5 Reasons to Add Old Second Bancorp (OSBC) to Your Portfolio

It seems to be a wise idea to add Old Second Bancorp, Inc. OSBC stock to your portfolio now. Supported by strong fundamentals, the company is well-poised for growth.

The Zacks Consensus Estimate for OSBC’s current-year earnings has been revised 1% upward over the past 60 days, reflecting that analysts are optimistic regarding its earnings growth potential. OSBC currently carries a Zacks Rank #2 (Buy).

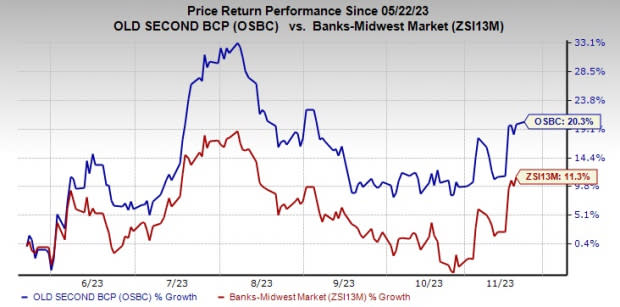

Over the past six months, shares of Old Second Bancorp have gained 20.3% compared with the industry’s growth of 11.3%.

Image Source: Zacks Investment Research

There are some other factors mentioned below that make Old Second Bancorp an attractive investment option now.

Earnings Strength: Over the last three to five years, the company witnessed earnings growth of 10.3%. The upward trend is expected to continue in the near term. In 2023, OSBC’s earnings are projected to grow 33.7%.

Moreover, the company has an impressive earnings surprise history. Its earnings surpassed the Zacks Consensus Estimate in three of the trailing four quarters, the average beat being 0.94%.

Revenue Growth: Old Second Bancorp’s revenues witnessed a compound annual growth rate (CAGR) of 18.8% over the last five years (2017-2022). The uptrend in revenues continued in the first nine months of 2023. In 2023, revenues are expected to increase 17.2% on a year-over-year basis.

Strong Leverage: Old Second Bancorp’s debt/equity ratio is 0.16, lower than the industry’s average debt/equity ratio of 0.31. This reflects that the company will be financially stable, even in adverse economic situations.

Superior Return on Equity (ROE): Old Second Bancorp’s ROE of 19.52% compares favorably with the industry average of 13.30%. This highlights the company’s commendable position over its peers in using shareholders’ funds.

Favorable Valuation: With respect to the price/earnings (P/E) ratio, the company seems undervalued right now. Its P/E (F1) ratio is 6.77, lower than the industry average of 8.44.

Moreover, the stock currently has a Value Score of B. The Value Score condenses all valuation metrics into one actionable score that helps investors steer clear of “value traps” and identify stocks that are truly trading at a discount. Our research shows that stocks with a Style Score of A or B, when combined with a Zacks Rank #1 (Strong Buy) or 2, offer the best upside potential.

Other Key Picks

A couple of other top-ranked stocks from the finance space are Prospect Capital Corporation PSEC and First Citizens BancShares, Inc. FCNCA.

Earnings estimates for PSEC have been revised 8.1% upward for the current fiscal year over the past 60 days. The company’s share price has decreased 5.2% over the past three months. PSEC currently sports a Zacks Rank #1. You can see the complete list of today’s Zacks #1 Rank stocks here.

First Citizens BancShares currently carries a Zacks Rank of 2. Its earnings estimates have been revised upward by 6.7% for the current year over the past 60 days. In the last three months, FCNCA’s share price increased 4.9%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

First Citizens BancShares, Inc. (FCNCA) : Free Stock Analysis Report

Old Second Bancorp, Inc. (OSBC) : Free Stock Analysis Report

Prospect Capital Corporation (PSEC) : Free Stock Analysis Report