The AES Corporation (AES): Time For A Financial Health Check

Stocks with market capitalization between $2B and $10B, such as The AES Corporation (NYSE:AES) with a size of USD $7.01B, do not attract as much attention from the investing community as do the small-caps and large-caps. However, generally ignored mid-caps have historically delivered better risk adjusted returns than both of those groups, primarily due to seasoned executives running a lean corporate structure. I recommend you look at the following hurdles to assess AES’s financial health. See our latest analysis for AES

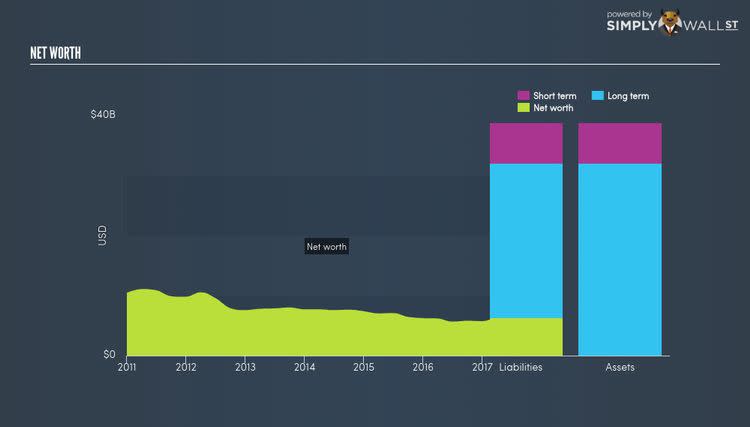

Can AES service its debt comfortably?

While ideally the debt-to equity ratio of a financially healthy company should be less than 40%, several factors such as industry life-cycle and economic conditions can result in a company raising a significant amount of debt. In the case of AES, the debt-to-equity ratio is over 100%, which means that it is a highly leveraged company. This is not a problem if the company has consistently grown its profits. But during a business downturn, availability of cash may dry up, making it hard to operate. While debt-to-equity ratio has several factors at play, an easier way to check whether AES’s leverage is at a sustainable level is to check its ability to service the debt. A company generating earnings at least three times its interest payments is considered financially sound. AES’s interest on debt is not strongly covered by earnings as it sits at around 2.45x. This means lenders may refuse to lend the company more money, as it is seen as too risky in terms of default.

Can AES pay its short-term liabilities?

Debt to equity ratio is an important aspect of financial strength. But if the company has a substantial amount of cash on its balance sheet, that should allay some fear of a debt overhang and increase the chance of meeting upcoming liabilities. In order to measure liquidity, we must compare AES’s current assets with its upcoming liabilities. Our analysis shows that AES does not have enough liquid assets on hand to meet its upcoming liabilities. Though this is a common practice, since cash is better utilized invested in the business or returned to shareholders, it does raise some concerns for investors should adverse events arise.

Next Steps:

Are you a shareholder? AES’s high debt levels are not met with high cash flow coverage. This means investors should ask themselves if they think AES can improve in terms of debt management and operational efficiency. Given that AES’s financial situation may change, I recommend exploring market expectations for AES’s future growth on our free analysis platform.

Are you a potential investor? Although investors should analyse the serviceability of debt, it shouldn’t be viewed in isolation of other factors. Ultimately, debt is often used to fund or accelerate new projects that are expected to improve a company’s growth trajectory in the longer term. AES’s Return on Capital Employed (ROCE) in order to see management’s track record at deploying funds in high-returning projects.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.