B&G Foods (BGS) Gains on Q2 Earnings Beat, Sales Remain Soft

B&G Foods, Inc. BGS posted second-quarter 2019 results, wherein the bottom line crushed its four-quarter negative surprise trend. Markedly, shares of the company gained 6.4% during yesterday’s after-hour trading session.

However, the stock has slumped 38.1% year to date against the industry’s growth of 13.6%. This can be accountable to B&G Foods’ drab record. The company has been posting soft sales for a while now, and the trend continued in the quarter under review. The Pirates Brands’ divestiture to Hershey HSY continued to negatively impact sales, which was somewhat compensated by the McCann and Clabber Girl acquisitions.

Prospects from buyouts, efficient pricing and other initiatives keep management encouraged about 2019. Hence, the company raised its net sales outlook for 2019, while retaining the other forecasts. This along with B&G Foods’ better-than-expected earnings seems to have boosted investors’ confidence.

Q2 Highlights

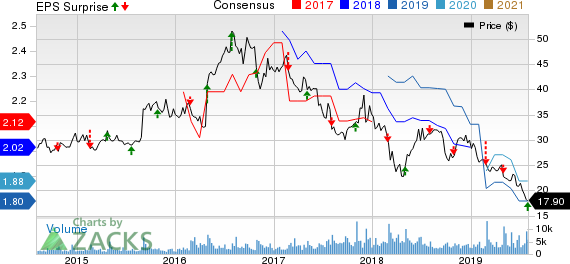

B&G Foods, Inc. Price, Consensus and EPS Surprise

B&G Foods, Inc. price-consensus-eps-surprise-chart | B&G Foods, Inc. Quote

Adjusted earnings of 38 cents per share beat the Zacks Consensus Estimate of 35 cents. The bottom line remained flat year over year. While interest expenses reduced, results were hampered by lower sales and contraction in gross margin.

B&G Foods’ net sales of $371.2 million missed the Zacks Consensus Estimate of $372 million and declined 4.4% year over year. The top line was hurt by the sale of Pirate Brands, which was partly made up by sales from McCann’s (acquired in July 2018) and Clabber Girl (acquired in May 2019). McCann’s and Clabber Girl contributed $2.2 million and $8.4 million, respectively, to B&G Foods’ net sales in the second quarter of 2019.

Net sales from the company’s base business dipped 0.5% to $360.6 million, owing to $4 million increase in net pricing, negated by a $5.5-million fall in unit volumes and currency headwinds impact of about $0.2 million.

Net sales from Green Giant products (including Le Sueur) grew 7.9%, courtesy of increased sales of frozen and shelf-stable products. Green Giant frozen net sales advanced 4.1% and Green Giant shelf-stable net sales were up 23.5%.

Adjusted gross margin was 26%, down 10 basis points (bps) year over year. SG&A expenses escalated 6.9% to $39.9 million, due to a rise in general and administrative expenses along with increased non-recurring costs and costs related to acquisitions/divestitures. This was partly compensated by a fall in warehousing, selling and consumer marketing costs. As a percentage of sales, SG&A expenses were up 1.1% to 10.7%.

Adjusted EBITDA fell 4.7% to $71 million in the reported quarter on account of Pirate Brands’ divestiture, partially cushioned by improved operating performance and the buyouts of McCann’s and Clabber Girl. Adjusted EBITDA margin dropped 10 bps to 19.1%.

Other Financial Updates

The company concluded the quarter with cash and cash equivalents of $19.9 million, long-term debt of $1,802.6 million and shareholders’ equity of roughly $868.4 million.

Outlook

B&G Foods is on track with its solid pricing initiatives, which somewhat drove sales in the second quarter. The company expects product innovation, prudent acquisitions, efficient pricing and cost of goods sold efforts to help it battle cost inflation in 2019. However, the sale of Pirate Brands is expected to continue to affect results in the third and fourth quarters.

All said, management now expects 2019 net sales of $1.665-$1.700 billion compared with the previous forecast of $1.635-$1.665 billion.

Adjusted EBITDA is still anticipated to be $305.0-$320.0 million. Further, the company projects adjusted earnings per share between $1.85 and $2.00, which stands well above the Zacks Consensus Estimate of $1.80.

Check These Solid Food Stocks

General Mills GIS, with a Zacks Rank #2 (Buy), has a long-term EPS growth rate of 7%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

McCormick MKC, also with a Zacks Rank #2, has a long-term EPS growth rate of 8%.

Breakout Biotech Stocks with Triple-Digit Profit Potential

The biotech sector is projected to surge beyond $775 billion by 2024 as scientists develop treatments for thousands of diseases. They’re also finding ways to edit the human genome to literally erase our vulnerability to these diseases.

Zacks has just released Century of Biology: 7 Biotech Stocks to Buy Right Now to help investors profit from 7 stocks poised for outperformance. Our recent biotech recommendations have produced gains of +98%, +119% and +164% in as little as 1 month. The stocks in this report could perform even better.

See these 7 breakthrough stocks now>>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Hershey Company (The) (HSY) : Free Stock Analysis Report

McCormick & Company, Incorporated (MKC) : Free Stock Analysis Report

B&G Foods, Inc. (BGS) : Free Stock Analysis Report

General Mills, Inc. (GIS) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research