Associated Banc-Corp (ASB) Rides on Organic Growth Amid Cost Woes

Associated Banc-Corp’s ASB efforts to focus on improving fee income, strategic expansion and business restructuring plans, decent loan growth and higher rates are expected to keep aiding financials. Yet, elevated expenses and substantial commercial loan exposure are headwinds.

Associated Banc-Corp is focused on its organic growth strategy, evident from solid loans and deposit balances and efforts to improve fee income. While the company’s total revenues declined in 2021, it witnessed a compound annual growth rate (CAGR) of 2.9% over the five years ended 2022, with the upward trend continuing in the first quarter of 2023.

The company expects the expansion of its lending capabilities (as part of its new strategic plan) and higher rates to help drive incremental revenues going forward. We expect total revenues (FTE) to grow 7.3% in 2023.

ASB has been undertaking measures to improve operating efficiency. In 2021, the company announced a strategic expansion plan, which has already resulted in the growth of its lending capabilities and will support core business growth and transform digital capabilities. The efforts include the addition of “higher-margin” lending portfolios and digital investments, which are expected to bolster revenues, operating leverage and profitability over time. Our estimates for gross loans suggest a CAGR of 5% by 2025.

Nonetheless, Associated Banc-Corp has been witnessing a consistent rise in non-interest expenses. Expenses witnessed a CAGR of 1% over the last five years (2017-2022). Expenses are expected to remain elevated, given the company’s inorganic growth efforts, digitization, inflationary pressure and investments in franchises. Our estimates for total non-interest expenses suggest a CAGR of 2.9% over the next three years.

Further, a major part of Associated Banc-Corp’s loan portfolio — 62.2% as of Mar 31, 2023 — comprised total commercial loans (commercial and business lending, as well as commercial real estate lending). A higher concentration of commercial loans may pose regulatory and market challenges for the company.

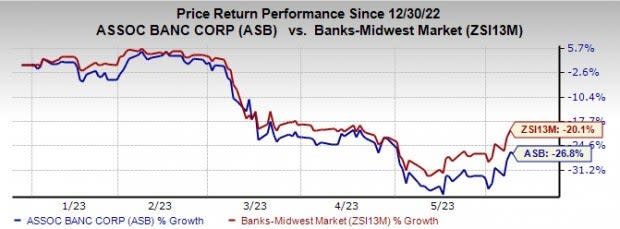

Shares of this Zacks Rank #3 (Hold) company have lost 26.8% so far this year compared with the industry’s decline of 20.1%.

Image Source: Zacks Investment Research

Banks Worth a Look

A couple of better-ranked stocks from the banking space are Pathward Financial, Inc. CASH and Bar Harbor Bankshares BHB.

The Zacks Consensus Estimate for Pathward Financial’s earnings for fiscal 2023 has been revised 1.8% upward over the past 60 days. Its shares have gained 16.2% in the year-to-date period. Currently, CASH carries a Zacks Rank #2 (Buy).

Bar Harbor Bankshares currently carries a Zacks Rank #2. Its earnings estimates for 2023 have been revised 1.4% upward over the past two months. So far this year, BHB’s shares have lost 17%. You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Pathward Financial, Inc. (CASH) : Free Stock Analysis Report

Associated Banc-Corp (ASB) : Free Stock Analysis Report

Bar Harbor Bankshares, Inc. (BHB) : Free Stock Analysis Report