Boston Scientific (BSX) Hits 52-Week High: What's Driving It?

Shares of Boston Scientific Corporation BSX reached a new 52-week high of $50.87 on Apr 5 before closing the session marginally lower at $50.74.

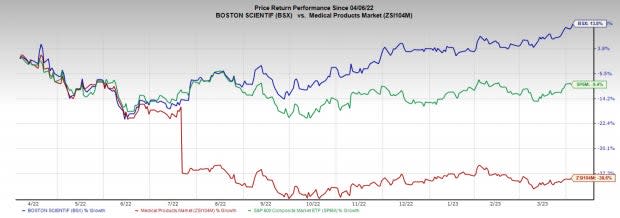

In the past year, this Zacks Rank #3 (Hold) stock has risen 13.8% against a 38.6% decline of the industry and the S&P 500 composite’s fall of 9.4%.

Boston Scientific has a long-term expected earnings growth rate of 11.2%. The company has a favorable P/Sales ratio of 4.6 compared with the industry’s P/Sales ratio of 8.2. In the last reported quarter, Boston Scientific’s revenues surpassed the Zacks Consensus Estimate by 0.12%. The average earnings surprise in the trailing four quarters was 0.22%.

BSX is witnessing an upward trend in its stock price, prompted by several recent acquisitions, including strategic investments made to complement the company’s Electrophysiology portfolio. The optimism led by the organic revenue growth in the fourth quarter of 2022 and bullish 2023 guidance is expected to contribute. However, exposure to competitive markets and flat sales of the company’s pacemaker device are major downsides.

Let’s delve deeper.

Image Source: Zacks Investment Research

Key Growth Drivers

Acquisitions to Add Value: We are upbeat about Boston Scientific’s several recent acquisitions, which will potentially boost the top line in the long term.

In February 2022, the company completed the acquisition of Baylis Medical Company. The Baylis integration continues to go well with the differentiated Transseptal access and remains on track to achieve its full-year expectations.

Further, Boston Scientific recently announced its plans to buy a majority stake in M.I. Tech to broaden the company’s Neuromodulation product line. The strategic investment in the Chinese medical technology company, Acotec, is expected to expand Boston Scientific’s drug-coated balloon offerings.

In November 2022, BSX also entered into a definitive agreement to acquire Apollo Endosurgery. The $615 million acquisition deal will add a complementary and innovative endoluminal surgery portfolio to the company.

Promising Growth From WATCHMAN Device: Boston Scientific’s structural heart programs are fast building momentum, banking on the strong performance of the WATCHMAN left atrial appendage closure device. The next generation WATCHMAN FLX is strongly capturing the European market.

In the fourth quarter, WATCHMAN’s organic sales grew 22% year over year. BSX recently completed the enrollment of the CHAMPION-AF trial way ahead of the schedule.

Per a representative of the company, this head-to-head trial versus novel oral anticoagulation has the potential to more than triple the number of patients indicated for WATCHMAN FLEX in 2027 and beyond.

Currently, the company expects double-digit growth within WATCHMAN in 2023, fueled by innovation, ongoing clinical evidence and strong commercial execution.

A Strong Q4 Performance: Over the past year, Boston Scientific has outperformed its industry. In the fourth quarter, Boston Scientific’s revenues were in line with the Zacks Consensus Estimate. The company registered a year-over-year improvement in organic sales, indicating a strong rebound in the legacy business even amid several macroeconomic issues.

Organic revenues in each of its core business segments and geographies were up in the reported quarter.

The 2023 guidance given by the company appeared bullish. This indicates that Boston Scientific is well-poised to handle the industry-wise trend of currency headwinds and global inflationary pressure.

Downsides

A Competitive Landscape: The presence of many players has made the medical device market highly competitive. BSX participates in several markets, including Cardiovascular, CRM, Endosurgery and Neuromodulation, where it faces competition from large, well-capitalized companies such as Johnson & Johnson, Abbott, Medtronic, Stryker, Smith & Nephew and Edwards Lifesciences, apart from several other smaller companies.

Pacemaker Sales Still Sluggish: Declining worldwide pacemaker sales over the recent past continued to weigh on Boston Scientific's CRM results. However, pacemaker sales should gradually improve with new product launches (including the launch of the RESONATE platform) and easier comps.

Key Picks

Some better-ranked stocks in the broader medical space are Orthofix Medical OFIX, Viemed Healthcare VMD and Insulet PODD.

Orthofix Medical, carrying a Zacks Rank #2 (Buy) at present, has an estimated growth rate of 57.71% for the next year. Orthofix’s earnings surpassed the Zacks Consensus Estimate in three of the trailing four quarters and missed the same in one, the average surprise being 140.02%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Orthofix Medical’s shares have decreased 47.4% compared with the industry’s 15.9% decline in the past year.

Viemed Healthcare, carrying a Zacks Rank #2 at present, has an estimated growth rate of 83.33% for 2024. Shares of VMD have surged 89.4% against the industry’s 38.6% decline over the past year.

In the last reported quarter, Viemed Healthcare’s earnings surpassed the Zacks Consensus Estimate by 25%, while revenues missed by 1.3%.

Insulet, carrying a Zacks Rank #2 at present, has an estimated growth rate of 56.59% for 2024. Insulet’s shares have risen 18.2% against the industry’s 38.6% decline over the past year.

PODD’s earnings surpassed estimates in three of the trailing four quarters and missed the same in one, the average surprise being 59.81%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Boston Scientific Corporation (BSX) : Free Stock Analysis Report

ORTHOFIX MEDICAL INC. (OFIX) : Free Stock Analysis Report

Insulet Corporation (PODD) : Free Stock Analysis Report

Viemed Healthcare, Inc. (VMD) : Free Stock Analysis Report