Arthur J Gallagher (AJG) Stock Up 32% YTD: More Upside Left?

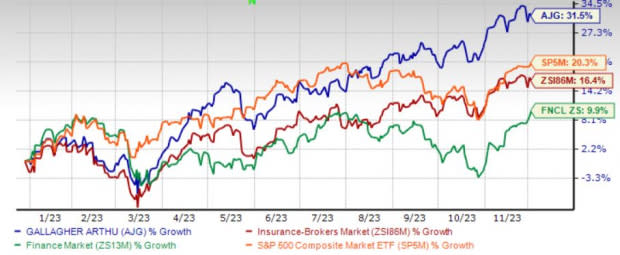

Arthur J. Gallagher’s AJG shares have gained 31.5% year to date, outperforming the industry’s increase of 16.4%, the Finance sector’s increase of 9.9% and the Zacks S&P 500 Composite’s gain of 0.4% in the same period. With a market capitalization of $53.6 billion, the average volume of shares traded in the last three months was 0.8 million.

Solid performance of the Brokerage and Risk Management segments, strategic buyouts to capitalize on growing market opportunities and effective capital deployment continue to drive AJG’s performance.

Earnings of this Zacks Rank #2 (Buy) insurance broker increased 19.9% over the last five years, better than the industry average of 11.4%. The largest property/casualty third-party claims administrator has a stellar record of beating estimates for the last 21 quarters.

Image Source: Zacks Investment Research

Can It Retain the Momentum?

The Zacks Consensus Estimate for Arthur J. Gallagher’s 2023 earnings per share (EPS) is pegged at $8.79, indicating an increase of 13.6% on 18.3% higher revenues of $10 billion. The consensus estimate for 2024 EPS is pegged at $10.11, indicating an increase of 15% on 12.7% higher revenues of $11.2 billion.

The long-term earnings growth rate is currently pegged at 13.2%, better than the industry average of 11.4%. It has a Growth Score of B.

The insurer is on track to generate both organic (particularly international) and inorganic growth. Focus on tapping opportunities across the globe bodes well for growth, thus expecting organic revenues and adjusted EBITDAC margins in 2023 in Risk Management and Brokerage segment to be better than the 2022 level.

In the Brokerage segment, AJG expects brokerage organic growth at the higher end of the 8%-9% range in 2023 and 7-9% in 2024. Adjusted EBITAC margin is expected to expand 30-40 bps in the fourth quarter of 2023 and about 50 bps in 2024.

In the Risk Management segment, the company expects fourth-quarter organic growth in double-digit banking on rising claim counts and continued growth from recent new business wins. The company expects to see organic growth of 13% in the fourth quarter and more than 15% in 2023 and 9% to 11% organic and margins around 20% in 2024.

AJG’s inorganic growth story is also impressive. This insurance broker acquired 37 entities in the first nine months of 2023 that contributed about $475.3 million to estimated annualized revenues. It has quite a strong pipeline with about $450 million of revenues, associated with almost 45 term sheets, either agreed upon or being prepared. AJG continues to expect M&A capacity upward of $3 billion through the end of 2023 and another $3.5 billion in 2024 without using any equity.

Banking on operational expertise, AJG has a solid capital position that helps it increase payouts to shareholders. Its dividend has increased at a four-year CAGR of 5.1%, currently yielding 0.9%. The board of directors also approved a $1.5 billion share buyback program.

Other Stocks to Consider

Some other top-ranked stocks from the insurance industry are Erie Indemnity ERIE, Brown and Brown BRO and Marsh & McLennan Companies MMC.

The Zacks Consensus Estimate for Erie Indemnity’s 2023 and 2024 earnings indicates a respective 49.4% and 15.5% year-over-year increase. ERIE delivered a four-quarter average earnings surprise of 10.03%. Shares have risen 22.9% year to date. It sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Brown and Brown’s 2023 and 2024 earnings indicates a respective 21.1% and 9.4% increase year over year. The consensus estimate has risen 2 cents for 2023 and 1 cent for 2024 in the past 30 days. BRO delivered a four-quarter average earnings surprise of 12.25%. It presently carries a Zacks Rank #2. Shares of BRO have risen 30.8% year to date.

Marsh & McLennan delivered a four-quarter average earnings surprise of 6.45%. The Zacks Consensus Estimate for 2023 and 2024 earnings indicates a respective 15.6% and 9.3% year-over-year increase. The consensus estimate has risen 2 cents for 2023 and 5 cents for 2024 in the past 30 days. The expected long-term earnings growth rate is pegged at 11.1%. MMC currently carries a Zacks Rank #2. Its shares have risen 19.7% year to date.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Marsh & McLennan Companies, Inc. (MMC) : Free Stock Analysis Report

Arthur J. Gallagher & Co. (AJG) : Free Stock Analysis Report

Brown & Brown, Inc. (BRO) : Free Stock Analysis Report

Erie Indemnity Company (ERIE) : Free Stock Analysis Report