Berkshire Business Unit Focus: Pilot Flying J

On Jan. 16, Berkshire Hathaway Inc. (NYSE:BRK.A) (NYSE:BRK.B) announced the purchase of the remaining 20% of Pilot Travel Centers (PTC) from the Haslem family. A week and a half before the sale, the Delaware court lawsuit over accounting methods disputing the value of the balance of the company owned by the Haslems was settled by both parties. Both A and B shares had closed slightly below the previous day's price after the transaction was announced. Berkshire's 80% of the company before the purchase comprised 20.80% of Berkshire's revenues in the third quarter of 2023. This discussion aims to provide background information on this now wholly-owned subsidiary that makes up a large portion of the Berkshire Hathaway portfolio.

Industry characteristics

Truck stops, travel centers and travel plazas are part of the highly fragmented and competitive retail defensive industry. Most truck stops and travel centers are privately owned chains or single-location enterprises. Target customers are professional truck drivers and distance motorists who travel long distances and are looking for convenience, quick service and opportunities to rest and replenish both themselves and their fuel tanks. Most truck stops offer fuel rewards or loyalty programs to attract repeat customers.

The truck stops and travel industry began in the 1920s and was aligned with the development of the automotive industry. The first truck stops consisted mainly of simple rest stops and basic facilities such as gas stations, small buildings and diners. The industry grew rapidly during the 1950s and 1960s to include larger and more sophisticated facilities offering additional services and merchandise. In the late '80s and early '90s, truck stops combined fuel stations with convenience or travel stores and full-serve restaurants. The '90s began to attract more consumer travelers with RVs and automobiles. Truck stop operators noted that professional drivers and these new gasoline smaller vehicle customers preferred quick, convenient services and amenities, so sit-down restaurants were exchanged for quick, grab-and-go style eateries, otherwise known as quick-serve restaurants with less sit-down space. Truck stops began carrying a wider arrangement of merchandise including perfume, electronics and gift items displayed in convenient store layouts that appealed to their customer base. Some stops even feature hotels or cinemas.

Typically truck stops are conveniently located near large interstate highways. The average truck stop occupies approximately 75 acres of land to provide plenty of parking for weary professional drivers who must comply with the hours-of-service rules mandated by the Federal Motor Carrier Safety Administration.

Truck stops often engage in franchise partnerships to roll out their convenience stores and restaurant services. Warren Buffett (Trades, Portfolio) discussed the characteristics of strong economic franchise operations in his 1991 chairman's letter. Both Pilot Flying J and Travel Centers of America also offer franchise opportunities for truck stop site owners. Common FSR and QSRs franchise operations within large truck stops include Black Bear Diner, IHOP, Starbucks (NASDAQ:SBUX), Taco Bell, Dairy Queen, KFC, Subway, Pizza Hut, Dunkin' Donuts (DNKN) and many others.

The U.S. trucking market size is expected to grow at a 3% compound annual growth rate through 2027, according to Zippia.com, which leaves a modest opportunity for truck stop providers to capture additional shares of this modestly growing market.

Industry trivia

The largest truck stop in the U.S., off Interstate 80 in Walcott, Iowa, is three times larger than the size of an average truck stop and has 5,000 visitors per day. It has been a Travel Centers of America franchised operation since 1992, after the death of then-owner Bill Moon (the site is still owned by the Moon family.)

The oldest truck stop in the U.S. is Dixie Travel Plaza, which was established in 1928 and is just off Interstate 55 in McLean, Illinois. Since 2012, Dixie Travel Plaza has been owned by Road Ranger, which was purchased by Chilean company Enex, a subsidiary of Quinenco SA (XSGO:QUINENCO), in 2018.

Competitive landscape

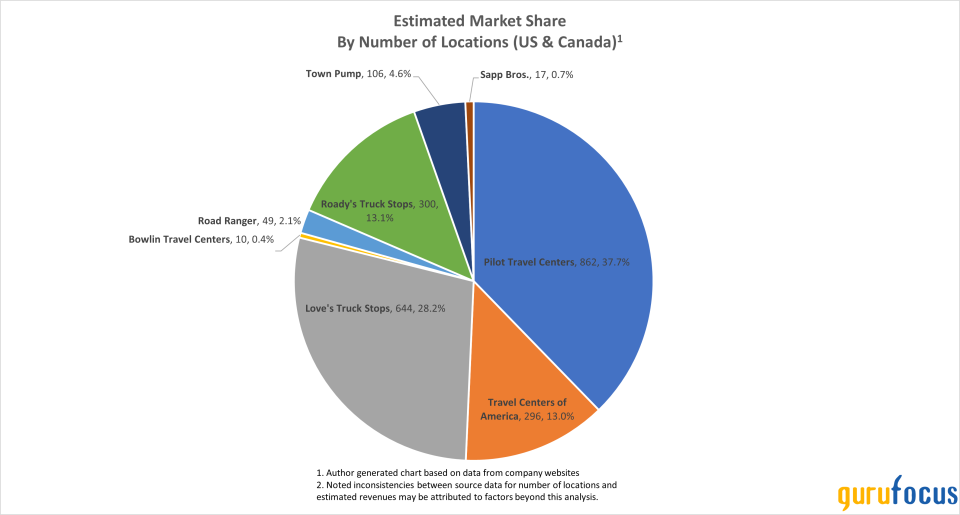

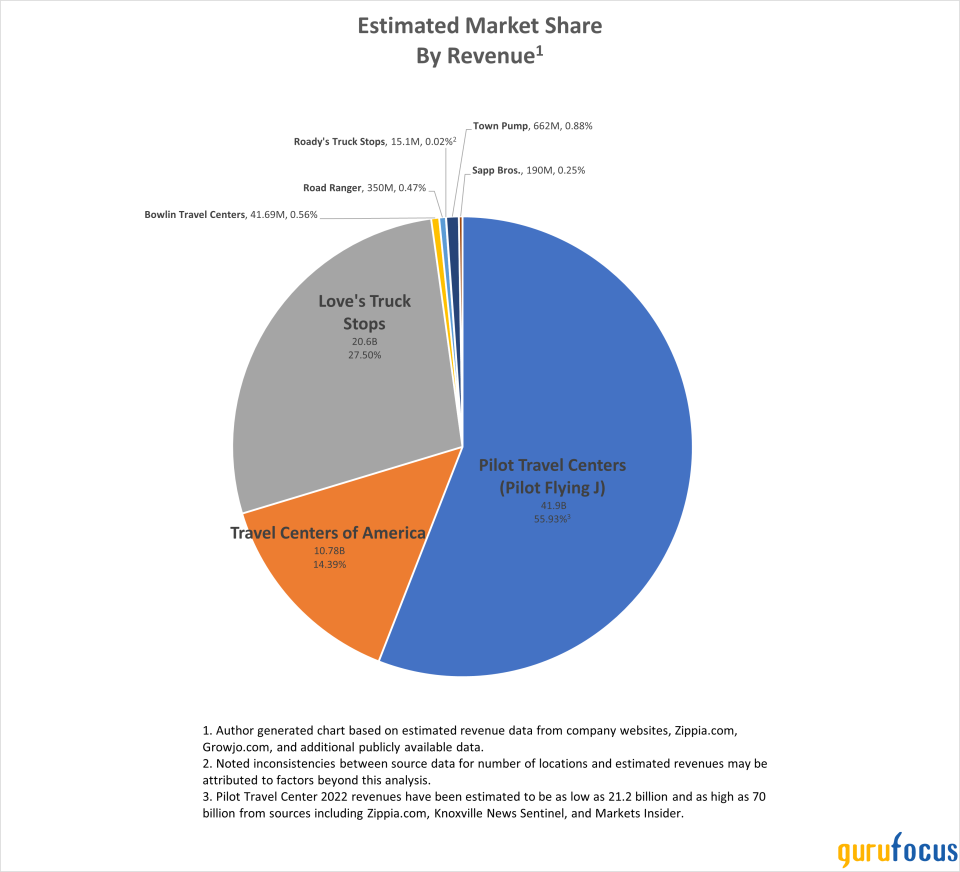

The charts below roughly depict the distribution of geographic footprint and 2022 revenue estimates for major truck stop players in the U.S. and Canada. These data from publicly available sources contain caveats in terms of accuracy as all these establishments are either privately owned or are subsidiaries of larger corporations, so do not comply with SEC filing guidelines. Also, chains often consist of both large truck stops that accommodate professional rigs and heavy traffic as well as smaller, traditional gas stations or related businesses, so comparisons between the number of locations and revenue estimates are not reflective of the differences in individual receipts and volume of traffic per each location. For example, Love's Truck Stop's geographical footprint also includes its Speedco subsidiary of oil change specialty shops acquired in 2017. The location map may also conceal an overlap in the number of sites for Pilot and Town Pump as the companies have a notable relationship in Montana. Pilot lists 36 Town Pump sites in its list of locations and Town Pump acquired three Montana Pilot Flying J locations, which it still operates under the Pilot brand as part of a Federal Trade Commission agreement designed to reduce competition in a 2010 merger between Pilot Travel Centers and Flying J Inc.

Nevertheless, Pilot appears to be the clear leader both in terms of its geographic footprint and estimated revenue. The most formidable competitor is Love's Truck Stops. Pilot Travel Centers LLC (doing business as Pilot Flying J) is now wholly owned by Berkshire Hathaway. Travel Centers of America operated as a publicly traded company until February of 2023, when BP (NYSE:BP) purchased the company. As stated above, Road Ranger is owned by the Enex subsidiary of Quinenco. Other players in this field are privately held.

Berkshire's investment in Pilot

Berkshire started investing in Pilot Flying J when Buffett bought a 38.60% stake in the company in October 2017 for $3 billion and bought an additional 41.40% stake in January 2023 for an estimated value of roughly $8.20 billion, with the remaining 20% of the company bought for an estimated $11 billion in January of this year.

Before Berkshire's investment, Pilot Travel Centers had many of the large-moat business characteristics that attracted the Oracle of Omaha, including a long, family-centric operating history, market dominance and good brand recognition. Forbes ranked Pilot as the fifth-largest private U.S. company before Berkshire Hathaway's investment in 2017 and the large influx of the conglomerate's cash flow resources has improved the company's debt rating and expanded its geographical footprint.

Since Berkshire's initial stake, Pilot Flying J has grown by nearly 15% in terms of its North American footprint. The company had an annual increase in revenues between 2021 and 2022 of nearly 58%. Thus, Berkshire Hathaway has paid approximately $22 billion for a company that generates as much as $42 billion annually and may generate more than $1 billion in cash flow this year. However, revenue and profits of the company have both decreased since 2022. In April 2023, Berkshire replaced the Haslem-selected CEO and chief financial officer positions with two well-entrenched Berkshire executives.

Pilot's impact on Berkshire Hathaway

Pilot's contribution to Berkshire's profitability is a tall order considering the sheer size of its entire portfolio and operations. The company has admittedly struggled in recent years to find acquisitions that can solidly benefit its investment value position. As Pilot Travel Centers comprised a large percentage of Berkshire's revenues in the third quarter of 2023, one way to gauge the impact of this acquisition is by looking at its stock performance since the time of the company's initial investment and comparing it to the performance of the stock's performance before that time. Another way is to gauge Berkshire's total return since the acquisition against a larger market index.

To apply the first gauge, I compared various point-in-time metrics of third-quarter 2017 (a snapshot from a time before Berkshire's initial investment in Pilot) with its current metrics:

PERFORMANCE | 3RD-QUARTER 2017 | CURRENT | CHANGE (CAGR) |

SHARE PRICE TTM | $270,430.00 | $610,086.00 | 14.52% |

REVENUE TTM | $235.14B | $349.271B | 7.10% |

NET INCOME TTM | $18.675B | $76.813B | 22.00% |

FCF TTM | $33.001B | $26.723B | 3.90% |

TOTAL RETURN TTM | 21.05% | 30.56% | 6.41% |

VALUATION | 3RD-QUARTER 2017 | CURRENT | CHANGE (CAGR) |

PE RATIO TTM | 20.44 | 11.57 | 6.41% |

PB RATIO TTM | 1.51 | 1.68 | 1.79% |

PFCF TTM | 14.15 | 33.04 | 15.18% |

EV/SALES | 2.08 | 2.79 | 5.02% |

EV/EBITA | 11.73 | 16.92 | 6.30% |

EARNINGS YIELD | 5.05% | 8.72% | 9.53% |

FCF YIELD | 7.40% | 3.03% | 16.05% |

CAPITAL ALLOCATION | 3RD-QUARTER 2017 | CURRENT | CHANGE (CAGR) |

ROA TTM | 2.87% | 7.81% | 18.16% |

ROE TTM | 6.06% | 14.62% | 15.81% |

ROIC TTM | 3.22% | 3.97% | 3.55% |

To apply the second gauge, I compared the growth of shares and dividends (a proxy for total return) for Berkshire against the Vanguard S&P Value Index Fund ETF (VOOV) and the Vanguard 500 Index Fund (VOO) from Oct. 2, 2017 (a snapshot from a time before the initial investment in Pilot) until today.

Keep in mind these results have been convoluted by changes and events that occurred to Berkshire Hathaway's greater portfolio during that time. Since 2017, the conglomerate has made sizable investments in Apple (NASDAQ:AAPL) and Bank of America (NYSE:BAC) in addition to those made in Pilot.

Despite the Pilot acquisition, Berkshire Hathaway is currently not attractive as a value investment prospect. GuruFocus gives the Class A stock an overall score of 69 and a value rank of just 1 priced over 36% above its GF Value.

Conclusion

Pilot Travel Centers is a longtime market leader in the heavily competitive truck stop and travel center business. The company has all the aspects of a quality business that Buffett loves, was bought at a screaming deal and will likely positively affect Berkshire Hathaway's business in the coming years. Unfortunately, with its huge size and cash position, a lot is needed from an acquisition to move the needle of profitability and value upward, and Pilot's ability to do that may fall short.

Currently, Berkshire stock is not an attractive buy. However, if the company can find more diamonds like Pilot in the future, its prospects as a viable investment will be rosy.

This article first appeared on GuruFocus.