Altice (ATUS) Q4 Earnings Miss Estimates on Lower Revenues

Altice USA, Inc. ATUS reported mixed fourth-quarter 2023 results, with the top line surpassing the Zacks Consensus Estimate but the bottom line missing the same. The company reported a revenue decline year over year, owing to soft demand trends in the Residential, News and Advertising segments. However, growth in mobile line net additions, the company’s focus on network upgrades, improving customer care, AI integration and financial discipline are positive factors.

Net Income

Altice reported a net loss of $117.8 million or a loss of 26 cents per share compared with a loss of $193.1 million or 43 cents per share in the prior-year quarter. Income tax benefit and lower operating expenses led to a narrower loss during the quarter. The bottom line, however, missed the Zacks Consensus Estimate by 33 cents.

In 2023, net income was $53.2 million, down from $194.6 million in 2022.

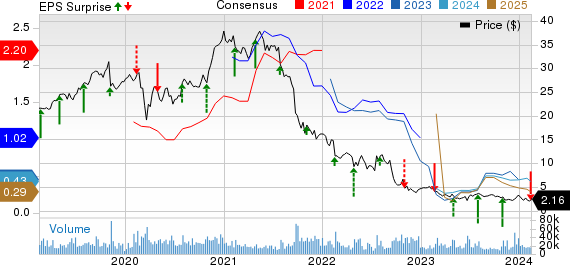

Altice USA, Inc. Price, Consensus and EPS Surprise

Altice USA, Inc. price-consensus-eps-surprise-chart | Altice USA, Inc. Quote

Revenues

Total revenues in the quarter were $2.3 billion, down from $2.36 billion in the prior-year quarter. Declining net sales from broadband and video customers impeded the top line. However, the top line beat the consensus estimate by 13 million.

In 2023, net sales totaled $9.23 billion compared with $9.64 billion in 2022.

The company made progress in its growth strategies by accelerating network enhancement and customer experience. At the quarter-end, Altice had 2.73 million FTTH (Fiber to the home) passings, about 14,900 of which were added in the September-December period.

FTTH broadband net additions were more than 46,000 in the quarter, led by increased migration of existing customers and higher fiber gross additions. Total fiber broadband customers reached 341,000 by the end of the quarter. Residential average revenue per user (ARPU) improves marginally by 0.1% year over year to $136.01. Despite losses of video subscribers, greater mobile penetration, lower churn rate and AI implementation across care and retention centers supported the ARPU.

Business services and wholesale revenues increased to $372 million from $368.4 million in the year-ago quarter. The improvement was driven by growth in Lightpath revenues. Net sales surpassed our revenue estimate of $349.3 million.

News and Advertising revenues were $128.1 million, down from 151.8 million in the year-earlier quarter, owing to lower political advertising revenues. Net sales fell short of our revenue estimate of $157.9 million.

Residential revenues (which include Broadband, Video and Telephony) were $1.79 billion, down from $1.83 billion in the year-earlier quarter, primarily due to the loss of higher ARPU video customers. Net sales beat our estimate of $1.75 billion.

Other Quarterly Details

Operating income improved to $302.3 million from $301.1 million in the year-ago quarter. Adjusted EBITDA was $903.3 million compared with $913.3 million in the prior-year quarter. Optimum Mobile witnessed healthy subscriber growth during the quarter, reaching 322,000 customers, representing a 7.1% penetration of the company’s total broadband customer base.

Altice’s total passings grew more than 165,000 and reached 9.6 million at the end of the full year 2023. The company is witnessing solid customer penetration, typically reaching approximately 40% within a year of rollout in new-build areas.

Cash Flow & Liquidity

In 2023, Altice generated $1.82 billion of cash from operating activities compared with $2.36 billion in 2022. As of Dec 31, 2023, the company’s net debt was $24.82 billion.

Zacks Rank & Stocks to Consider

Altice currently has a Zacks Rank #3 (Hold).

NVIDIA Corporation NVDA, currently carrying a Zacks Rank #2 (Buy), delivered a trailing four-quarter average earnings surprise of 18.99%. In the last reported quarter, it delivered an earnings surprise of 19.64%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

NVIDIA is the worldwide leader in visual computing technologies and the inventor of the graphic processing unit. Over the years, the company’s focus evolved from PC graphics to AI-based solutions that support high-performance computing, gaming and virtual reality platforms.

Qualcomm Inc. QCOM, carrying a Zacks Rank #2 at present, delivered a trailing four-quarter average earnings surprise of 5.9%. In the last reported quarter, it delivered an earnings surprise of 15.55%.

It designs, manufactures and markets digital wireless telecom products and services based on the Code Division Multiple Access technology. The products include CDMA-based integrated circuits and system software for wireless voice and data communications as well as global positioning system products.

Arista Networks, Inc. ANET, carrying a Zacks Rank #2 at present, is likely to benefit from strong momentum and diversification across its top verticals and product lines. The company has a software-driven, data-centric approach to help customers build their cloud architecture and enhance their cloud experience. Arista has delivered an earnings surprise of 13.28%, on average, in the trailing four quarters.

The company holds a leadership position in 100-gigabit Ethernet switching share in port for the high-speed data center segment. It is increasingly gaining market traction in 200 and 400-gig high-performance switching products and remains well-positioned for healthy growth in the data-driven cloud networking business with proactive platforms and predictive operations.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

QUALCOMM Incorporated (QCOM) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

Arista Networks, Inc. (ANET) : Free Stock Analysis Report

Altice USA, Inc. (ATUS) : Free Stock Analysis Report