Apellis Pharmaceuticals: A Potential Value Trap?

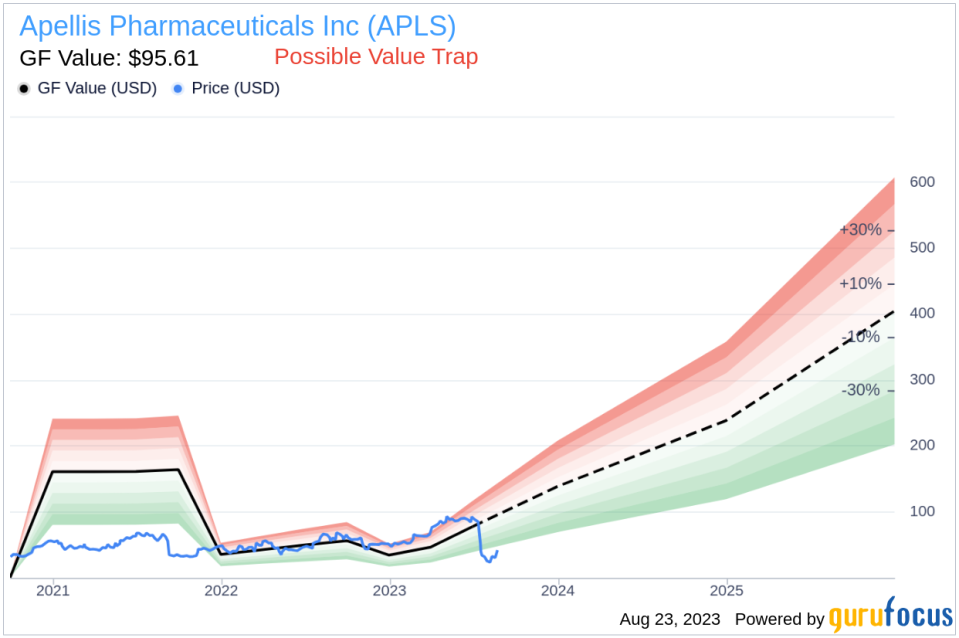

Value-focused investors are always on the hunt for stocks that are priced below their intrinsic value. One such stock that merits attention is Apellis Pharmaceuticals Inc (NASDAQ:APLS). The stock, which is currently priced at $41.8, recorded a gain of 35.89% in a day and a 3-month decrease of 53.67%. The stock's fair valuation is $95.61, as indicated by its GF Value.

Understanding the GF Value

The GF Value represents the current intrinsic value of a stock derived from our exclusive method. The GF Value Line on our summary page gives an overview of the fair value that the stock should be traded at. It is calculated based on three factors: historical multiples (PE Ratio, PS Ratio, PB Ratio and Price-to-Free-Cash-Flow) that the stock has traded at, GuruFocus adjustment factor based on the company's past returns and growth, and future estimates of the business performance.

We believe the GF Value Line is the fair value that the stock should be traded at. The stock price will most likely fluctuate around the GF Value Line. If the stock price is significantly above the GF Value Line, it is overvalued and its future return is likely to be poor. On the other hand, if it is significantly below the GF Value Line, its future return will likely be higher.

Considerations for Investment Decisions

However, investors need to consider a more in-depth analysis before making an investment decision. Despite its seemingly attractive valuation, certain risk factors associated with Apellis Pharmaceuticals should not be ignored. These risks are primarily reflected through its low Altman Z-score of -1.21, and a Beneish M-Score of 5.27 that exceeds -1.78, the threshold for potential earnings manipulation. These indicators suggest that Apellis Pharmaceuticals, despite its apparent undervaluation, might be a potential value trap. This complexity underlines the importance of thorough due diligence in investment decision-making.

Understanding the Altman Z-Score and Beneish M-Score

Before delving into the details, let's understand what the Altman Z-score entails. Invented by New York University Professor Edward I. Altman in 1968, the Z-Score is a financial model that predicts the probability of a company entering bankruptcy within a two-year time frame. The Altman Z-Score combines five different financial ratios, each weighted to create a final score. A score below 1.8 suggests a high likelihood of financial distress, while a score above 3 indicates a low risk.

Developed by Professor Messod Beneish, the Beneish M-Score is based on eight financial variables that reflect different aspects of a company's financial performance and position. These are Days Sales Outstanding (DSO), Gross Margin (GM), Total Long-term Assets Less Property, Plant and Equipment over Total Assets (TATA), change in Revenue (?REV), change in Depreciation and Amortization (?DA), change in Selling, General and Admin expenses (?SGA), change in Debt-to-Asset Ratio (?LVG), and Net Income Less Non-Operating Income and Cash Flow from Operations over Total Assets (?NOATA).

A Closer Look at Apellis Pharmaceuticals

Apellis Pharmaceuticals Inc is a clinical-stage biopharmaceutical company. It focused on the development of novel therapeutic compounds to treat disease through the inhibition of the complement system, which is an integral component of the immune system, at the level of C3 the central protein in the complement cascade.

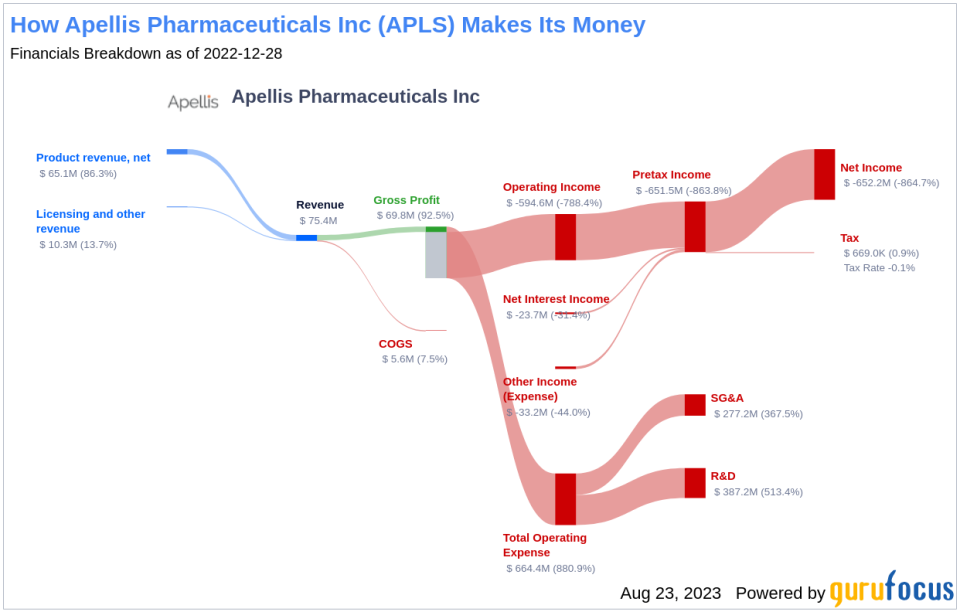

This is the income breakdown of Apellis Pharmaceuticals:

Apellis Pharmaceuticals's Low Altman Z-Score: A Breakdown of Key Drivers

A dissection of Apellis Pharmaceuticals's Altman Z-score reveals Apellis Pharmaceuticals's financial health may be weak, suggesting possible financial distress:

The Retained Earnings to Total Assets ratio provides insights into a company's capability to reinvest its profits or manage debt. Evaluating Apellis Pharmaceuticals's historical data, 2021: -1.88; 2022: -1.95; 2023: -2.85, we observe a declining trend in this ratio. This downward movement indicates Apellis Pharmaceuticals's diminishing ability to reinvest in its business or effectively manage its debt. Consequently, it exerts a negative impact on its Z-Score.

When it comes to operational efficiency, a vital indicator for Apellis Pharmaceuticals is its asset turnover. The data: 2021: 0.31; 2022: 0.11; 2023: 0.20 from the past three years suggests a recent decline following an initial increase in this ratio. The asset turnover ratio reflects how effectively a company is using its assets to generate sales. Therefore, a drop in this ratio can signify reduced operational efficiency, potentially due to underutilization of assets or decreased market demand for the company's products or services. This shift in Apellis Pharmaceuticals's asset turnover underlines the need for the company to reassess its operational strategies to optimize asset usage and boost sales.

The days sales outstanding (DSO) is an important financial metric that denotes the average time a company takes to collect payment after a sale is completed. Looking at the historical data from the past three years (2021: 0.31; 2022: 0.11; 2023: 0.20), there appears to be a rising trend in Apellis Pharmaceuticals's DSO.

An uptick in DSO might indicate aggressive revenue recognition practices, and in some cases, potential earnings manipulation. To explain, when DSO increases, it means the company's receivables are growing. This could be a result of sales being recorded before customers have paid, which inflates the revenue figures. In extreme cases, a company may even recognize revenue from sales that may never be collected, an action that is considered earnings manipulation. A rising DSO figure warrants scrutiny as it can signal financial distress or questionable accounting practices within the company. Therefore, investors should closely monitor such trends for early detection of any potential financial risks.

Next is the leverage index, which is computed as the change in the Debt-to-Asset Ratio. An increase in this ratio may suggest that the company is taking on more debt, thereby potentially inflating earnings.

Conclusion: A Potential Value Trap?

Despite Apellis Pharmaceuticals (NASDAQ:APLS) appearing to be undervalued according to the GF Value, the company's financial indicators suggest potential risks. The low Altman Z-Score and high Beneish M-Score indicate potential financial distress and earnings manipulation, respectively. Therefore, it's crucial for investors to conduct thorough due diligence before investing in Apellis Pharmaceuticals, as it might be a potential value trap.

GuruFocus Premium members can find stocks with high Altman Z-Score using the following Screener: Walter Schloss Screen . To find out the high quality companies that may deliver above average returns, please check out GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.