Is Bausch Health Companies (NYSE:BHC) Using Too Much Debt?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Bausch Health Companies Inc. (NYSE:BHC) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Bausch Health Companies

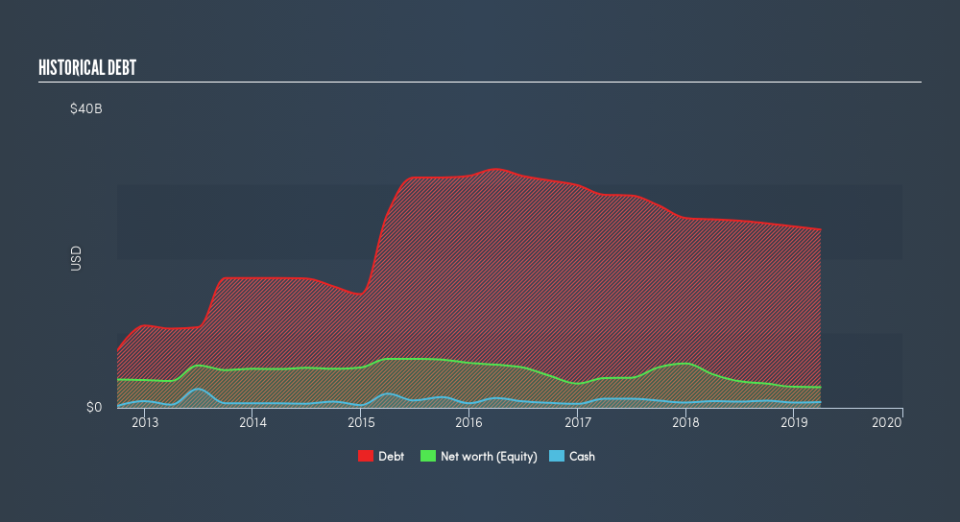

What Is Bausch Health Companies's Net Debt?

As you can see below, Bausch Health Companies had US$24.2b of debt at March 2019, down from US$25.3b a year prior. However, because it has a cash reserve of US$782.0m, its net debt is less, at about US$23.4b.

How Strong Is Bausch Health Companies's Balance Sheet?

We can see from the most recent balance sheet that Bausch Health Companies had liabilities of US$3.94b falling due within a year, and liabilities of US$25.8b due beyond that. Offsetting this, it had US$782.0m in cash and US$1.79b in receivables that were due within 12 months. So it has liabilities totalling US$27.2b more than its cash and near-term receivables, combined.

This deficit casts a shadow over the US$8.21b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt After all, Bausch Health Companies would likely require a major re-capitalisation if it had to pay its creditors today.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Weak interest cover of 0.47 times and a disturbingly high net debt to EBITDA ratio of 7.0 hit our confidence in Bausch Health Companies like a one-two punch to the gut. This means we'd consider it to have a heavy debt load. Looking on the bright side, Bausch Health Companies boosted its EBIT by a silky 83% in the last year. Like the milk of human kindness that sort of growth increases resilience, making the company more capable of managing debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Bausch Health Companies can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Bausch Health Companies actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

On the face of it, Bausch Health Companies's interest cover left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Once we consider all the factors above, together, it seems to us that Bausch Health Companies's debt is making it a bit risky. Some people like that sort of risk, but we're mindful of the potential pitfalls, so we'd probably prefer it carry less debt. In light of our reservations about the company's balance sheet, it seems sensible to check if insiders have been selling shares recently.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.