Is The AES (AES) Too Good to Be True? A Comprehensive Analysis of a Potential Value Trap

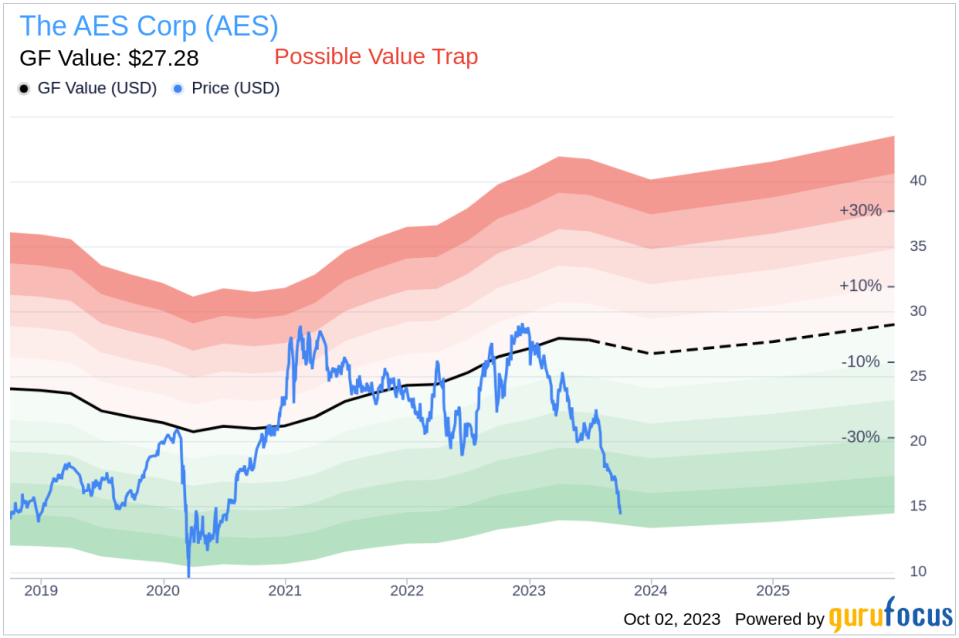

Value-focused investors are constantly seeking stocks that are priced below their intrinsic value. The AES Corp (NYSE:AES) is one such stock that warrants attention. Currently priced at $14.51, the stock recorded a daily loss of 4.57% and a 3-month decrease of 29%. According to its GF Value, the stock's fair valuation stands at $27.28.

Understanding GF Value

The GF Value represents the current intrinsic value of a stock, derived from our unique methodology. The GF Value Line on our summary page provides an overview of the fair value at which the stock should ideally be traded. This value is calculated based on historical multiples (PE Ratio, PS Ratio, PB Ratio, and Price-to-Free-Cash-Flow) that the stock has traded at, GuruFocus adjustment factor based on the company's past returns and growth, and future estimates of business performance.

The GF Value Line represents the fair value at which the stock should be traded. If the stock price significantly deviates from the GF Value Line, it indicates potential overvaluation or undervaluation, affecting its future return.

However, before making an investment decision, investors need to delve deeper. Despite its seemingly attractive valuation, The AES (NYSE:AES) carries certain risk factors that should not be overlooked. Reflected primarily through its low Altman Z-score of 0.51, these indicators suggest that The AES, despite its apparent undervaluation, might be a potential value trap. This complexity underscores the importance of thorough due diligence in investment decision-making.

Understanding Altman Z-score

The Altman Z-score is a financial model invented by New York University Professor Edward I. Altman in 1968. It predicts the probability of a company entering bankruptcy within a two-year time frame. The Altman Z-Score combines five different financial ratios, each weighted to create a final score. A score below 1.8 suggests a high likelihood of financial distress, while a score above 3 indicates a low risk.

Company Overview: The AES Corp (NYSE:AES)

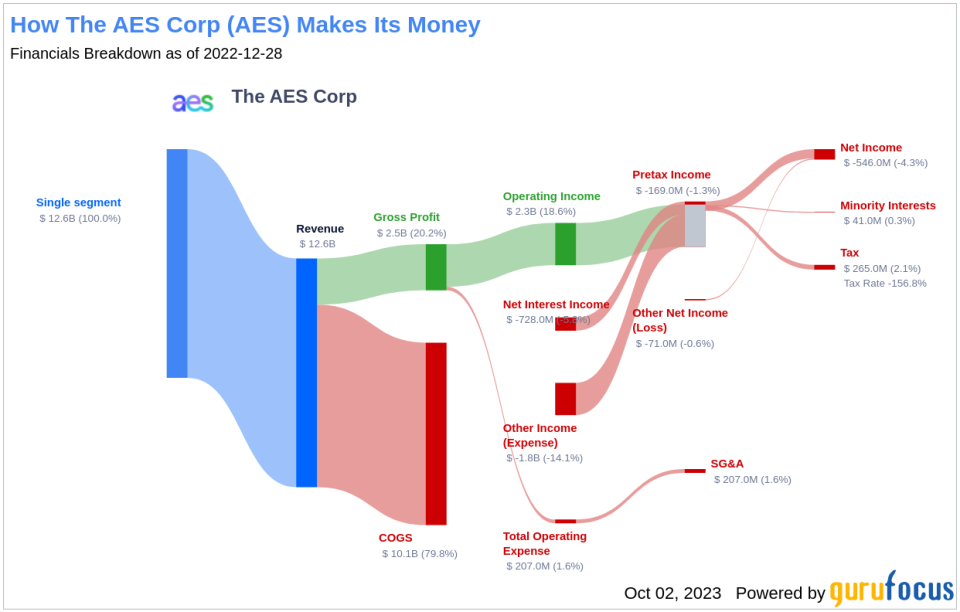

AES is a global power company with a generation portfolio consisting of over 32 gigawatts of generation, including renewable energy (46%), gas (32%), coal (20%), and oil (2%). The AES operates six electric utilities, distributing power to 2.6 million customers. Despite its market cap of $9.70 billion and sales of $13 billion, the stock's price is lower than its GF Value, suggesting potential undervaluation.

The AES's Low Altman Z-Score: A Breakdown of Key Drivers

A closer look at The AES's Altman Z-score reveals potential financial distress. The EBIT to Total Assets ratio, which correlates earnings before interest and taxes (EBIT) to total assets, is a crucial measure of a company's operational effectiveness. An analysis of The AES's EBIT to Total Assets ratio from historical data (2021: 0.03; 2022: 0.01; 2023: 0.03) indicates a declining trend. This reduction suggests that The AES might not be utilizing its assets to their full potential to generate operational profits, which could negatively affect the company's overall Z-score.

Conclusion: Is The AES a Value Trap?

Despite its seemingly undervalued price, The AES (NYSE:AES) carries potential risk factors that should not be overlooked. The low Altman Z-score and declining EBIT to Total Assets ratio suggest potential financial distress, indicating that The AES might be a value trap. Thorough due diligence is crucial before making an investment decision. GuruFocus Premium members can find stocks with high Altman Z-Score using the following Screener: Walter Schloss Screen .

This article first appeared on GuruFocus.