Analyst Forecasts Just Became More Bearish On Daqo New Energy Corp. (NYSE:DQ)

Market forces rained on the parade of Daqo New Energy Corp. (NYSE:DQ) shareholders today, when the analysts downgraded their forecasts for this year. Revenue estimates were cut sharply as the analysts signalled a weaker outlook - perhaps a sign that investors should temper their expectations as well.

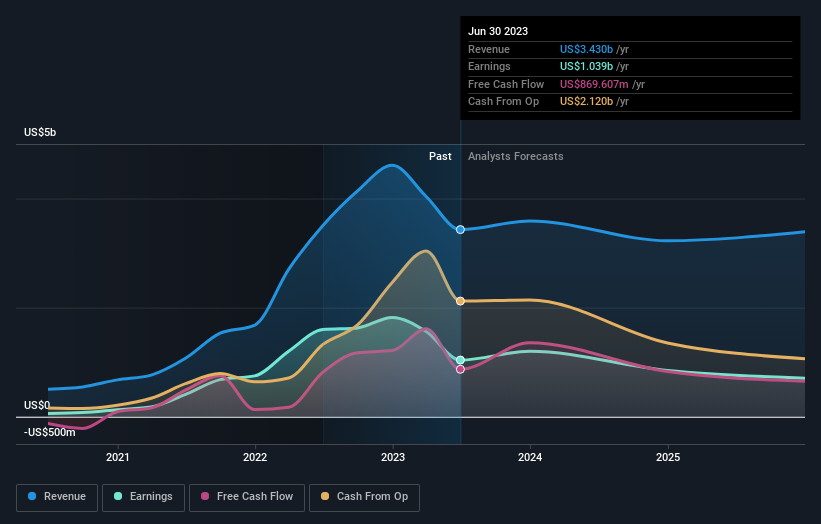

Following the latest downgrade, the current consensus, from the twelve analysts covering Daqo New Energy, is for revenues of US$2.9b in 2023, which would reflect an uncomfortable 16% reduction in Daqo New Energy's sales over the past 12 months. Statutory earnings per share are presumed to grow 14% to US$15.30. Previously, the analysts had been modelling revenues of US$3.6b and earnings per share (EPS) of US$15.30 in 2023. Indeed we can see that the consensus opinion has undergone some fundamental changes following the recent consensus updates, with a sizeable cut to revenues and some minor tweaks to earnings numbers.

See our latest analysis for Daqo New Energy

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. We would highlight that sales are expected to reverse, with a forecast 30% annualised revenue decline to the end of 2023. That is a notable change from historical growth of 57% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 14% annually for the foreseeable future. It's pretty clear that Daqo New Energy's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most obvious conclusion from this consensus update is that there's been no major change in the business' prospects in recent times, with analysts holding earnings per share steady, in line with previous estimates. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. Overall, given the drastic downgrade to this year's forecasts, we'd be feeling a little more wary of Daqo New Energy going forwards.

There might be good reason for analyst bearishness towards Daqo New Energy, like dilutive stock issuance over the past year. Learn more, and discover the 2 other risks we've identified, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.