Booz Allen (BAH) Shares Fall 1.4% Despite Q3 Earnings Beat

Booz Allen Hamilton Holding Corp. BAH reported better-than-expected third-quarter fiscal 2024 results.

Quarterly adjusted earnings per share (EPS) of $1.41 surpassed the Zacks Consensus Estimate by 24.8% and exceeded the year-ago quarter by 31.8%. The company reported revenues of $2.57 billion, which beat the consensus estimate by 1.5% and increased 12.9% year over year. Revenues, excluding billable expenses, were $1.77 billion, up 13% year over year.

However, BAH’s impressive third-quarter results failed to impress the investors as the company’s shares declined 1.4% since its earnings release on Jan 26.

Backlogs

Total backlog increased 14.2% from the prior-year figure to $34.3 billion. This surpassed our estimate of $33.3 billion. Funded backlog of $5.2 billion increased 15.6% year over year. Unfunded backlog declined 9.2% to $9.2 billion.

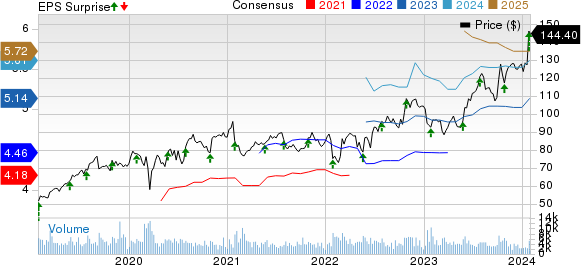

Booz Allen Hamilton Holding Corporation Price, Consensus and EPS Surprise

Booz Allen Hamilton Holding Corporation price-consensus-eps-surprise-chart | Booz Allen Hamilton Holding Corporation Quote

Priced options increased 29.3% to $19.9 billion. The book-to-bill ratio was 0.72, up from 0.09 a year ago. The headcount of 33,798 improved 8.6% year over year.

EBITDA Margins Rise

Adjusted EBITDA amounted to $290.6 million, up 19.1% year over year. It outshined our projection of $268.6 million. Adjusted EBITDA margin on revenues increased to 11.3% from 10.7% in the prior year.

Key Balance Sheet & Cash Flow Numbers

Booz Allen exited the quarter with cash and cash equivalents of $601.8 million compared with $557.3 million at the year-ago quarter end. Long-term debt (net of current portion) was $3.37 billion compared with $3.39 billion in the prior quarter.

The company used $234 million of net cash from operating activities. Capital expenditures were $23.1 million. Free cash flow was $210.9 million.

Updated Fiscal 2024 Outlook

BAH currently projects revenue growth in the range of 14-15% compared with the prior view of 11-14%. It expects adjusted EPS in the range of $5.25-$5.40 (prior view: $4.95-$5.10). The current Zacks Consensus Estimate for earnings of $5.03 per share is below the EPS guidance.

Adjusted EBITDA is now expected in the range of $1.16–$1.18 billion compared with its prior view of $1.12 billion to $1.15 billion. Adjusted EBITDA margin on revenues is anticipated to be around 11%, revised from the previous range of 10-11%. Net cash provided by operating activities is still projected in the range of $200-$275 million, revised from the previously expected $160-$260 million. The company expects the effective tax rate to be in the 22-23% band.

Booz Allen currently sports a Zacks Rank #1 (Strong Buy).

Other Stocks to Consider

Investors interested in the broader Business Services sector can consider the following other top-ranked stocks:

DocuSign DOCU: The Zacks Consensus Estimate for DocuSign’s fiscal 2024 revenues indicates 9.2% growth from the year-ago figure while earnings are expected to grow 41.4%. The company beat the consensus estimate in each of the past four quarters, the average surprise being 24.7%.

DOCU currently sports a Zacks Rank of 1. You can see the complete list of today’s Zacks #1 Rank stocks here.

Broadridge Financial Solutions BR: The Zacks Consensus Estimate for Broadridge’s 2024 revenues indicates 7.7% growth from the year-ago figure, while earnings are expected to grow 10.1%. The company beat the consensus estimate in three of the past four quarters and matched on one instance, the average surprise being 5.4%.

BR carries a Zacks Rank #2 (Buy), at present.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Broadridge Financial Solutions, Inc. (BR) : Free Stock Analysis Report

Booz Allen Hamilton Holding Corporation (BAH) : Free Stock Analysis Report

DocuSign (DOCU) : Free Stock Analysis Report