Should You Be Adding BCB Bancorp (NASDAQ:BCBP) To Your Watchlist Today?

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like BCB Bancorp (NASDAQ:BCBP). While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

See our latest analysis for BCB Bancorp

How Fast Is BCB Bancorp Growing?

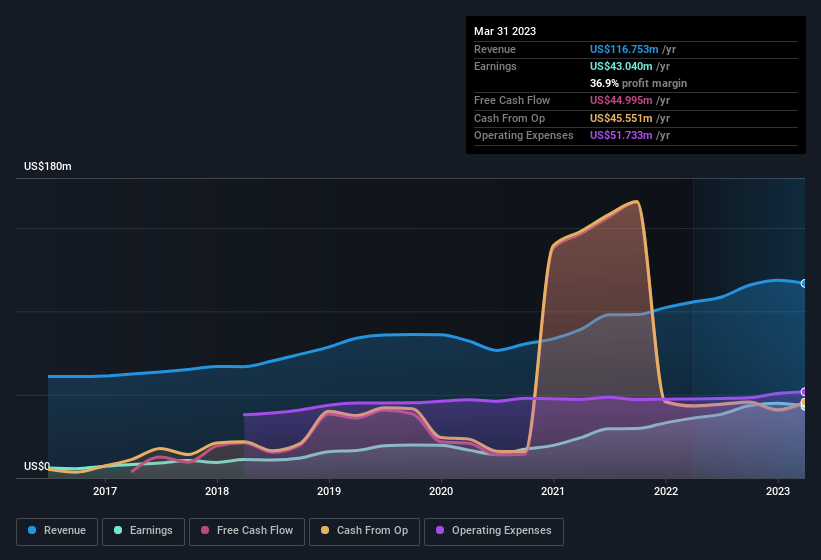

If a company can keep growing earnings per share (EPS) long enough, its share price should eventually follow. That means EPS growth is considered a real positive by most successful long-term investors. Shareholders will be happy to know that BCB Bancorp's EPS has grown 37% each year, compound, over three years. If the company can sustain that sort of growth, we'd expect shareholders to come away satisfied.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. It's noted that BCB Bancorp's revenue from operations was lower than its revenue in the last twelve months, so that could distort our analysis of its margins. While we note BCB Bancorp achieved similar EBIT margins to last year, revenue grew by a solid 11% to US$117m. That's a real positive.

You can take a look at the company's revenue and earnings growth trend, in the chart below. Click on the chart to see the exact numbers.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of BCB Bancorp's forecast profits?

Are BCB Bancorp Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

The good news is that BCB Bancorp insiders spent a whopping US$1.2m on stock in just one year, without so much as a single sale. Knowing this, BCB Bancorp will have have all eyes on them in anticipation for the what could happen in the near future. We also note that it was the Independent Chairman of the Board, Mark Hogan, who made the biggest single acquisition, paying US$169k for shares at about US$11.24 each.

Along with the insider buying, another encouraging sign for BCB Bancorp is that insiders, as a group, have a considerable shareholding. To be specific, they have US$23m worth of shares. That's a lot of money, and no small incentive to work hard. As a percentage, this totals to 12% of the shares on issue for the business, an appreciable amount considering the market cap.

Does BCB Bancorp Deserve A Spot On Your Watchlist?

You can't deny that BCB Bancorp has grown its earnings per share at a very impressive rate. That's attractive. Not only that, but we can see that insiders both own a lot of, and are buying more shares in the company. These things considered, this is one stock worth watching. One of Buffett's considerations when discussing businesses is if they are capital light or capital intensive. Generally, a company with a high return on equity is capital light, and can thus fund growth more easily. So you might want to check this graph comparing BCB Bancorp's ROE with industry peers (and the market at large).

Keen growth investors love to see insider buying. Thankfully, BCB Bancorp isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here