Advance Auto Parts (NYSE:AAP) Beats Q3 Sales Targets But Stock Drops 11.1%

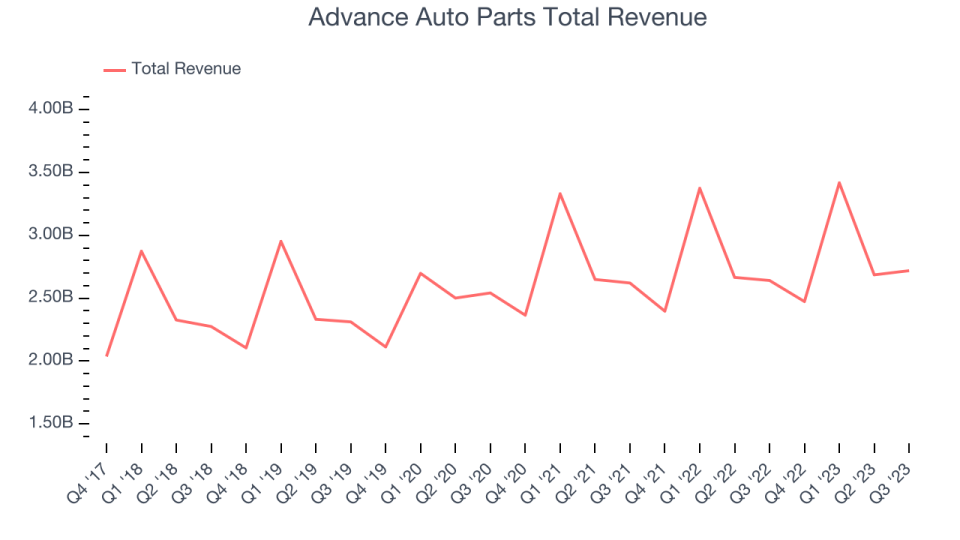

Auto parts and accessories retailer Advance Auto Parts (NYSE:AAP) beat analysts' expectations in Q3 FY2023, with revenue up 2.9% year on year to $2.72 billion. Its full-year revenue guidance of $11.28 billion at the midpoint also came in slightly above analysts' estimates. Turning to EPS, Advance Auto Parts made a GAAP loss of $0.82 per share, down from its profit of $1.84 per share in the same quarter last year.

Is now the time to buy Advance Auto Parts? Find out by accessing our full research report, it's free.

Advance Auto Parts (AAP) Q3 FY2023 Highlights:

Revenue: $2.72 billion vs analyst estimates of $2.67 billion (1.7% beat)

EPS: -$0.82 vs analyst estimates of $1.44 (-$2.26 miss)

The company reconfirmed its revenue guidance for the full year of $11.28 billion at the midpoint

The company significantly lowered its GAAP EPS guidance for the full year to $1.60 at the midpoint ($4.80 prior, reduction includes some one-time expenses)

Free Cash Flow of $152.6 million, up 193% from the same quarter last year

Gross Margin (GAAP): 36.3%, down from 44.7% in the same quarter last year (one-time "change in estimate for inventory reserves that resulted in a one-time impact of approximately $119 million")

Same-Store Sales were up 1.2% year on year (beat vs. expectations of up 0.3% year on year)

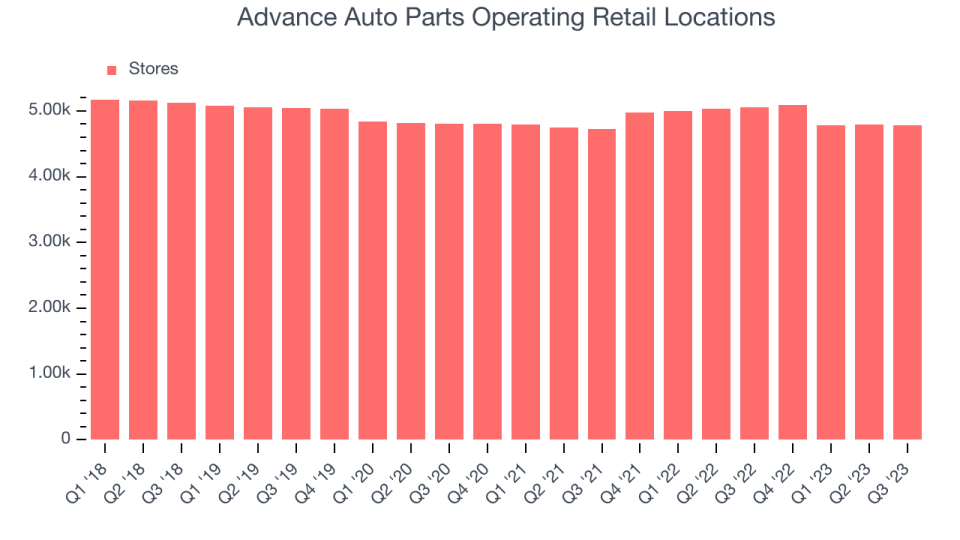

Store Locations: 4,785 at quarter end, decreasing by 275 over the last 12 months

“Since joining Advance, I have partnered with the board and management team to move with speed in conducting a comprehensive review of the business,” said Shane O'Kelly, president and chief executive officer.

Founded in Virginia in 1932, Advance Auto Parts (NYSE:AAP) is an auto parts and accessories retailer that sells everything from carburetors to motor oil to car floor mats.

Auto Parts Retailer

Cars are complex machines that need maintenance and occasional repairs, and auto parts retailers cater to the professional mechanic as well as the do-it-yourself (DIY) fixer. Work on cars may entail replacing fluids, parts, or accessories, and these stores have the parts and accessories or these jobs. While e-commerce competition presents a risk, these stores have a leg up due to the combination of broad and deep selection as well as expertise provided by sales associates. Another change on the horizon could be the increasing penetration of electric vehicles.

Sales Growth

Advance Auto Parts is larger than most consumer retail companies and benefits from economies of scale, giving it an edge over its competitors.

As you can see below, the company's annualized revenue growth rate of 3.9% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was mediocre as its store footprint remained relatively unchanged, implying that growth was driven by more sales at existing, established stores.

This quarter, Advance Auto Parts reported decent year-on-year revenue growth of 2.9%, and its $2.72 billion in revenue topped Wall Street's estimates by 1.7%. Looking ahead, analysts expect sales to grow 1.2% over the next 12 months.

While most things went back to how they were before the pandemic, a few consumer habits fundamentally changed. One founder-led company is benefiting massively from this shift and is set to beat the market for years to come. The business has grown astonishingly fast, with 40%+ free cash flow margins, and its fundamentals are undoubtedly best-in-class. Still, its total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Number of Stores

A retailer's store count often determines on how much revenue it can generate.

When a retailer like Advance Auto Parts keeps its store footprint steady, it usually means that demand is stable and it's focused on improving operational efficiency to increase profitability. Advance Auto Parts's store count shrank by 275 locations, or 5.4%, over the last 12 months to 4,785 total retail locations in the most recently reported quarter.

Taking a step back, the company has kept its physical footprint more or less flat over the last two years while other consumer retail businesses have opted for growth. A flat store base means that revenue growth must come from increased e-commerce sales or higher foot traffic and sales per customer at existing stores.

Same-Store Sales

Advance Auto Parts's demand within its existing stores has been relatively stable over the last eight quarters but fallen behind the broader consumer retail sector. On average, the company's same-store sales have grown by 1.3% year on year. Given its flat store count over the same period, this performance stems from increased foot traffic at existing stores or higher e-commerce sales as the company shifts demand from in-store to online.

In the latest quarter, Advance Auto Parts's same-store sales rose 1.2% year on year. This growth was a well-appreciated turnaround from the 0.7% year-on-year decline it posted 12 months ago, showing the business is regaining momentum.

Key Takeaways from Advance Auto Parts's Q3 Results

With a market capitalization of $3.45 billion, Advance Auto Parts is among smaller companies, but its $317.5 million cash balance and positive free cash flow over the last 12 months give us confidence that it has the resources needed to pursue a high-growth business strategy.

It was good to see Advance Auto Parts beat analysts' revenue expectations this quarter, aided by a same-store sales beat. Beyond that, it was a complicated and worrisome quarter. Gross margin declined meaningfully year on year (partly due to a one-time inventory charge) and EPS missed. While full year revenue guidance was only slightly lowered, EPS guidance was meaningfully lowered, with management highlighting "continued pressure in Q4 from higher product costs that we do not expect to offset with price. We are taking significant steps to improve our cost structure and remain focused on returning the business to profitable growth.” Overall, this was a mediocre quarter for Advance Auto Parts. The company is down 11.1% on the results and currently trades at $51.97 per share.

Advance Auto Parts may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

The author has no position in any of the stocks mentioned in this report.