5 Small Drug Stocks to Buy From a Rebounding Industry

The drug/biotech sector is seeing a recovery in 2024 after a rather lukewarm 2023. Biotech M&A activity is expected to be strong in 2024, which could be the prime reason for the optimistic outlook for the industry. In addition,innovation is likely to drive growth in the industry, with key spaces like weight loss/obesity and Alzheimer’s disease drugs attracting attention.

High interest rates, global supply chain constraints, pressure in the U.S. regional banking space and rising geopolitical concerns (Russia/Ukraine and Gaza/Israel wars) have increased broader economic concerns. Uncertainty about the impact of Medicare drug price negotiations and the Federal Trade Commission’s (FTC) scrutiny of M&A deals are some other concerns. Nonetheless, the fundamentals of the sector remain strong, and investors are expected to come back to this defensive space eventually. These positive factors should keep stocks like United Therapeutics UTHR, Esperion Therapeutics. ESPR, Heron Therapeutics HRTX, Lyra Therapeutics LYRA and Aldeyra Therapeutics ALDX afloat.

Industry Description

The Zacks Medical-Drugs industry comprises small and some medium-sized drug companies, which make medicines for both human and veterinary use. We have a separate industry outlook discussion on big drugmakers. Small drugmakers have a limited portfolio of marketed drugs or no commercial-stage drugs at all. Some drugmakers are dependent on just one marketed drug or pipeline candidate. For such companies, upfront or milestone payments from collaboration partners — in most cases their larger counterparts — are the main sources of revenues. These companies need ample free cash flow to fund their R&D activities.

Factors Shaping the Future of the Medical-Drugs Industry

Pipeline Success: The success or failure of key pipeline candidates in clinical studies can significantly drive the stock price of industry players. Successful innovation and product line extensions in important therapeutic areas and strong clinical study results may act as important catalysts for the stocks.

Strong Collaboration Partners: These companies regularly seek external partners and collaborators for complementary strengths. A partnership deal with a popular drugmaker is a good sign about the potential of small pharma companies, especially when an equity investment is included in the deal. M&A deals are in full swing in the sector, signaling growth.

Investment in Technology for Innovation: For these smaller companies, succeeding in a shifting global market and evolving healthcare landscape requires adopting innovative business models, investing in new technologies and increasing investments in personalized medicines. Over the past few years, scientific and technological advancements have made it possible to develop personalized therapies. Other than that, adoption and information exchange through the meaningful use of health IT, development of therapies that improve overall patient outcomes and investment in developing and emerging markets are some of the key priorities for drug companies. Artificial intelligence and machine learning techniques are being used for the rapid advancement of drug discovery and target identification processes.

Pipeline Setbacks: The smaller companies have their share of risk in the form of unstable cash flows. Also, the failure of key pipeline candidates in pivotal studies and regulatory and pipeline delays can be huge setbacks for these smaller companies and significantly hurt their share price in the future.

Zacks Industry Rank Indicates Bright Prospects

The group’s Zacks Industry Rank is basically the average of the Zacks Rank of all the member stocks.

The Zacks Medical-Drugs industry currently carries a Zacks Industry Rank #97, which places it in the top 39% of 250 Zacks industries. Our research shows that the top 50% of the Zacks-ranked industries outperform the bottom 50% by a factor of more than 2 to 1.

Before we present you with a few top-ranked stocks to capitalize on the thriving prospects of the small and medium-sized drugmakers’ space, let’s take a look at the industry’s recent stock-market performance and the valuation picture.

Industry Lags S&P 500 and Sector

The Zacks Medical-Drugs industry is a huge 190-stock group within the broader Medical sector. The industry has underperformed the S&P 500 as well as the Zacks Medical sector in the past year.

Stocks in this industry have collectively risen 0.5% in the past year compared with the Zacks S&P 500 composite’s rise of 28.3% and the Zacks Medical sector’s increase of 9.4% in the said time frame.

One Year Price Performance

Industry's Current Valuation

On the basis of the trailing 12 months price-to-sales ratio (P/S TTM), which is a commonly used multiple for valuing these small drugmakers, the industry is currently trading at 2.18, compared with the S&P 500’s 4.22 and the Zacks Medical sector's 3.37.

Over the last five years, the industry has traded as high as 5.06X, as low as 1.70X, and at the median of 2.66X, as the chart below shows.

Trailing 12-Month Price-to-Sales (P/S) Ratio

5 Drug Stocks to Keep an Eye On

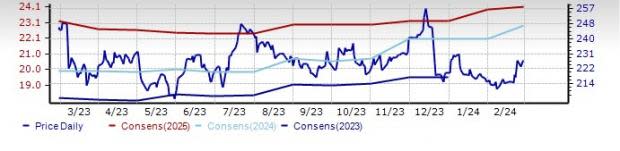

United Therapeutics: Silver Spring, MD-based United Therapeutics Corporation markets three medicines to treat pulmonary arterial hypertension (PAH) called Remodulin, Orenitram and Tyvaso, which are different formulations of treprostinil. Demand for United Therapeutics’ treprostinil medicines is strong with a record number of patients on therapy despite generic concerns and competitive pressure. Potential approvals for the expanded use of Orenitram and Tyvaso can potentially drive long-term growth. The company aims to develop Tyvaso in idiopathic pulmonary fibrosis and progressive pulmonary fibrosis indications, which are forms of chronic fibrosing interstitial lung disease, as management believes that sales in PAH indications have reached their peak. The company is progressing fast toward its goal of generating revenues worth $4 billion by 2025-end.

United Therapeutics’ stock has declined 7.2% in the past year. The consensus estimate for 2024 earnings has risen from $23.17 per share to $24.14 per share over the past 60 days. The company has a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here. .

Price and Consensus: UTHR

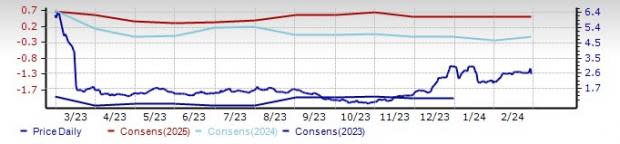

Esperion Therapeutics: Plymouth, MI-based Esperion Therapeutics’ portfolio of marketed drugs, Nexletol and Nexlizet, have demonstrated encouraging uptake since their launch in 2020. The drugs’ prescription trends have improved sequentially in recent quarters. Esperion’s restructuring plan to focus on commercializing its two drugs and reducing operating expenses seems promising. Positive data from the CLEAR outcome study on Nexletol in cardiovascular (CV) risk reduction, if approved to be included in the drug’s label, should allow the drug to be prescribed to a larger treatment population. Management has submitted this data to regulatory bodies in the United States and Europe, with a potential approval expected in 2024.

Esperion Therapeutics’ stock has declined 57% in the past year. The consensus estimate for 2024 earnings has risen from 53 cents per share to 73 cents per share over the past 60 days. The company has a Zacks Rank #2.

Price and Consensus: ESPR

Lyra Therapeutics: Watertown, MA-based Lyra Therapeutics is developing two therapies for the treatment of chronic rhinosinusitis (CRS) in late-stage studies. LYR-210 and LYR-220 are bioresorbable nasal implants designed to deliver six months of continuous anti-inflammatory medication to the sinonasal passages for the treatment of CRS, a highly prevalent inflammatory disease of the paranasal sinuses.

In September, Lyra announced positive top-line data from the BEACON phase II study of LYR-220 in CRS patients who have had prior ethmoid sinus surgery. The study met its primary safety endpoint with LYR-220 demonstrating statistically significant and clinically relevant improvements in symptom severity.

Enrollment has been completed in the pivotal phase III ENLIGHTEN I study on the second candidate, LYR-210, in CRS patients who have not had ethmoid sinus surgery, with top-line data expected in the first half of 2024. Enrollment is ongoing in the second pivotal phase III study, ENLIGHTEN II on LYR-210, also in the pre-surgical CRS patient group.

The stock of Lyra Therapeutics has risen 142.5% in the past year. The consensus estimate for 2024 loss has narrowed from $1.09 per share to $1.07 per share over the past 60 days. The company has a Zacks Rank #2.

Price and Consensus: LYRA

Heron Therapeutics: Redwood City, CA-based Heron Therapeutics’ key marketed drug is Zynrelef, a non-opioid dual-acting local anesthetic for post-operative pain for a wide range of surgical procedures. In January, the FDA approved an expansion to the Zynrelef label to include additional orthopedic and soft tissue procedures, which will now cover an estimated 13 million procedures annually, an estimated increase of 86% over the prior indicated procedures. In phase III studies, Zynrelef demonstrated superiority to bupivacaine solution, the current standard of care, with lower pain scores, fewer patients experiencing severe pain and lower opioid consumption. In January, the company also announced a five-year distributor partnership with CrossLink Life Sciences to expand promotional efforts for Zynrelef. Its other commercial products Aponvie, Cinvanti and Sustol are also generating decent sales.

The stock of Heron Therapeutics has risen 16.3% in the past year. The consensus estimate for 2024 loss has widened from 40 cents per share to 48 cents per share over the past 60 days. The company has a Zacks Rank #2.

Price and Consensus: HRTX

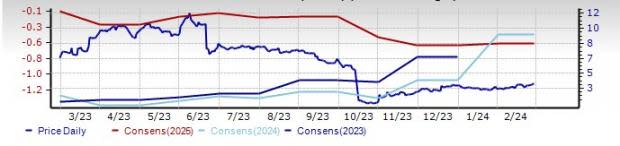

Aldeyra Therapeutics: Burlington, MA-based Aldeyra Therapeutics is a leader in the development of RASP (reactive aldehyde species) modulators for the treatment of immune-mediated disease. Lately, it has seen success with studies on its investigational RASP modulator, ADX-629, which has demonstrated potential activity in clinical studies of patients with psoriasis, asthma, COVID, ethanol toxicity, chronic cough and atopic dermatitis.

Aldeyra Therapeutics is conducting a phase II study on ADX-629 in Sjögren-Larsson Syndrome and moderate alcoholic hepatitis. Based on positive biomarker results observed in the adult cohort of the phase II study of ADX-629 in Sjögren-Larsson Syndrome, Aldeyra Therapeutics plans to expand the study to include pediatric patients for which a proposed expansion is expected to be filed with the FDA in the first half of 2024. At present, there is no FDA-approved therapy for Sjögren-Larsson Syndrome. Initial clinical data from Sjögren-Larsson Syndrome study on ADX-629 demonstrated broad-based normalization of the majority of abnormal metabolomic signatures along with a reduction in accumulation of fatty alcohols in patients treated with ADX-629.

Top-line results from the moderate alcoholic hepatitis study are expected in the second half of 2024. Two other investigational RASP modulators, ADX-246 and ADX-248, are in early-stage development.

The stock of Aldeyra Therapeutics has declined 47.8% in the past year. The consensus estimate for 2024 loss has narrowed from $1.08 per share to 45 cents per share over the past 60 days. The company has a Zacks Rank #2.

Price and Consensus: ALDX

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

United Therapeutics Corporation (UTHR) : Free Stock Analysis Report

Esperion Therapeutics, Inc. (ESPR) : Free Stock Analysis Report

Aldeyra Therapeutics, Inc. (ALDX) : Free Stock Analysis Report

Heron Therapeutics, Inc. (HRTX) : Free Stock Analysis Report

Lyra Therapeutics, Inc. (LYRA) : Free Stock Analysis Report