These 4 Measures Indicate That ARB (ASX:ARB) Is Using Debt Reasonably Well

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies ARB Corporation Limited (ASX:ARB) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for ARB

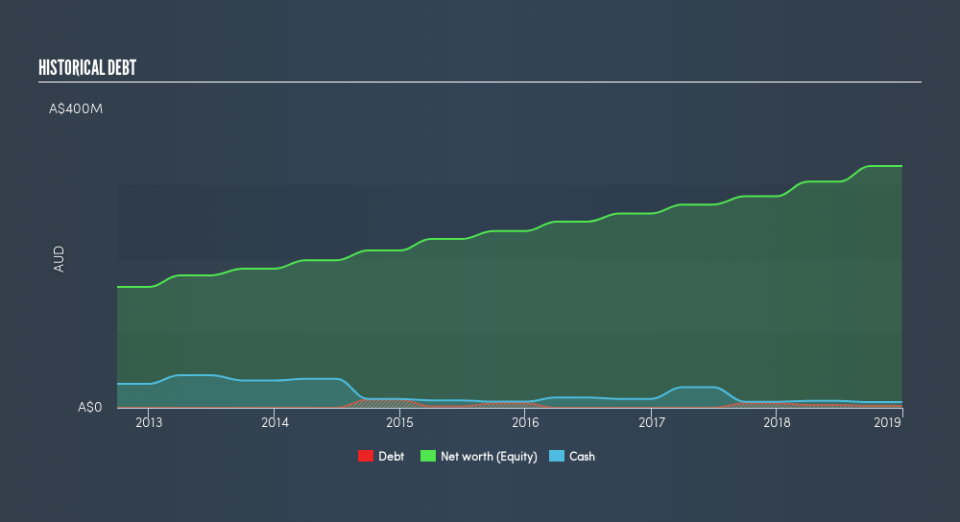

What Is ARB's Debt?

You can click the graphic below for the historical numbers, but it shows that ARB had AU$2.51m of debt in December 2018, down from AU$6.25m, one year before. However, its balance sheet shows it holds AU$7.72m in cash, so it actually has AU$5.21m net cash.

A Look At ARB's Liabilities

According to the last reported balance sheet, ARB had liabilities of AU$54.4m due within 12 months, and liabilities of AU$1.06m due beyond 12 months. Offsetting this, it had AU$7.72m in cash and AU$47.2m in receivables that were due within 12 months. So its total liabilities are just about perfectly matched by its shorter-term, liquid assets.

This state of affairs indicates that ARB's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the AU$1.36b company is struggling for cash, we still think it's worth monitoring its balance sheet. While it does have liabilities worth noting, ARB also has more cash than debt, so we're pretty confident it can manage its debt safely.

Fortunately, ARB grew its EBIT by 7.1% in the last year, making that debt load look even more manageable. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if ARB can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. ARB may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. In the last three years, ARB's free cash flow amounted to 36% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that ARB has AU$5.2m in net cash. On top of that, it increased its EBIT by 7.1% in the last twelve months. So we are not troubled with ARB's debt use. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that ARB insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.