5 Giant Wholesale Retailers to Buy for Q4 2023

Wall Street completed a disappointing third-quarter 2023 after witnessing an impressive bull run in the first two quarters. The fourth quarter of any year historically remains favorable to U.S. stock markets as it deals with the holiday season. Notably, during the holiday season the retail sector gets maximum importance. This year too, the scenario remains the same.

Retail sales have not been impacted much due to record-high inflationary pressures. U.S. consumption expenditure stayed buoyant despite the Fed pursuing an extremely high interest rate regime in the last one and a half years.

Research firm Deloitte estimated that the total holiday retail sales in 2023 will be in the range of $1.54 to $1.56 trillion during the November to January timeframe. This marks an year-over-year improvement of 3.5% to 4.6% in 2023. Deloitte also forecast that within the total holiday retail sales, e-commerce sales will account for $278 billion to $284 billion. This marks a year-over-year improvement of 10.3% to 12.8%.

Mastercard SpendingPulse estimated that holiday retail sales (excluding automotive) between Nov 1 and Dec 24, are expected to increase 3.7% year over year. E-commerce and online sales are likely to grow 6.7% and 2.9%, respectively.

Bain & Company forecasts nominal U.S. retail sales to grow 3% year over year in November and December, reaching nearly $915 billion, with 90% of the growth coming from non-store (e-commerce and mail-order) sales.

Our Top Picks

We have narrowed our search to five retail giants that have strong growth potential for the rest of 2023. These stocks have seen positive earnings estimate revisions in the last 60 days. Each of our picks carries either a Zacks Rank #1 (Strong Buy) or 2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

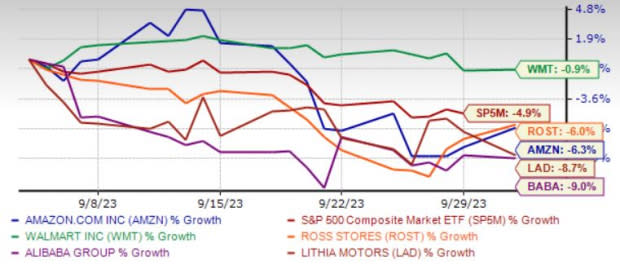

The chart below shows the price performance of our five picks in the past month.

Image Source: Zacks Investment Research

Amazon.com Inc. AMZN has been benefiting from a strengthening AWS services portfolio and its growing adoption rate has contributed well. Ultrafast delivery services and an expanding content portfolio are positives for AMZN. The strengthening relationship with third-party sellers is also encouraging. Its advertising business is also making a robust contribution. Improving Alexa skills along with robust smart home product offerings are tailwinds for AMZN.

Zacks Rank #1 Amazon has an expected revenue and earnings growth rate of 11.1% and more than 100%, respectively, for the current year. The Zacks Consensus Estimate for current-year earnings has improved 43.9% over the last 60 days.

Walmart Inc. WMT has been benefiting from its robust omnichannel operations due to its efforts to enhance store and online experience. WMT has been particularly gaining from its efforts to boost delivery services. Increased market share in grocery continued to boost U.S. comps in the first quarter of fiscal 2024. Strong comps growth globally, expense leverage and e-commerce growth across all units favored the company. WMT raised its guidance for fiscal 2024.

Zacks Rank #2 Walmart has an expected revenue and earnings growth rate of 9.3% and 2.2%, respectively, for the current year (ending January 2024). The Zacks Consensus Estimate for current-year earnings has improved 0.2% over the last 30 days.

Ross Stores Inc. ROST has benefited from positive customer response to its improved merchandise and strong value offerings. ROST has been benefiting from the execution of its store expansion plans over the years.

ROST operates a chain of off-price retail apparel and home accessories stores, which target value-conscious men and women, aged 25 to 54 in middle-to-upper middle-class households. ROST has a proven business model as the competitive bargains it offers continue to make its stores attractive destinations for customers in all economic scenarios.

Zacks Rank #1 Ross Stores has an expected revenue and earnings growth rate of 8.1% and 19.4%, respectively, for the current year (ending January 2024). The Zacks Consensus Estimate for current-year earnings has improved 6.1% over the last 60 days.

Lithia Motors Inc.’s LAD diversified product mix and multiple streams of income reduce its risk profile and position it for long-term sales and profit growth. LAD is on a buyout spree, which is increasing its market share.

Enhanced digital solutions — including the Driveway e-commerce program — are helping LAD to further boost profitability and market presence. Driveway generated $900 million in revenues in 2022 and expects to hit $9 billion in annual revenues by 2025, thus paving the path for LAD’s rapid growth.

Zacks Rank #1 Lithia Motors has an expected revenue and earnings growth rate of 7.6% and 1.4%, respectively, for next year. The Zacks Consensus Estimate for next-year earnings has improved 0.1% over the last seven days.

Alibaba Group Holding Ltd.’s BABA solid momentum across the China and international commerce retail businesses is driving its top-line growth. Notably, China commerce retail business is driven by rising online physical goods GMV at Taobao and Tmall. Further, International retail business is riding on solid combined order growth.

BABA’s strength across the Cainiao logistics services, owing to robust domestic consumer logistics and international fulfillment solution services is a plus. This apart, cloud computing business and local services are acting as tailwinds. Considering these factors, we expect total revenues of BABA to grow 8.2% in fiscal 2024 from fiscal 2023.

Zacks Rank #1 Alibaba Group Holding has an expected revenue and earnings growth rate of 4.7% and 14.9%, respectively, for the current year (ending March 2024). The Zacks Consensus Estimate for next-year earnings has improved 13.7% over the last 60 days.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Walmart Inc. (WMT) : Free Stock Analysis Report

Ross Stores, Inc. (ROST) : Free Stock Analysis Report

Lithia Motors, Inc. (LAD) : Free Stock Analysis Report

Alibaba Group Holding Limited (BABA) : Free Stock Analysis Report