industry will become increasingly competitive in the future.

Forex Volatility: Inogen generates a significant portion of its revenues from the International market. Management expects international revenues to remain lumpy owing to the timing and size of the distributor. We also expect adverse foreign currency exchange rates to impede revenue growth in the near term owing to the strengthening of the U.S. dollar as against the Euro and other foreign currencies.

Estimate Trend

Inogen has been witnessing a negative estimate revision trend for 2024. Over the past 90 days, the Zacks Consensus Estimate for its loss per share has widened from $2.35 to $3.43.

The Zacks Consensus Estimate for fourth-quarter 2023 revenues is pegged at $78.1 million, suggesting an 11.4% decline from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space are DaVita Inc. DVA, Merit Medical Systems, Inc. MMSI and Integer Holdings Corporation ITGR.

DaVita, sporting a Zacks Rank #1 (Strong Buy), has an estimated long-term growth rate of 17.3%. DVA’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 36.6%. You can see the complete list of today’s Zacks #1 Rank stocks here.

DaVita’s shares have gained 39.9% compared with the industry’s 9.6% rise in the past year.

Merit Medical, carrying a Zacks Rank of 2 (Buy) at present, has an estimated long-term growth rate of 11.5%. MMSI’s earnings surpassed estimates in each of the trailing four quarters, with the average being 14.4%.

Merit Medical has gained 9.1% compared with the industry’s 12.9% rise in the past year.

Integer Holdings, carrying a Zacks Rank of 2 at present, has an estimated long-term growth rate of 15.8%. ITGR’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 11.9%.

Integer Holdings’ shares have rallied 44.7% compared with the industry’s 3.7% rise in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

DaVita Inc. (DVA) : Free Stock Analysis Report

Merit Medical Systems, Inc. (MMSI) : Free Stock Analysis Report

Inogen, Inc (INGN) : Free Stock Analysis Report

Integer Holdings Corporation (ITGR) : Free Stock Analysis Report