Is BHP Billiton plc’s (LSE:BLT) Balance Sheet A Threat To Its Future?

There are a number of reasons that attract investors towards large-cap companies such as BHP Billiton plc (LSE:BLT), with a market cap of GBP £71.71B. One such reason is its ‘too big to fail’ aura which gives it the appearance of a strong and healthy investment. However, investors may not be aware of the metrics used to measure financial health. There are always disruptions which destabilize an existing industry, and although large-caps are hard to knock down, it is useful to understand its level of resilience. Here are few basic financial health checks to judge whether a company fits the bill or there is an additional risk which you should consider before taking the plunge. Check out our latest analysis for BHP Billiton

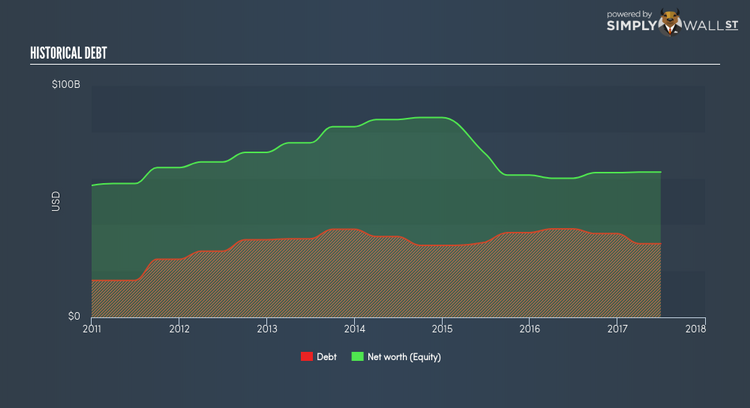

Is BLT’s level of debt at an acceptable level?

What is considered a high debt-to-equity ratio differs depending on the industry, because some industries tend to utilize more debt financing than others. As a rule of thumb, a financially healthy large-cap should have a ratio less than 40%. In the case of BLT, the debt-to-equity ratio is 50.73%, which means, while the company’s debt could pose a problem for its earnings stability, it is not at an alarmingly high level yet. No matter how high the company’s debt, if it can easily cover the interest payments, it’s considered to be efficient with its use of excess leverage. A company generating earnings (EBIT) at least three times its interest payments is considered financially sound. BLT’s interest on debt is sufficiently covered by earnings as it sits at around 13.31x. Debtors may be willing to loan the company more money, giving BLT ample headroom to grow its debt facilities.

Does BLT generate enough cash through operations?

A simple way to determine whether the company has put debt into good use is to look at its operating cash flow against its debt obligation. This also assesses BLT’s debt repayment capacity, which is not a big concern for a large company. In the case of BLT, operating cash flow turned out to be 0.53x its debt level over the past twelve months. This is a good sign, as over half of BLT’s near term debt can be covered by its day-to-day cash income, which reduces its riskiness to its debtholders.

Next Steps:

Are you a shareholder? BLT’s high debt level shouldn’t be an impetus for investors to sell given its high operating cash flow seems adequate to meet obligations which means its debt is being put to good use. Since BLT’s financial situation may differ over time, I suggest exploring market expectations for BLT’s future growth on our free analysis platform.

Are you a potential investor? Although investors should analyse the serviceability of debt, it shouldn’t be viewed in isolation of other factors. After all, debt is often used to fund or accelerate new projects that are expected to improve a company’s growth trajectory in the longer term. This is why I suggest you examine BLT’s Return on Capital Employed (ROCE) in order to see management’s track record at deploying funds in high-returning projects.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.