Big Bank Earnings: Why $18 Billion in Tax Savings May Not Be a Buy Signal

Earlier this week, the biggest banks in the U.S. released their fourth-quarter and full-year earnings for 2019. JPMorgan Chase & Co. (NYSE:JPM), Bank of America (NYSE:BAC), Citigroup (NYSE:C) and Morgan Stanley (NYSE:MS) posted earnings and revenue beats, with only Wells Fargo & Co. (NYSE:WFC) and Goldman Sachs (NYSE:GS) falling short due to litigation costs.

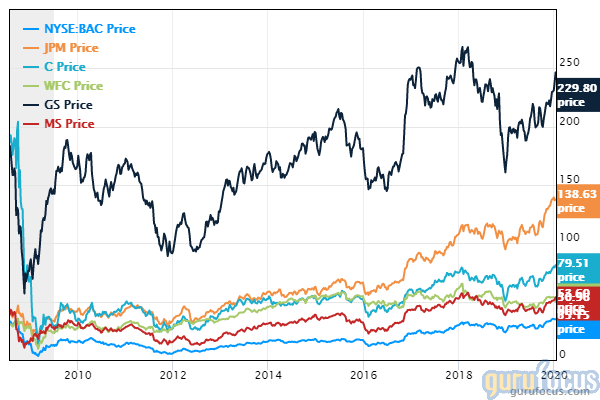

For the quarter, JPMorgan's $29.2 billion in revenue and $2.57 in earnings per share beat analyst expectations of $27.26 billion and $2.32. Bank of America saw revenue of $22.5 billion and earnings of 74 cents per share compared to estimates of $22.35 billion and 68 cents, Citigroup saw revenue of $18.38 billion and earnings of $1.90 compared to estimates of $17.7 billion and $1.82 and Morgan Stanley saw revenue of $10.9 billion and earnings of $1.30 compared to sales estimates of $9.72 billion and EPS of 99 cents.

Goldman Sachs posted a revenue beat of $9.96 billion compared to estimates of $8.9 billion, earnings per share came in at $4.69, falling short of expectations of $5.47 due to litigation costs. Wells Fargo's revenue and earnings per share were predicted to reach $19.81 billion and $1.12, respectively. However, the bank ended the quarter with revenue of $19.86 billion and earnings per share of 93 cents, again due to litigation costs.

With many of the banks posting record numbers on their earnings statements, some may wonder why some of their share prices dropped by a couple percentage points following the reports before going back up. Doesn't increasing profitability make a stock even more attractive? However, these numbers aren't all good news for the banks, and they may not necessarily make the stocks a good buy for new investors - here's why.

Where did the tax savings go?

The Tax Cuts and Jobs Act was a large part of what powered the big banks through to make record profits for two years straight. Despite being sold to the public as a way to help struggling companies (and thereby workers), the tax cuts had another purpose - to provide an earnings boost for banks in preparation for upcoming Federal Reserve interest rate cuts. However, while the cuts made the big banks look more attractive to investors by driving up earnings, large portions of the money saved ended up skipping over balance sheets and landing in the wallets of shareholders and top executives instead. Some of it ended up benefitting workers, but the important point is that it missed the balance sheets almost entirely.

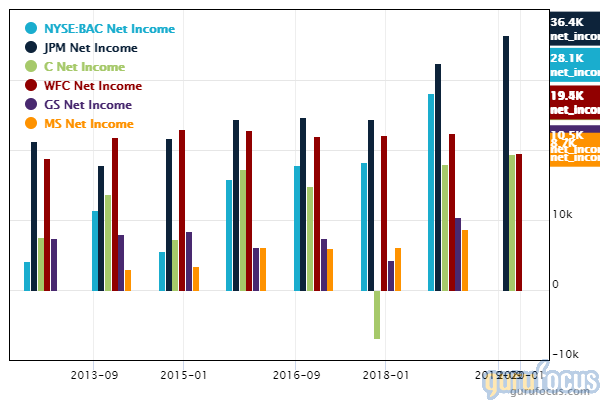

Let's do the math. The big banks reported combined tax savings of $18 billion in 2019 compared to $14 billion in 2018, which represents a 10% to 12% drop in the interest rate compared to the 30% that was in place before the cuts. On average, this saved each bank around $3 billion for 2019 and $2.3 billion in 2018. We don't have all the necessary numbers for the 2019 calculations yet, so let's go over 2018 instead. As you can see in the chart below, most of the six banks saw jumps in net income when the tax cuts went into effect in 2018. This was partially due to the tax cuts, but also partially due to other factors such as increases in deposits, investment banking and global expansion.

Bank of America, for example, received $3.5 billion in tax savings in 2018, contributing to a $10 billion jump in net income to $28 billion. It issued shareholder payouts worth $6.1 billion in the first quarter (mostly through an intensive share repurchase program), raised the CEO's salary by 15% and paid workers a combined $145 million in bonuses and salary increases (the bank had approximately 135,500 employees in 2018). Net interest yield of around 2.52% for 2018 declined to around 2.35% by the end of 2019, but growth in deposits still pushed interest income up from $47.4 billion in 2018 to $49.4 billion in 2019.

Could the tax savings help in a recession?

From these numbers, we can reasonably conclude that if the economy were to enter a recession, the money that big banks continue to receive from tax cuts would not do much in the way of providing a cushion. Instead, most of it has gone toward rewarding shareholders and making the stocks look more attractive on paper through share buybacks, achieving neither of the original goals of significantly increasing workers' paychecks or increasing the banks' risk positions.

While in a strong bull market, the impact of interest rate cuts on the earnings of large, diversified banks that offer a variety of financial services is indeed insignificant, it becomes far more of a drawdown when a market enters bear territory and both households and corporations begin defaulting on their loans and declaring bankruptcy.

In fact, lowering interest rates during a strong bull market has the potential to increase the number of loans that are available to go bad during financially lean times. Lower rates encourage households and businesses alike to borrow more money, which is why banks on average have seen increases in their net interest income in 2018 and 2019, despite lower rates. This is essentially borrowing growth from the future, making the potential downside worse in exchange for accelerating growth and tossing out cash in the short term.

Thus, while both tax savings and interest rate cuts have helped banks continue to grow their earnings by making them look more financially attractive and making it easier for their customers to borrow money, respectively, neither of these things will help the banks when the bull market eventually comes to an end. For the most part, $18 billion in tax savings is not a good reason to rush out and buy bank stocks - not unless you are confident that the continued trend of increased borrowing, low default levels and aggressive share buybacks will continue over the long term.

Disclosure: Author owns no shares in any of the stocks mentioned. The mention of stocks in this article does not at any point constitute an investment recommendation. Investors should always conduct their own careful analysis or consult registered investment advisors before taking action in the stock market.

Read more here:

Not a Premium Member of GuruFocus? Sign up for a free 7-day trial here.

This article first appeared on GuruFocus.