Accelerate Diagnostics, Inc.'s (NASDAQ:AXDX) 38% Jump Shows Its Popularity With Investors

Accelerate Diagnostics, Inc. (NASDAQ:AXDX) shareholders are no doubt pleased to see that the share price has bounced 38% in the last month, although it is still struggling to make up recently lost ground. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 33% over that time.

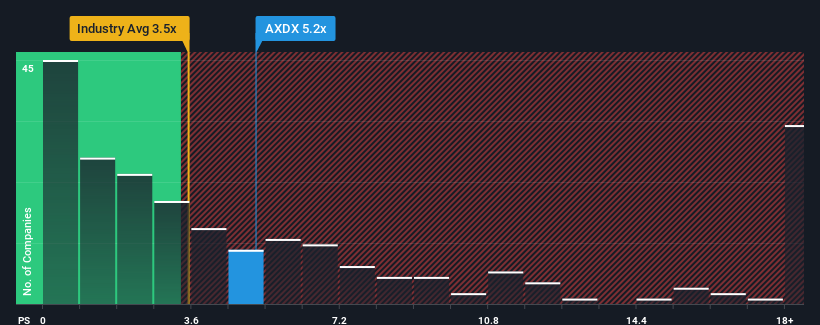

After such a large jump in price, Accelerate Diagnostics may be sending bearish signals at the moment with its price-to-sales (or "P/S") ratio of 5.2x, since almost half of all companies in the Medical Equipment in the United States have P/S ratios under 3.5x and even P/S lower than 1.5x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

View our latest analysis for Accelerate Diagnostics

What Does Accelerate Diagnostics' Recent Performance Look Like?

Accelerate Diagnostics' revenue growth of late has been pretty similar to most other companies. One possibility is that the P/S ratio is high because investors think this modest revenue performance will accelerate. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Accelerate Diagnostics.

What Are Revenue Growth Metrics Telling Us About The High P/S?

The only time you'd be truly comfortable seeing a P/S as high as Accelerate Diagnostics' is when the company's growth is on track to outshine the industry.

Retrospectively, the last year delivered a decent 8.2% gain to the company's revenues. This was backed up an excellent period prior to see revenue up by 37% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Looking ahead now, revenue is anticipated to climb by 24% per annum during the coming three years according to the two analysts following the company. With the industry only predicted to deliver 8.9% per annum, the company is positioned for a stronger revenue result.

With this in mind, it's not hard to understand why Accelerate Diagnostics' P/S is high relative to its industry peers. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Key Takeaway

Accelerate Diagnostics' P/S is on the rise since its shares have risen strongly. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Accelerate Diagnostics maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Medical Equipment industry, as expected. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 6 warning signs with Accelerate Diagnostics (at least 2 which can't be ignored), and understanding these should be part of your investment process.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here